This journal logs investment transactions made in the portfolio. Hopefully it will help me be more rigorous/honest with myself.

July 2026

- Sell NWBD (£1.44). I am actually underweight UK Fixed Income, so selling some feels odd. However I am struggling with how over-weight I am in my SIPP on Fixed Income, and underweight growth assets like US Equities. So I am rotating a little bit within the SIPP. NWBD is a large holding for me – probably too large given the risks with single line debt holdings.

- Buy IGG (£15). IG Group has announced a large $1.3bn acquisition of Underdog. The share price has dropped >10% as a result. This is classic muppetry by UK institutions, fretting about the cancellation of the share buyback programme. The IG CEO Breon Corcoran is one of the best out there and he has an excellent track record (in previous life at Paddy Power and Betfair) of acquisitions. I am buying on the dip.

- Sell MCD ($270). Longstanding (10+ year) holding that has underperformed and I am now taking opportunity to Close the position, looking to reduce overweight USA Equities exposure.

- Sell Adyen. Closing this position too – partly to balance the portfolio and partly due to lower confidence.

- Buy SUPR. Topping up in the ‘property proxy’ portfolio. This portfolio is almost two years old so in theory it would be nice if all holdings need to be about 5% bigger than at inception – I am some way off.

- Buy LLPC. Topping up – I need Fixed Income UK and in a GIA, and as luck would have it that opportunity (i.e. some reinvestable dividends) has presented itself.

June 2026

- Buy ALU (£2.40). Topping up, reinvesting (wider) dividends.

- Close ADYEN (€845). I’m liquidating this position. My original investment thesis doesn’t really apply, and I need some funds to make an angel investment.

- Buy ULVR (£42.55). Reinvesting some ULVR dividends. I can’t get too excited about the underlying investment here but I do think the share price is low and has asymmetric upside to it.

- Buy NTEA (£1.23). Modest inflation-proofing in my ‘property proxy’ portfolio.

May 2026

- Buy PBEE (£1.38). I’m topping up. This business is back below it’s (very overpriced) 2021 IPO price. But it’s 4 times bigger now, growing, and operating cash positive. So while it is still expensive on fundamentals, I think it compares pretty favourably to other SaaS-like stocks.

April 2026

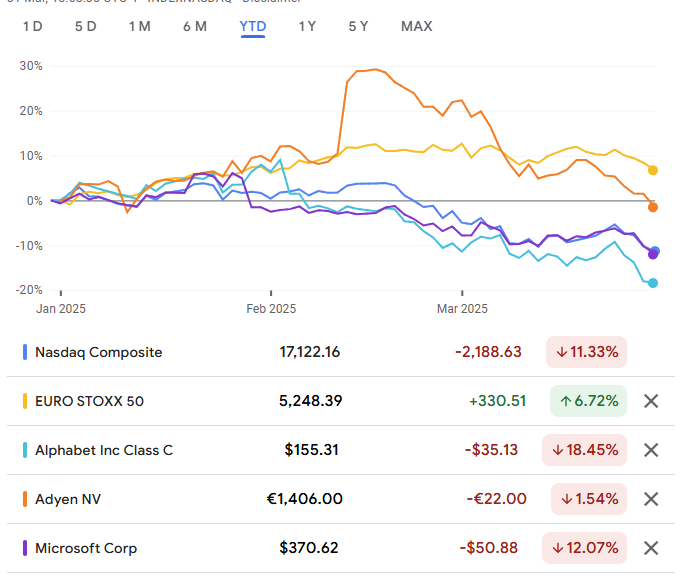

- Sell GOOG ($372). Can’t quite believe I sold some of this for $315 earlier this month… but I’m selling a bit more in the pre-open session on the back of excellent numbers yesterday. Much as I rate Google, and its AI, I think its core search business and its cloud business haven’t got quite the prospects they would like right now, and I’m derisking a little.

- Close WISE (£10.50). I need some liquidity for a possible car purchase. WISE feels too low margin and low growth, and quite exposed to further geopolitical dramas, so I am bailing.

- Close HGT (£3.38). I am (temporarily) exiting this position. Partly to raise some liquidity, and partly to crystallise a (SaaS-pocalypse) loss. I think HGT is probably a buy right now and plan to re-enter this position when liquidity allows.;

- Sell GOOG ($315). Selling more of my favourite stock. Sigh. But in fact I am raising a bit of liquidity for a project I am contemplating / derisking by top slicing one of my biggest holdings / etc. I will have some capital gains from this but considering I sold at $265 not too long ago I think that is all in the round.

- Buy NWBD (£1.48). Topping up some UK Fixed Income, in a tax-sheltered account. I sold quite a lot of this holding last month in other accounts as part of a clear-out, so to some extent I am recycling.

March 2026

- Various ETF buys/sells to simplify/refocus holdings between accounts.

February 2026

- Buy AMZN ($198). Buying on the dip. AMZN seems to be getting caught by the SaaS-pocalypse. I don’t feel it should be. It is an AI arms merchant, and still has an all-conquering e-commerce biz. at $200/share it is back to 2024 pricing, despite being 50% bigger.

- Sell FEV (£4.30). This European investment trust isn’t liked by IB, I think because it has a modest level of internal leverage. In any case it has been underperforming H50E/the index. I’m closing out of it in one account.

- Sell ULVR (£52). I’m a complexity mood and looking to reduce holdings. Easiest done in tax sheltered accounts like pension accounts. I’m closing out of it in a pension account.

- Sell Nestle (Fr74). I am closing out this Swiss holding in one account – it’s an account which makes dealing with CHF and Swiss things very painful, so this is really a tidying up exercise.

December 2025

- Sell ADBE ($352). I am slowly closing out this position.

- Sell MICC (£11.60). Unilever has spun out the Magnum Ice Cream Company. I haven’t followed this closely but it leaves me with a subscale holding that I don’t particularly fancy bulking up on. I’m treating it as a capital distribution and am selling it. Heaven knows what that does to my Capital Gains realisations but we’ll see in due course.

November 2025

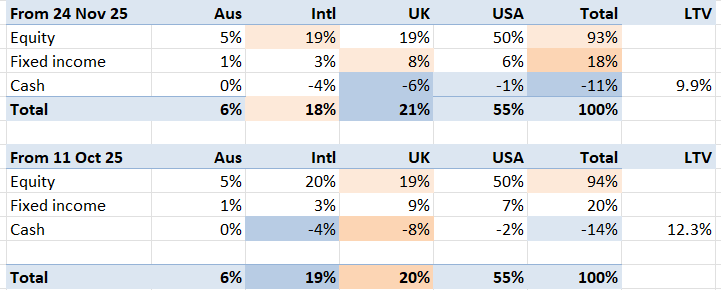

Following that tweak to the target allocation, I am now a bit Long (for once) on Fixed Income. I am also feeling a bit sour about how my ISAs are so laden with fixed income that they are not delivering the sort of returns the rest of my portfolio is delivering. So a few tweaks, all within an ISA account

- Sell Janus Henderson Asian Income (£1.05)

- Sell VUCP (£36.68).

- Sell LLPC (£1.50). Very rare trim of one of these high coupon bonds.

- Buy LCUK (£13.71). I am a bit underweight UK equities.

- Buy HSPX (£51). I have zero USA Equities in a key ISA account. Time to start, in a modest way, correcting this.

- Buy ADM (£31.40). Topping up this still-small position.

Another change to the target allocation – reflecting a windfall I’ve just received, which I’m using to pay down debt a bit faster than normal. Overall this is a tightening of the leverage target, pulling back my level of equity and fixed income by a small amount to offset.

And some trades

- Buy IGG (£10.50). Limit order filled, topping up this (quite small) holding on a dip.

- Buy ADM (£32.50). Topping up this UK Equity, in an ISA. It has 6.5% divi yield and a P/E of 13 right now, which feels like good value. Admittedly this is because profitability has more than doubled very quickly, which may not be sustainable.

- Buy WISE (£9.10). Topping up, on a dip. Wise’s latest results show costs growing twice as fast as revenues – never a good look. I’m nonetheless quite impressed by the growth numbers, and the number of integrations / licenses the platform is assembling. My hunch is that some of the cost increases are marketing investments. This is a relatively small holding so I’m going to buy a bit more and keep watching.

October 2025

- Sell SHOP ($180). Taking profits, via a small top-slice. Tech stocks have gone ballistic this month. SHOP is over 100% up y-on-y. I’ll incur some CGT but that might be just as well, depending on what the budget has in store for us next month.

- Sell GOOG ($270). GOOG is on a tear. It’s my biggest single stock holding, and is giving me concentration risk issues – especially when the tech sector seems so hot right now. And much as I love the stock, it’s up 10% on the month and I am taking profits via another small top slice.

- Rebalancing from International Equities to UK/USA Fixed Income in a tax-sheltered account

- Sell HMEF (£10.45) – up about 20% in 12 months – quite a large holding – I am slightly overbalanced International Equities so am reducing this

- Buy VGOV (£16.13) – a stalwart UK Fixed Income holding, now yielding 4.55% – that income is worth having tax-sheltered

- Buy HMT Gilt 4.75% 22/10/35 – Topping up – similar logic to VGOV

- Buy VUTY (£16.47) – adding this USA Fixed Income holding into my tax-sheltered account – it yields 4.2% these days

- Buy LLPC (£1.53) – stalward corporate-bond-ish – yielding about 6%. I have quite a lot of exposore to this but figure Lloyds is trustworthy.

- Buy BHP (£21). Topping up on this Aus Equity, where I am a bit underweight. Feels fully priced. But a quality stock.

- Sell ADBE ($350). I like Adobe’s numbers. But I don’t like its share price movement over the last two years – in which it has halved. I have been viewing it as a buying opportunity but now I have lost confidence. I think the market is worrying about AI clobbering the business and I think the market probably knows more than me on the topic. So I am looking for a controlled exit. Step 1 has just happened, via a limit order filling today.

- Sell GOOG ($255). Tiny top slice on this oh-so-blue chip stock. It pains me to sell GOOG but after a >50% rise in 12m now does feel like a good time. It is my biggest single holding, and has grown to exceed 5% of my net portfolio value, which is creating a concentration risk issue for me.

- Other rebalancing away from International Equities and USA Equities towards fixed income

- Buy LLPC (£1.54). Fixed income topup

- Buy UK Treasury 4.75% 22/10/35. Fixed income topup.

- Sell VAPX (£23.21). Reducing International Equities.

- Sell FEV (£4.24). International Brokers doesn’t like this International Equities security (which is a bad sign on margin), and will only let me reduce/close. I’m reducing.

- Sell MSFT ($515). Tiny top slice on this blue chip stock.

- Buy UK Treasury 4.125% 29/01/27. Not great value this, but a very low risk asset – hedging me against the chance of a stock market drop.

- Sell DOM (£1.90). Longstanding position, that I entered at around £3. I’m finally throwing in the towel, and rotating into ADM.

- Buy ADM (£1.25). Admiral Insurance, not Archer Daniels! Topping up a stock I admire, but have only a minor position in. The topup takes it closer to my median holding value.

- Some rebalancing with my ‘property’ portfolio

- Sell CTY (£5.03) – to reduce equity exposure

- Buy NWBD (£1.46) – to swing back towards fixed income

- Buy NTEA (£1.28) – more fixed income

- Sell HMEF (£10.09). I’m overweight International Equities, so I’m trimming this holding.

- Sell VAPX (£22.67). More rebalancing as per HMEF trade.

- Buy NTEA (£1.27). Topping up on UK Fixed Income. By buying this preferred stock/bond. It is relatively cheap versus my other favourites LLPC/NWBD.

- Buy LLPC (£1.55). Not great value, but a stalwart of the portfolio – so I’m topping up.

- Buy UK Gilt 4.125% 29/1/27. Topping up on this Gilt. Another UK Fixed Income topup.

- Bought BHP (£20.80). Topping up on Australian equity too; small nibble, which is just as good because the price is pretty full.

- Buy VUTY (£16.36). Topping up on USA Fixed Income.

September 2025

- Buy Schroder Asian Income (£0.49). I am underweight Fixed Income, of all sorts, so am reinvesting dividends into this old International stalwart.

- Buy VUTY (£16.14). As above, I am reinvesting dividends into Fixed Income – this time USA.

- Buy LGEN (£2.40). A limit order just filled, during a blip downwards in UK stocks. The account in question is my ‘property proxy’ portfolio, for which LGEN is the backbone dividend stock. So this is effectively reinvesting (those 9%) dividends, compounding returns a little.

August 2025

A quiet month

- Close ASY (£5.40 ish). A liquidity lesson. I decided it was time to close out of this smallcap position I’ve had since around 2018 (a tip from Maynard Paton), after trading declines since 2022 haven’t been reversed. My holding was over £25k worth, in a company with market cap of around £230m. And, ouch, it proved hard to sell. I found myself selling in batches of 1000 shares, and one batch I sold seemed to pull the price from £5.40 to £5.10. In the end I have closed out the position at an average price of about £5.40 but it has taken me a month.

July 2025

- Sell AEWU (£1.07). I am reducing my position here – a bit further – in line with the comments below. This reduction is not in the ‘property proxy’ portfolio but another holding.

- Close Fundsmith Equity Fund (£2.30). I’ve had this for some time. Its performance hasn’t impressed. Its five year track record right now is about 6.5% per year. My own 5 year performance is 8%+. So I’m closing this position out.

- Sell RGL (£1.26). Another position that IB has trading restrictions on. I have a small rump holding here, which I’m closing out of.

- Sell FEV (£4.03). I am a bit overweight International Equities. And for some reason IB has trading restrictions on this Fidelity Investment Trust, only allowing me to reduce/close the position. I am reducing a bit.

- Buy IGLT (£9.78). I remain materially underweight UK Bonds so am topping up this Gilt ETF.

June 2025

- Buy SUPR (£0.85). As per comment against RGL I am shifting my property-proxy portfolio real-estate exposure in the direction of this new holding.

- Sell RGL (£1.23). What a nice co-incidence… RGL has just ticked up, at exactly the same time that I’ve been (prompted by some v useful comments to my most recent blog post) reviewing other Property REITs. So in my property-proxy portfolio I’m shifting out of RGL and into SUPR.

- Sell AEWU (£1.07). As per comments above, I’m reducing this position to bring in SUPR into this (property proxy) portfolio at a sensible weight.

- Buy HGT (£4.80). A limit order filled. I am a longtime admirer of this investment trust – which invests in tech software businesses across Europe.

- Sell DOM (£2.60). I have been a dogged ‘buy and hold’-er of DOMino’s Pizza for ages. However I think I must have been reading too many of those ‘rookie mistakes: waiting until you’re right, instead of using Stop Losses’ tips, and I’m overweight UK equities, so it’s time to exit this position.

- Buy VUCP (£34.70), Sell VUTY (£15.86). Call me paranoid, but I think US Corporate Bonds at 5.5% dividend represent a better risk/return proposition than US Treasury Bonds at 4%, currently.

- Buy NWBD (£1.46). Am underweight on Fixed Income in both UK and USA – so am topping up an old favourite pref share.

May 2025

- Slight adjustment to my target allocations – recorded in my Investment Philosophy‘s change log.

April 2025

- Buy L&G Emerging Markets Govt Bonds (£0.40) – topping up on International Fixed Income.

- Buy BHP (£15.95). Topping up; I am underweight in Australian equities.

March 2025

Quite a busy month! As of 31 March here are some key comparables:

- Buy ADYEN (€1400). Limit order filling.

- Buy MSFT ($372). Limit order filling.

- Swap IUSA for HSPX. Modest bit of ‘Sell America’ – replacing an iShares holding with an equivalent HSBC holding. In a tax-sheltered account, so no capital gains tax. HSBC’s ETFs are becoming more competitive, though in this case I am swapping quarterly distributions for biannual distributions – not my preference.

- Swap VFEM for HMEF. Modest bit of ‘Sell America’ and also moving to a cheaper equivalent fund.

At this point in the month, my portfolio is down nearly 5% – driven by US markets falling pretty steeply under Trump-itis. Microsoft is almost down to $375! European equities are up, in the meantime

- Sell AEWU (£1.02). I am overweight UK equities, so am downsizing this position.

- Buy BHP (£19). I am underweight Oz equities, so am topping up.

- I need to free up cash partly for a) a splurge holiday that isn’t paying for itself and b) ISA topups due imminently

- Sell EMIM (£27.75). I’m overweight International Equities.

- Sell VUTY (£16.67). And overweight USA Fixed Income.

- Buy GOOG ($161). A limit order filled, on a dip. GOOG is now on a P/E of 18, despite being expected to deliver 10% revenue growth, and having 30% Op Profit margins. It’s a big holding for me but remains a cracking business which I am delighted to own.

- Sell FEV (£3.90). I’m overweight International Equities now, and rebalancing a little

- Buy DOM (£2.80). A limit order has filled. I am a bit disillusioned with Domino’s but I remain a believer in its long term prospects.

- Buy MSFT ($381). A small nibble, on the dip.

Earlier in the month…

- Buy Wise (£9.10). Topping up. Buying more into a bigger dip. I’m still slightly below my target position size, so am not bothered that my in price is falling as I top up.

- Buy GOOG ($170). Limit order filling. Google remains an incredible business, growing almost 10% a year and making 30% operating margins – which makes it a “Rule of 40%” business. I’m buying on a dip.

- Buy MQG ($225). I am topping up, on a limit order filling on a dip. I am a bit underweight Australia, and Macquarie is a solid performer. I am not following it closely – Buffett would not approve – but trust the brand, the trading metrics and the international cut-through.

- Sell SMT (£9.70). I am overweight International Equities. I have a small holding of SMT in one account; I am closing it, to tidy things up a fraction.

- Buy NWBD (£1.44). I am underweight UK Fixed Income. Topping up, in a tax-free ISA.

- Buy NTEA (£1.20). I am underweight UK Fixed Income. Topping up, in a tax-free ISA.

February 2025

- Buy SAUS (£42). Underweight Aus Equities, topping up.

- Sell GILS (£100). Rotating out of this Amundi/Lyxor bond ETF. In part, because it only pays a coupon annually.

- Buy WISE (£10.50). Opening a new position – via a limit order filling. I have had my eye on (Transfer)Wise for a long time now, and have just bought on a dip. There aren’t many UK PLCs that are ‘Rule of 40%’ and decently profitable. And Mrs FvL loves it….

- Buy IGG (£9.60). Small topup, on a dip.

- Buy HGT (£5.26). HG Tech is a feeder fund ./ investment trust into the Hg software-business-focused private equity firm. The track record is impressive, though obviously no guide to future performance.

- Buy GOOG ($193). I am pushing my boundaries here, because a) GOOG is my biggest single holding b) I am trying to stay tactically underweight USA and c) the bit of USA to be tactically underweight on is tech! BUT there is a buy-on-a-dip opportunity, with GOOG at P/E of about 23x, with >10% annual rev growth. GOOG is a Rule of 40% business, at a P/E of 23. Hard not to buy, DeepSeek, Antitrust or whatever.

January 2025

- Buy NTEA (£1.20). Topping up this holding, in a small rotation into Fixed Income (in which I am underweight).

- Buy MSFT ($417). MSFT has stumbled briefly – I’m topping up on a dip

- Buy IGG (£10.16). Opening this position, again because I am looking for a decent UK biz with growth potential. I like that they are buying Freetrade and think that has upside for them.

- £Buy ADM.L (£26.40). Co-incidence, honest, rotating from ADM (USA) to ADMiral (UK). Opening this position, as I am looking for a quality UK biz with OK growth dynamics, and have been an admirer (ahem) for a while.

- Sell ADM ($51). I’m closing this position too – as per MMM – I’m done with Dividend Champions that are very low growth. Partly, I’m trying to go tactically mildly underweight on US Equities – there is too much bubble chat around.

- Sell MMM ($142). I’m closing this position – annoyingly, the day it just popped 4% to $147 – doh. I’m done with Dividend Champions when they are very low growth – 4% div plus 2% growth isn’t cutting it.

- Sell H50E (£45). I am a bit overweight international equities, and looking to release funds for the imminent tax bill I need to pay.

- Sell VAPX (£20). I am overweight International Equities, and VAPX is not marginable at the moment. I’m trimming.

- Buy DOM (£2.80). ‘Buying on a dip’, I hope. I am a long term holder of this quality-at-a-reasonable-price stock, and it has dipped to an attractive price for no obvious reason.

- Sell DGE (£25.25). The FT has been putting the fear of God into me re the alcohol sector. I’m opting for a Dry January, investments wise, and exiting this position.

- Buy VFEM (£48). IB has just withdrawn margin on VFEM for some reason. I’m topping up in a non-margined account, which gives me more flexibility to reduce exposure with IB.

December 2024

- Buy AHT (£51). Nibbling at this to top up slightly, taking advantage of recent profit warning price slump. I am long term believer in this biz and if it relists in USA that is probably a +ve for me (though -ve for UK plc).

- Sell SOLV ($67). Finally cleaning up this spinout from MMM, which I have begrudgingly owned. Now culling as part of a towards-end-of-year cleanup.

- Buy ULVR (£46.33). Redeploying SOLV’s (US Equity) funds into Unilever (UK Equity) – am underweight UK Eq, and I have ULVR in the same account – no more logic than that really.

November 2024

October 2024

Slight adjustment to my target allocation – as recorded on the change log in my Investment Philosophy page.

And various trades:

- Buy ALU (£2.78). I’m topping up, after a recent price drop – for no particular reason I can see. In fact a few hours after I did this the price returned to £3/share. Very illiquid share, which has pluses/minuses.

- Buy LAND (£6.26). I have recently sold some property and am reinvesting proceeds in public equities. However I want to retain property characteristics. At the blue chip end, that is a choice between Segro, British Land (BLND) and Land Securities (LAND). Based on yield and value I’m plumping for LAND.

- Buy LGEN (£2.27). As per the property sale mentioned above, I am looking for reliable inflation-proof yield. LGEN is a standout proposition here – 9% divi yield, ‘safe’, admittedly very little growth prospect. With 9% I can take 5-6% out as yield and reinvest 3% to track inflation.

- Sell MMM ($134). I stuck by MMM when it was under $100, with a >$6 dividend. Then it spun out SOLV and reset its dividend, and my original investment thesis disappeared. The share price is up to $134 but the divi is only $3, so I have lost the plot. I am trimming the position slightly in my Ltd company account, where company dividends are tax free.

- Buy ADM ($56). Archer Daniels is a Dividend Champion, which is struggling post an accounting scandal. Its divi record remains intact, and the yield is around 3.5%. With projected 6% divi growth, this feels like a relatively attractive topup price. I’m topping up.

September

- Sell SHOP ($80). A longstanding limit order filled.

- Buy NWBD (£1.41). Underweight UK fixed income. This preferred bond has been an old favourite – tho I generally like buying lower than £1.40.

- Buy NTEA (£1.24). As per NWBD, though slightly cheaper.

- Buy VGOV (£16.84). I am slightly underweight UK fixed income. Topping up on my favourite ETF at the moment (largely due to its monthly dividends, which is a dopamine hit).

August

- Buy DOM (£3.00). Domino’s pizza is a compounder. It’s a franchise with a reasonable organic growth model and some decent competitive advantages. Its growth story was interrupted by a spat with its key franchisees but that appears to be behind it. Yet its share price is down near its 5 year trough. Time to top up.

July

June

- Buy Adyen (€11.60). Bizarrely I had a limit order on to BUY Adyen for almost the same figure I had my HL limit order on to SELL. A day after the HL one popped upwards, the Adyen one popped downwards. It must have been an odd order because that price isn’t showing up on Google Finance’s record of the day. I bought into Adyen after a thought provoking piece from Monevator’s Mogul column, which served me well. Since then the stock has maintained decent growth momentum but also been quite volatile – a classic situation of setting limit orders to buy on the dip. That’s what’s just happened today.

- Sell HL (£11.10). When HL popped above £11, as a result of bid talks, I set a limit order a couple of weeks ago to ‘take profits’ (hah – actually to sell at almost my in price). As of 18 June that limit order just filled. A biz like Rightmove – excellent strategic position, unable to articulate a coherent/exciting revenue growth story – and undervalued accordingly. Good luck to the private equity owners, and more shame the public equity markets in the UK.

May 2024

April 2024

- Buy LGEN (£2.52). New ISA tax year – new investments to be made. In a tax-free account, I bias towards higher dividend payers. And right now I’m light on my UK exposure. So I’m topping up Legal & General, a high dividend payer proxy for the UK market.

March 2024

- Sell GOOG ($152). Capital gains harvesting / taking profits / deleveraging, slightly.

- Sell IGLT (£10.50). Capital loss harvesting.

- Buy VGOV (£16.90). Capital loss rotation.

February 2024

- Buy ADM ($53). Arthur Daniels Midland is a long term Dividend Champion. But it’s got into a spot of bother recently with its CFO being suspended/sacked for accounting regularities. Its share price has almost halved. I am taking a punt on there being more upside than downside here, and buying in at a dividend yield of about 3.5%.

24/2/24: Tightening my asset allocation another notch – reducing target leverage from -20% to -18%.

I need a bit of liquidity, for a small private/illiquid investment I’m making. Thus:

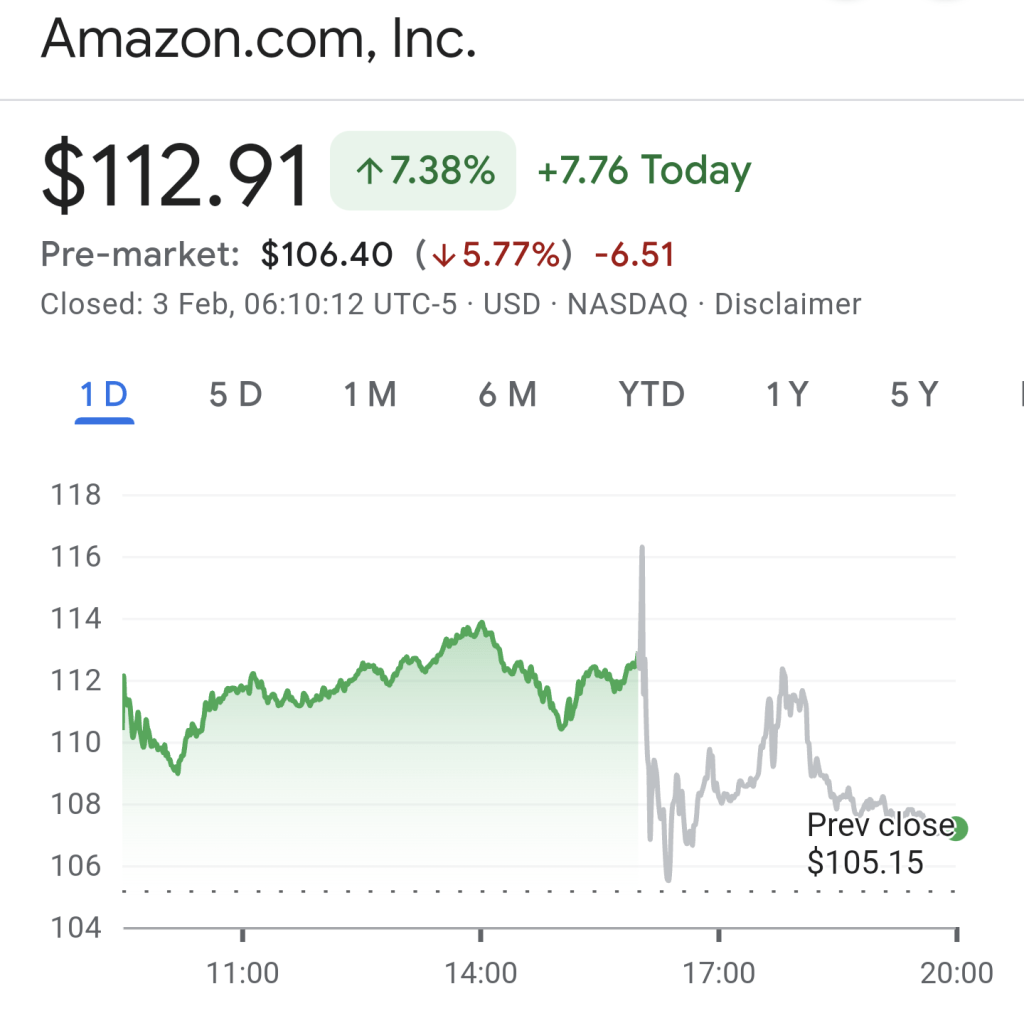

- Sell AMZN ($168). Top slicing a bit of my holding. Every time I have top sliced Amazon before, a year or two later I ‘regret’ it (i.e. the share price has risen well past my top slice price). This time around, with Jeff Bezos taking $4bn off the table in the same month, let’s see what happens.

- Sell GOOG ($141). Top slicing my other large Magnificent-7 holding. As above, generally I don’t like betting against GOOG. But with an anti-trust investigation underway in the USA, there is scope for downside surprise – particularly if the remedy is to unstitch the AAPL relationship.

January 2024

- Sell BHMG (£3.62). I’m closing this macro hedge fund position. Partly to free up funds for an unlisted investment. Partly to crystallise 20% capital losses. This position is a tip I found in the blogs; it has decent long term returns but has dropped almost since I opened my position. The best that can be said about it is that it is negatively correlated with the wider equity market, so my overall NAV has significantly increased since I bought it!

I’m liquidating some assets to raise funds to pay my UK tax bill:

- Sell DIS ($90). Closing out the position entirely. Long term, I am a big believer. Medium term, there are too many headwinds for me to remain comfortable.

- Sell INXG (£13.27). I’ve been offloading index-linked gilts ever since the moron Truss period.

- Sell VUSA (£71). I’m overweight USA already so in any serious liquidity exercise I need to sell US positions – the index will do.

- Sell CTY (£4.04). I quite like this Investment Trust for its focus on dividends. But with base rates now at 5%, CTY’s 5% yield isn’t so impressive. I’m trimming my position.

December 2023

- Buy VAPX (£19.50). Rebalancing towards International Equities.

November

16 Nov 23: Tightening target allocation slightly

- Buy VAPX (£19.47). I am rebalancing towards International Equities, where I am underweight.

- Sell BWSA (£1.13). Bristol & West is trying to redeem/buy out their preference shares. I perceive a risk of being left with an unlisted security if I am not careful so I have sold out of much of my holding early, taking a small (1-2%) loss in the process.

- Buy ALU (£1.50). Microcap business that I quite like – with 7% divi yield and modest growth. I’m topping up.

October

- Buy MMM ($88). A (small, one divi’s worth of) limit order filled at $88. This Dividend Aristocrat is paying $6/yr dividends with reasonable divi cover. A decent yield play.

- Buy RMV (£4.90). Rightmove just fell 25% due to OnTheMarket being bought. I have never been wrong buying Rightmove below £5 so here I go again.

- Buy VAPX (£18.34). Swapping into this, from ABD.

- Sell ABD. I am exiting this International Equities position.

- Buy ISF (£7.46). Topping up UK Equities index.

- Buy NTEA (£1.15). Topping up this high yield pref, UK Income.

- Buy NWBD (£1.28). An advantage of my new SIPP broker is that I can buy this preferred share – an old favourite, not supported by many platforms even IBKR. I’m reinvesting dividends.

September 2023

- Buy VAPX (£19.30). Topping up on an International Equities holding.

- Buy Schroder Asian Income fund (£0.45). Topping up on International Fixed Income.

August 2023

- Buy HL (£7.60). Trying to catch this falling knife. But Hargreaves has a huge new earning stream – interest – and remains the market leader with price-insensitive customers. It’s on a P/E of 12, with a divi yield of 6%. I’m topping up.

- Buy PBEE (£0.72). This is a rare activist holding for me – a penny stock, more or less. It is transitioning from being an overvalued, massive cash burn business into being a solid growth and operationally cashflow positive business. I’m topping up.

- Buy NWBD (£1.29). I have that rare situation of surplus cash in an account which will trade this preferred share – a high yield UK Fixed Income security – so time to top up.

July

- Buy VFEM. I have some surplus cash in the SIPP and need to top up on International Equity.

June 2023

- Sell AMZN ($125). Not a common thing this, but I am going to ‘take profits’ (in fact partially crystallise a loss) on my AMZN stock. I can’t get my ahead around the P/E, given revenues are in fact falling in AWS and the retail business is lossmaking.

May 2023

- Buy MMM ($100). I have just clocked that MMM’s price has fallen to a yield of 5.9%. It is a dividend champion, with 1.5x Divi cover, so I think that divi is safe. I’m making a plump for it, and swapping it in in exchange for DIS which has a divi cover of 1% and a big fight with Florida’s government at the moment.

- Sell DIS ($101). Selling my GIA holding of this – as per MMM trade above.

Apr 2023

- Close ADS (€154). It popped up at the end of March, recovering enough for me to get out of this irritating position.

Mar 2023

- Closing PEPsi. This is an old Limit order filling at $179. Slightly annoying, in fact, because it realises some capital gains and I wasn’t expecting it – I would have much preferred this to be in the new tax year!

- Closing Logitech. Slight change of strategy – I was reinvesting CHF dividends from my main two swiss holdings into Logitech but now Complexity wins, and I’m divesting this holding. This harvests a small capital loss too.

Feb 2023

- Close JPM ($144).

- Margin increase: BHMG.

- Sell SHOP. Well well. Selling one of the knives I caught, for a profit.

- Sell AMZN, GOOG. Small profit taking via limit orders which filled surprisingly ($116 on AMZN!) on an out-of-hours price blip as the earnings release came out.

January 2023

- Sell META ($151). A limit order filled, at $151. Cutting my losses, having recovered somewhat.

- Various administrative swaps – e.g. from VGOV to IGLT – see upcoming blog post.

- Sell JPM ($135).

- Buy ULVR. Redeploying some HSV capital. I’m looking to upweight a branded consumer dividend payer. Choosing between DGE and ULVR I prefer ULVR. I can’t shake the observation that many people I know are cutting back on alcohol consumption, and while I know there is growth opportunity for DGE and strong competitive moats I think ULVR is safer.

- Buy GOOG. Redeploying some HSV capital. I’m underweight US Equities. GOOG has reasonable growth momentum and a P/E of 18.

- Close HSV. Homeserve has been taken private, at £12/share. I’m not thrilled – I saw this business as a genuine UK leader and run by a capable entrepreneur to boot. But I’m happy to take some liquidity and redeploy right now.

- Sell ADS (€140). I am trimming my position, cutting my losses. This stock has ticked up to €140 from a low of under €100 so there is good news but my average price is over €200 so I am not really seeing it that way! In the short term performance will be a problem after the Kanye West debacle. I’ll sit this one out. It helps that I am overweight Intl Equities.

December 2022

- Sell MEUD. With USA dipping, I am overweight Intl Equities. I am selling this holding to rebalance.

- Buy IGLT. Rebalancing out of Intl Equities.

- Buy META. More tiny topups as per Nov.

- Buy BWSA. I am a tiny bit underweight on UK Fixed Income and am reinvesting dividends/coupons into some of my high yield bonds.

November

- Buy META. I think Facebook is oversold. It still has Zuck running it, even tho Sheryl arguably should be running it. It has more control over its profits than most – it could just suspend R&D. And it is on 11x P/E.

- Buy DIS. Feels oversold at $90.

- Buy AMZN. I’m going in…. topping up this big holding, also at $90.

- Sell JPM. I know higher rates are good here but it’s a bank, and not looking as well run as it is famous for. I’m taking some profits.

- Buy ADS. I think this is oversold too. Decent brand and generally well run, on 3.x% divi yield.

- Sell VAS. I am a tiny bit overweight Oz equities so am rotating out of this to fund the ‘buying oversold’ plays listed above.

October 2022

- Sell BGS. As an active fund (boo tss) focusing on Japan (where there is an argument for active mgmt, but which is struggling in ways I don’t understand), I’m not sure this fits in my strategy very well. And it’s done poorly. And I’m overweight on International Equities. So I’m closing my position.

- Buy ADS. Minor topup nibble to reduce my avg in-price, and take advantage of >3% yield – buying a Kanye-West dip.

- Buy various T-bills/gilts. I’m branching out – tempted by the 4-5% yields guaranteed (in local currency, at least) for 20+ years – into actual bonds.

- Buy SHOP. A longstanding limit order just filled. Which reflects this stock hitting record lows. I am overweight US Equities so don’t entirely need this extra holding but there we go.

- Sell INXG. Reflecting more on the carnage affecting INXG, and the time-limited nature of the BoE’s support, I am alarmed to realise that INXG is my biggest bond holding by far – and I have quite a bit of GILI too. Given that it is manifestly failing to do what it is supposed to, I am taking advantage of the 30% price spike since its low last week to rotate out of it and into IGLT/similar instead. I bought (a bit) last week at around £11 and sold (a lot more) today at £14.70.

- Buy IGLT. As above. A point to note – IGLT has over £1.1bn of AUM, whereas VGOV has only £127m. Only comparable ETF for scale is GILS which is around half the size at £670m.

September

- Buy LGEN. I am treating L&G as something of a bond proxy at the moment. Good dividends – an equity exposure with high yields that suits tax-sheltered accounts quite well. No growth prospects per se but something of a play on ‘UK plc’ which I think is oversold right now.

- Buy INXG. Nervewracking. This is a rebalancing buy, but one finds oneself asking whether UK Gilts are trustworthy or might explode. Crazy times.

- Buy DOM. Feels cheap, even without a CEO.

- Buy BWSA. Topping up on UK Fixed Income – but I do want some yield!

August 2022

- Buy ALU. I am underweight UK equities. This smallcap UK manufacturing business is very illiquid but appears to be good value. I’m topping up, as much as the liquidity allows me to.

- Buy DOM. Domino’s pizza is approaching multi year lows. It has a decent growth model – despite rivals – and is suffering from a CEO transition. I think it’s close enough to being a ‘ham sandwich’ business so I’m topping up.

- Sell MMM. I have a venture capital investment which needs funds – and I don’t want to use ‘borrowed money’ for this so I am selling down existing liquid holdings to fund this. With current exposure being 2% overweight into US Equities, I’m selling one of them – in this case some MMM; even though MMM feels quite good value at the moment, I have more 5 year confidence in my tech holdings / other USA holdings.

July

- Buy ALU. Illiquid smallcap stock, potentially oversold. P/E of 5.5, divi yield of 7%+, and reasonable top line growth.

- Sell VAPX. Trimming position slightly to rotate into a UK Equity – ALU

- Sell LCWL. This holding is (simplistically) categorised as USA Equities. And after a day of +4% equity markets, I am overweight equities – particularly USA Equities. I’m continuing to rotate out, moving to my underweight fixed income instead.

- Buy INXG. Topping up UK Fixed Income, as a rotation away from USA Equities.

- Buy VEMT. Topping up International Fixed Income.

- Buy LGEN. I am trying to top up Fixed Income, in a Fidelity ISA. Fidelity doesn’t have any Fixed Income funds that I like and won’t let me buy bonds direct. So I’m cheating, and going for LGEN – which has a large, pretty solid dividend (esp in a tax-free ISA), and a share price that rarely goes anywhere. It isn’t helping my allocation but it will do the trick.

- Sell DOCU. What a roller coaster ride. But I’m out. Rotating out of USA equities, not profitable / dividend paying.

- Buy MDM. Rotating into International Equities, profitable, 6% divi yield, down on its luck.

- Buy DOM. Buying opportunity as CEO has been poached, but I suspect the biz will trade fine nonetheless. Dividends (3.7%) too, yum yum.

June 2022

- Sell ESTC. I’m closing this position. I had a good ride but now when I am a bit overweight USA Equities, I am derisking and rotating into safer /less volatile stocks.

- Buy ULVR. As above – a safer/less volatile stock than ESTC. With a 3.6% divi yield too!

- Sell SPXD. Reducing US equities exposure.

- Buy XAUS. Increasing Aus equities exposure.

- Buy DOM. A limit order just filled – topping up a long term hold. Dominos continues to have reasonable growth (despite loss making competitors Deliveroo etc) and margins and pays a reasonable dividend yield.

- Sell HUBS. I’m closing out this position, as part of an effort to rebalance from US Equities into Australia / UK Equities. This stock is too volatile for my leveraged appetites right now, and as a loss-making tech stock it is likely to remain so.

- Buy HL. topping up an ISA holding – now that the divi yield is approaching 5%, this biz is starting to look like it might be near the bottom. A market leader with a good moat, the best platform in its space, and a commitment to invest more in technology.

- Sell EQQQ. I’m selling a NASDAQ tracker in my ISA. Because I’m long USA equities, and this holding is more volatile than most. I’m recycling into UK fixed income.

- Buy BWSA. More topping up of UK Fixed Income.

- Buy NTEA. More topping up of UK Fixed Income.

- Buy LLPC. More topping up of UK Fixed Income.

May

- Buy BWSA. Topping up UK Fixed Income – a B&W preferred note.

- Buy NTEA. Topping up UK Fixed Income – a Northern Electric (part of Berkshire Hathaway, I think I just learnt) preferred note.

- Buy SHOP. On a dip. >20% revenue growth continues.

- Buy FB/META. On a dip. P/E of 15, revenue growth still >10% p.a..

- Buy AMZN. On a dip. $90bn of top line growth expected next year.

- Buy ADS. On a dip.

- Sell IBKR. To rotate into a couple of dips. I’m closing this small position.

April

- Buy LOGN. Opening a new position (!) – in a Swiss growth stock (I think). This is reinvesting income from my Swiss holdings. I hold Swiss holdings as a substitute for holding Swiss francs. But looking at LOGN’s P/E multiple (15) and growth momentum (profits 5x in 3 years) this feels like a reasonable buy at the moment.

- Buy HL. Averaging my cost price down – with this market leader down 30% from when I first invested. I see the business as relatively inflation-proof and with hard-to-attack market leading advantages.

- Buy PSN. Recycling this housebuilder’s copious dividend back into the same stock.

- Buy SUPP. Buying this bombed out Woodford fund on a dip (back a long way) – averaging down my holding. Small sums involved – for a holding that remains small in value. My thinking being I won’t notice a drop in value of 25% but stand a chance to turn a loss into a profit if the price goes up by 50%.

March 2022

- Sell CMCSA. I have held Comcast for a few years – thinking of it as a well run dependable inflation-proof stock. However now I am overweight US equities, a bit cynical about cable/pay TV in the USA in a world of cord cutting, and ready to deploy into some underweight categories. I’ve exited my position.

- Buy DOM. I’m underweight UK equities and think Dominos is a reasonable buy below £4/share. It has growth, has a good value/low price point that should fare well in inflationary times, and its rivals are going to find inflation bites them. I’m topping up.

- Buy AGG. I can’t believe I was overweight USA fixed income earlier this month – how the markets have swung – I am now underweight USA fixed income and am topping up.

- Sell BRK.B. Much as I love Berkshire Hathaway, and much as it is now outperforming tech stocks over 3 years, I have rather a lot of it, I am long USA equities (which BRK is an almost perfect proxy for), and I need to redeem something to invest in an illiquid thing. So I’m trimming my BRK position.

- Buy SHOP. A limit order filled, topping up this fairly young position.

- Buy MMM. A blue chip stock, and a dividend champion, just down to its (almost) record dividend yield. Almost safe as houses.

- Sell DIS. Trimming this position, to pay for MMM. I’m not sure how much sport/disney+ will be watched with a war on, and Disney has suspended its dividend.

- Sold AGG. Tiny trim, to pay for IBKR. Am overweight USA fixed income so this is a mild rebalance.

- Buy IBKR. Another long term limit order filled, re-entering a position I closed recently after quite a while. IBKR has been fairly range bound. But it isn’t properly cheap yet. Annoyingly I am now a bit overweight on USA Equities, and the fill was in my most leveraged account. But I am reluctant to sell anything at the moment to rebalance.

February

- Buy SCS. This smallcap (£100m) sofa retailer is back where it was in 2018, even though revenues are 20%+ higher. It has >6% divi yield and I think some prospects of continued growth. On a P/E of 8. I think it is good value.

- Buy ULVR. Partial recycling of ABB1 into ULVR, which press comment seems to think is undervalued and I am inclined to agree – especially in a high inflation environment.

- Buy FB ($222).

- Recycling UK Bond allocation from ABB1 (compulsorily redeemed, boo tss) into similar high yield instruments, in my SIPP.

- Buy BWSA.

- Buy NTEA.

- Sell GOOG. I have just sold 10 Google shares, via a limit order tripping. This has happened because Google has just clipped upwards – resulting in Google overtaking Amazon as my largest holding, after many years of threatening to do this – and given my overweight US posture I had the limit order in place just in case.

January 2022

- Sell DIS. I generally love Disney, and the stock has done OK for me. However I am long USA, stubbornly so, and need something to reduce my exposure to. I don’t know Disney well at the moment but suspect that cruises / theme parks / etc are not going to have a good few years, and the streaming bunfight is not value creating for any participants. I’m trimming my position.

- Sell QCOM. I am still overweight USA. I need something to sell. My tech subset feels too large, still, so I’m closing out a blue chip stock that has kept its value but I don’t follow closely.

- Buy ESTC. This database business has been hammered by the spec tech correction. I’m topping up.

- Buy SHOP. I’ve had Shopify on my watch list for some time now. I set up a limit order about a month ago and it has just filled.

- Sell VZ. I’m overweight US equities right now. Which is principally because of my Tech holdings. But I like my Tech holdings! I’m closing the Verizon position, which has been a lacklustre holding for some years now. Reasonable dividend yield, no cap growth – would be better suited to the UK FTSE !

- Buy ABD – Aberdeen New Dawn. I am struggling with my Asia / EM exposure. I am underweight International (a mixture of Europe and Asia/Pac/Emerging). Within International, Europe has done very well recently, but A/P has stagnated. This leaves A/P as something I want to top up into. I don’t buy direct in these markets – I want a fund manager/etf. But my current holdings disappoint. I am rotating out of HFEL Henderson Far East Income and into a fund a friend has recommend (so village, I know) Aberdeen New Dawn.

- Sell HFEL.

December 2021

- Sell BKG. I’ve had Berkeley homes for a long time, without strong conviction. I generally liked the housebuilders for dividends / good value, and when I pruned the portfolio a year or so ago somehow Berkeley survived the cull. Since then its charismatic CEO has passed away and I don’t have a clear reason to continue to hold. Plus I’m a bit overweight on UK equities. So I’m closing my position.

- Buy ADS. A limit order has just tripped – so I am topping up a little bit in this long term hold. Helping me get back to target allocation on International Equities.

- Buy DIS – which has dipped to $147. I am a long term believer in this so am topping up.

- Buy MDM. I am rebalancing a little (see upcoming blog post) towards ‘International’, and Maisons Du Monde is a stock I have a certain amount of time for. It is cheap versus other country peers. And homewares is a sector that has been doing well in Zoom world and I suspect will continue to do well.

- Sell AHT. Reducing position mildly. Taking profits. Rebalancing a little out of UK (as per upcoming blog post).

- Sell EXPN. Perennial disappointment stock; my original investment thesis hasn’t come home to roost (yet?); rebalancing slightly from UK. Reducing position.

- Buy DOCU. Though I am overweight in USA, Docusign has dropped a lot. It is now on a lower revenue multiple than when I entered the position in 2018, so I am topping up a tiny bit.

November

October 2021

- Buy DOM. Buying on a dip. This stock is the plucky little eat-out-stock-that-can – a growth stock, with good margins, beseiged by irrational unprofitable rivals (Just Eat, Deliveroo, Uber Eats).

- Buy ALU. Small topup, triggered by a limit order on a price correction. Share price has doubled over 12-18 months, but profit recovery justifies that. Very illiquid microcap stock so limit orders only practical way to trade.

September

- Buy PEP. I have a longstanding limit order which has just popped. No enthusiasm for buying this but I see it as a broadly diversified long term solid performer.

- Buy ADBE. A limit order popped, to top up this core holding. I chuckle here because my broker has been asking for ages ‘do you want to adjust the limit price upwards?’ and I’ve just held course.

- Sell DOCU. Unusually for me, I had a Stop loss set up for DOCUsign. This just triggered, with Docusign down 12% in the last week, which halved my position. It is only back to June prices, so far from a rout. If it falls the same amount again, it’s back to 12 month ago prices – at which point I might just about consider buying back in.

August

I just re-read Monevator’s “best buy” list, and his piece about Lyxor ETFs. His Lyxor piece’s scaremongering about UK Reporting status is somewhat out of date (as he himself flags) about UK Reporting Status, thankfully. I have decided to rotate some iShares/Vanguard ETFs into their Lyxor Equivalents, mainly to spread my ETF load more evenly – but also to trim fees.

- Buy LCUK / Sell ISF.

- Buy LCWL / Sell VWRL.

- Buy GILI / Sell INXG.

- Buy ADBE. 43x earnings. Great growth. Hard to see who takes it on.

- Buy FB ($363). 26x earnings. And good growth. Know anything better value?

July 2021

- Buy BWSA. Having been (voluntarily, admittedly) ‘exited’ from NWBD, I am looking to recycle the proceeds into some other form of ‘predictable, high yield bond-like security’. Perusing Fixed Income Investor’s list and doing my own research I have settled on this building society preference share.

- Buy PEP. Even as I write this I am struggling to explain why I am topping up my small PEP holding. This is a holding I have been tempted to liquidate in the Great Complexity Purge. However for one reason or another it is clinging on in my portfolio. It is a 4th quartile size however. And it is in a subaccount with only a few holdings in it. Which for random reasons now has some surplus $ in it. I want to use those $. My ETFs are all GBP traded. That leaves me choosing between PEP, DIS, BRK and a couple of others. I’m showing PEP some love. Perhaps if it is a bigger holding I won’t notice it so much….

- Buy HSV. I have a hunch that Homeserve is that rare thing – a decent business in the FTSE-100. And a Buy opportunity. It has reasonable top line growth momentum – albeit profits took a knock in the lockdown – and strong mgmt. It’s a below median holding for me. At a P/E of 19. I’m topping up.

June

- Sell NWBD. Natwest’s cumulative preference shares, paying out nominal yield of 9%, have been a longstanding holding of mine. I learnt about them from Monevator when they cost about £1.20/share (yielding over 7%). Since then they have risen to over £1.50/share. Now there is a tender offer at £1.75/share. I’ve decided to take profits, closing out my holding (tho Mrs FvL still has some).

- Buy INXG/IGLT. My portfolio is reaching record highs. But that leaves me continually slightly underweight on fixed income. I am topping up a five figure sum, taking a bit of extra leverage to do so.

- Buy SAUS. I am underweight, a bit, and topping up.

- Buy HSV. Buying on a dip. Profits for this year are down but brokers estimates suggest longer term momentum unaffected.

- Sell DGE. My Ltd company/PIC is a tiny bit overleveraged, for various reasons. I’m a tiny bit overweight UK equities. Diageo has recovered to 2019 levels (£34/share). I don’t have a clear investment thesis for it – it was a safe dependable FMCG stock, but in a post Brexit world I don’t see double digit growth and think I’m as happy not owning it as owning it. I’ve closed my position. If it dips below £31 I would probably get back in.

May

No material trades this month.

April 2021

The markets have been on a tear this month. I have generally been left underweight Fixed Income, in all geographies, and International Equities.

- Buy INXG. In general I perceive inflation to be on the rise. Inflation is bad for bonds. But not so much for index-linked bonds. The UK is good on these. I have a significant six figure exposure to this ETF but am still growing it.

- Buy Vanguard UK Long Dated Gilts. This fund is almost like a leveraged bond fund. Ouch. So it has taken the biggest walloping in the last two months, and feels like a sensible thing to buy for uncorrelated UK fixed income exposure.

- Buy ASX:VGB. Very slightly underweight. I’m topping up with a nibble.

March 2021

- Buy BGS. I am underweight International Equities. This Baillie Gifford Nippon fund is a fairly new holding, and is down 15% on my entry price. Time to top up.

- Buy EXPN. Experian is a long term holding of mine. It is a market leading credit score brand, with strong network effects – albeit also quite a few tough challengers. Its price is ‘back two years’, even though the business is (just about) growing steadily. I imagine that credit scoring becomes extra valuable in a world of furlough, unemployment spiking, etc. I’m topping up.

February 2021

- Buy Invesco Perpetual Pacific Fund. I am a little bit underweight on Intl Equities. This is an area I am now shying away from direct holdings, and committing to a few funds/etfs. My Pacific fund is one of them and could do with bulking up. I’m adding to my position.

- Buy Santander perpetual bond/pref share. I have a few banking/similar high yield bonds, now all in tax sheltered accounts. As I’m underweight UK fixed income, I’m reinvesting dividends/coupons.

January 2021

- An enormous of amount of buys/sells to rationalise my accounts, as detailed in this blog post about streamlining my portfolio somewhat closer to the idealised ‘one ETF’.

- Buy FB ($266). Can’t quite believe it has a P/E of 25, given 40% compound growth rates in both revs and profits. Yes it is screwing up Whatsapp but P/E of 25 suggests value.

December 2020

- Close DAImler. I have been a fairly long term holder of Mercedes. I like top brands. It has a reasonable dividend yield. It is fairly diversified. But I find myself slightly overweight International Equities, and realising that I can’t tell you exactly what Daimler’s stance versus Tesla is – their electric vehicle push seems late to put it mildly. Are cars going to become the next energy sector – taken for granted by EU regulators and leaving shareholders neglected and suffering? I don’t follow them closely enough. So it’s time to get out.

- Sell XRO. Taking a tiny top slice off this, to make a charity donation with. I am overweight Aus still.

- Buy HEIO. A limit order for Heineken has just triggered, so I have topped up this (still small) holding a little. I remain underweight ‘international equities’.

- Sell ASX:IOZ. I have something of a rump holding here – kept partly because it is not MIFID and thus hard to trade. But I’m overweight Aus and think it’s time to clean this rump up. Leaving my Aus ETF exposure now more MIFID-y.

- Sell SAUS. I have found myself a bit overweight on Aus equities, thanks in no small part to my XRO holding having almost doubled in the last 12 months, so I am trimming. By selling the index, for better or for worse.

- Buy GILS. I am underweight UK fixed income, so am topping up an existing (small) Lyxor UK Gilts holding.

November 2020

- Buy ROche. I have some CHF burning a hole in my wallet. Time to redeploy into a safe, long term Swiss stock. Last time I did this, 10 years ago, was Nestle – which has doubled since. I want a different sector. Pharma, perhaps? Roche slightly cheaper than Novartis, with ~3% yield. Let’s try that.

- Buy INXG. I have some much-appreciated dividends to deploy. And am underweight on UK fixed income.

- Sell RDSB. I have held Shell largely thanks to its dividend yield / bluechip nature, in the face of ESG concerns and the slumping oil price. Since it cut its dividend, for the first time in 50+ years, earlier this year it has been on my Sell list. I’ve now closed my position.

- Buy HEIO. I am underweight International Equities. Heineken has been on my watchlist for a while – thanks to Ian Cowie and Nick Train – and I have taken the opportunity to open a position, at close to €70/share. I value its global brands, dividend track record, and continental European base.

- Buy MKC. I am a bit underweight USA and tho the price seems high, MKC has been one of my tiddler holdings for a while – I’m biting the bullet to top it up.

- Buy PEP. As per MKC.

October 2020

- Buy HUBS. I know a guy who uses Hubspot at work, and he is absolutely raving about it. I’ve opened a position. And then, with the correction at the end of the month, a limit order triggered – almost doubling my opening position.

- Buy BABA. I own a bit of Alibaba. P/E of under 30. More or less unaffected by Brexit, US election (unless USA chucks it off NASDAQ…?). I’m underweight International Equities and this feels like a sensible place to top up.

- Buy ADS. Topping up on International Equities, this global brand based in Germany feels like a reasonably safe place to park some funds. And in a world where exercise/outdoors is more important than ever, Adidas has the winds at its back.

- Sell PRU. I have liked/admired the Prudential brand. But in reality, active asset management, based in London, focused on Asia, isn’t feeling like the right place to be.

- Sell DGE. I’m trimming my ‘UK’ exposure at the moment. Diageo feels like it is in the cross hairs of trade wars / tax rises. I’m reducing exposure a notch.

September 2020

- Sell VUCP. As per VCSH below – rotating from USD/Fixed Income into Intl/Fixed Income.

- Buy VEMT. As per VCSH below – rotating from USD/Fixed Income into Intl/Fixed Income.

- Sell VCSH. I am a tiny bit overweight on USA/Fixed Income. And Interactive Brokers is sabre rattling about increasing margin requirements. So I am doing a tiny trim of a USA/Fixed Income position.

August 2020

- Sell WFC. I have been a long term holder of WFC, seeing it and JPM as two ‘blue chip banks’. I have held on to WFC even after their fraud/selling scandal. I have held on to WFC even as their share price halved this year, along with other banks e.g. HSBC. However now they have cut their dividend by 80%, and Warren Buffett has been selling, I am closing out the holding inside my Dividend Growth Portfolio – one of my almost-rules for the DGP is any cut/cancellation of the dividend triggers removing the offending holding from that portfolio.

- Buy BABA. Alibaba has lost relative ground to AMZN. I am underweight in it. Time to nibble a bit more.

- Buy DOM. The UK Dominos business seems like a rare growth stock in the UK, especially in a world of ordering more takeaway food. On the negative side, it has a bunch of competitive and irrationally-well financed competitors. I am buying (a tiny bit – I am slightly overweight in UK equities) when <£3.20.

- Buy LLPC, 87PN, PMO1 (very bravely). I am still underweight fixed income in all my geographies. I have a weakness for these UK listed high yielding corporate bonds, especially when dividend income has been slashed.

- Buy INXG, VUTY, VEMT, VCSH, ASX: VGB. Topping up my fixed income holdings across all geographies, across my core ETFs.

- Buy Schroder Asian Income Maximiser, Henderson Asian Dividend Income. Two ‘international / income’ holdings that remain reliable on the income front. I’m topping up.

- Close RTN. This stock has been a bugger’s muddle of an investment. I just set a limit price sell at 59p, and IB closed the position at 50p! An ignominious end to an ignominious investment.

- Close AIRd. I bought Airbus just before the pandemic really took hold (or, more correctly, before I noticed it). This was a poorly timed investment, to put it mildly. I’m closing it out.

July 2020

- Sell TW, the UK housebuilder. I have had a ‘runt’ holding here, below my £20k ‘minimum’, and have been trying to decide what to do with it. But I find myself overweight UK, and have heard some colour about the leadership that doesn’t make me a proud shareholder. I’m out.

- Buy ITX, the owner of Zara and other top apparel brands. Another ‘runt’ holding, which I have wavered on whether to clear out (retail -> yuk; disappointing results/dividends; no clear share price momentum) or build a position (great brand; long term entrepreneur holder; not that expensive). I’ve decided to build a position, and have just doubled my stake.

June 2020

ESG is flavour of the month, and has had me digging. I’ve only just noticed that an ESG version of Vanguard’s VWRL, iShare’s SUWS, is in fact even cheaper (20bps) than VWRL (22bps). I’ve swapped half of a VWRL holding for SUWS so I can keep tabs on how the two compare.

Allocation-wise, I have remained significantly underweight (2-3%) equities, and am deliberately not doing anything about it. I feel the market may give way at any moment, and I have plenty enough equity exposure on the upside.

I have also been a bit underweight (1-2%) bonds, and trying to top up into them, in all geographies:

- Buy VEMT. Emerging Treasuries.

- Buy L&G Emerging Markets Govt Bond Index.

- Buy LLPC, NWBD, 87PN, NTEA – various UK corporate bonds/similar yielding about 6%. This sort of predictable income is too tempting to resist at the moment, especially when it is tax-free in my ISAs/SIPPs.

- Buy AGG, BND (non UCITS ETFs – glad I have found a way to buy them at last!).

- Buy VUTY – the UCITS way to buy US treasuries.

May 2020

May felt very benign, as stock markets slowly recovered some of their March losses. I felt like the monster remains just out of sight below the surface though, and didn’t do much.

I did however top up a little bit on some of the best tech holdings, even Amazon and Microsoft despite being at record prices.

I closed out INF and AViva, which were both small positions I had been indecisive about. Different reasons, both.

I was slightly underweight in fixed income so any spare cash (not much of it available these days) was mostly spent on topping up fixed income – VUTY, NTEA, and NWBD in particular.

April 2020

The market has kicked off the month heading down, as wise heads in the US say we haven’t seen the size of the US problems yet.

- Buy ESTC. Opening a position in this cloud software platform, after hearing about it from a techie friend.

- Buy ALU. Topping up, at <70p a share, to bring down my average price (!) and noting that two NED/similar have just bought at this price.

- Buy LGEN. They confirmed they are going to pay their ~13p dividend. At <£2.00/share, this makes them a Buy for me.

- Buy SN. I’ve opened a position in this UK pharma/medical business last year, but it has remained fairly expensive. Until recently. I think medical/health businesses are all quite well positioned at the moment and its share price has fallen (a bit, not a lot) so I’m topping up.

- Buy ADBE. Limit order just triggered. This business is hurting as freelancers/etc are hurting, but it’s a digital businss not fully impacted by lockdowns. And it remains strategically very strong. I’m buying at what feels like a good price, but in fact is a price it reached only 12 months ago.

- Buy HSBA. The BoE has strong-armed UK-based banks into shelving their dividends. HSBC’s (hong kong-dominated, allegedly) investors have marked it down 20% in protest. This feels oversold; it is one thing to sell when a company cancels divi of its own volition; quite another when company *wants* to pay divi but regulator won’t let it. Regulator worried about market stress in UK, which is relatively small beer for HSBC. Now is the time for HSBC to shine. I’m topping up (v modestly), despite my longstanding misgivings on ‘playing with banks’.

March 2020

Last couple of days of March. Markets wobbling but not moving.

- Buy RDSB. Shell has just borrowed $12bn, increasing liquidity to $40bn. It looks like its dividend (£1.88, 11% yield) is going to be paid.

Last full week of March. Feels like Trump (“don’t let cure be worse than the problem”) may have provided support for S&P and FTSE-100 (at about 5000). I have bitten bullet to become an Elective Professional with my Personal Investment Company, removing retail protections, and allowing me to buy some ETFs that are not MIFID friendly.

- Buy LGEN. Feels cheap, no? I am worried about a ‘run’ but they have £400bn+ assets and market cap of 1% of that. Strong trusted brand. I’m topping up.

- Buy ASX: VGB. A non-MIFID ETF that I want to top up on.

- Buy ASX: VSO. A non-MIFID ETF that I am topping up on. Small-cap, which must be risky, but I assume that is priced in.

- Sold VAPX. Rebalancing trade.

Yikes. UK now moving into lockdown- schools to be closing from Friday. I find myself overweight US equities (and bonds), and overmargined – not a great place to be. Slowly fixing:

- Sell VUSA. Reducing exposure to US. [Warning: market timing?!] I don’t think US has seen its bottom yet.

- Close SKT. Outlet mall real estate. I suspect visits to these will be banned soon.

- Sell H50E/VAPX. Reducing slightly overweight exposure to International Equities, via cuts in a Eurozone ETF and Asia/Pac ETF.

- Sell ITX. Inditext, owner of Zara, makes me nervous – especially with its short supply chains.

- Sell DOCU. I don’t like selling this (it’s well-positioned for WFH ) but I am overweight and it is not profitable enough to keep me calm.

- Sold MMM. I need to sell something, even this blue chip stock.

- Bought PSN. I am underweight UK and believe Persimmon is a) selling houses – which will continue b) cash rich c) reasonably well governed d) dividend friendly.

- Close CSCO. This has been on my sell list for ages – in fact I have had a limit order in at $49 (hah!). I hear internet traffic is up a lot in Italy which must help CSCO, but they are capital spend which will be an early casualty too. I’m bailing.

- Close BKNG. This is painful, as I think it is darned cheap – but with travel so hard hit this could get worse.

- Sell TGT. Retailers can’t be the best thing to have.

- Sell IUSA.

- Sell AMZN. Just 10 shares. I *hate* selling Amazon, which long term will be fine, but it has held up well and is my biggest individual holding.

- Sell JPM. Just a few shares. I hate selling this blue chip stock too, esp when it is 40% down. But banks feel risky and I have a big position here.

- Sell BLK. I think Blackrock is a winner, but it is an AUM-driven business and AUMs are clearly down – and could go lower. I’m reducing my exposure.

- Sell VZ. This must be one of the survivors. But I am looking for things to trim and it counts.

- Sell QCOM. This ought to be a survivor too. But I need to trim something and this one isn’t food and it isn’t Amazon!

- Sell PFF. A legacy non-MIFID holding that was, in theory, supposed to be a high yield fixed income play. I haven’t liked it for ages but I can’t ever buy more (under MIFID) so selling is a non-trivial decision. We’ve reached that point – I’m reducing.

- Sell JNK. As per PFF above, at least as far as MIFID is concerned.

Now in 3rd week of March. Many countries shutting down, but not yet the UK. After a Friday 9%+ S&P bump, we are back in correction territory. Trading platforms are showing straint. I am overweight bonds and underweight equities, and gently rebalancing.

- Sell RSAB. Rebalancing out of direct bonds.

- Sell ABB1. A Santander high yield bond. Rebalancing out of such things.

- Buy ISF/CTY. Rebalancing into UK Equities, esp when FTSE is <5000.

The ‘corona virus correction’ is now a full-on ‘covid-19 market meltdown’. Yet, as I write this in 2nd week of March, bonds are firmly up. I’m nibbling away at rebalancing, trying to avoid getting too hurt by falling knives.

‘Oil price crash’ week

- Buy XAUS/SAUS. Rebalancing towards Oz equities (which have been brutally pumelled – especially BHP Billiton, which I hold).

- Buy MIDD. Rebalancing from UK bonds to UK (mid cap) equities.

- Sell ISXF. As per SLXX below.

- Sell SLXX. Rebalancing out of bonds, slightly, starting with corporate bonds.

- Buy EXPN. Digital / information business, famous for credit scoring. Distress heightens need for credit scoring, no?

- Buy RMV. I can’t really see how a market meltdown – that so far at least isn’t hurting the property market – can affect Rightmove. Can it?

- Buy GOOG. A big holding of mine, but I’m topping up (slightly); it’s a digital-only biz, one of the world’s top N brands, and as much in need during pandemics as ever.

- Buy ADBE. Digital only business – increasingly subscription – hard to see how it is affected by market meltdown.

- Buy GOOG. Digital only business. On sale.

- Buy JPM. Definite falling knife risk. Jamie Dimon in hospital/etc. Yikes. But this bluest chip of banks must be bigger than Dimon, no?

- Buy WFC. Definitely a falling knife. Two directors out, the misselling scandal rumbles on. But this is a quality franchise and Buffett is in the wings. 6% divi yield. Too tempting to ignore.

Corona virus correction continues. I need to rebalance towards UK equities. So I did:

- Buy INForma. Information (and exhibitions – doh!) business. Multinational . Rare UK leader.

- Buy RDSB. Shell, at £15. Sounds cheap. I know it’s possibly a ‘stranded asset’ but it is well managed with a good dividend.

February 2020

‘Corona virus correction’ (as it was then) trades

- Buy DISney. Massive brands. On sale.

- Buy MSFT. Just a nibble. It’s still expensive.

- Buy ADS. Brand. Reduced.

- Buy HL. Dominant player. On sale.

I am roughly in balance with my target allocation right now, which lets me nibble a bit more freely.

- Sell DAImler Benz. I have held the two leading German car brands for some time – thinking they have a low multiple for such revered brands, and that the brand will win vs the Tesla disruption. One of these holdings is in a Dividend Growth Portfolio (DGP). Mercedes has just announced a drastic dividend cut – which, as one of my DGP rules, means I am now closing the position.

- Sell CCL. I’m closing this position, as part of my simplifying exercise. Global leader this may be, and cruises must be a long term growth industry. However the scaleability of the model is not great, competition is intense, and CoronaVirus/etc illustrates the negative sentiments that can arise.

- Buy WFC. This bluechip bank has been under heavyweather for years, including a long spell on the naughty step for faking new customers. New CEO recently, but share price remains low – leaving its dividend yield near all-time highs (at 4.5%). Time to top up.

- Buy INF. Topping up on a dip.

- Buy CCL. Cruise line business continues to plod forwards. But share price now lower than when I entered so I am topping up.

- Buy MMM. One of the bluest chips. But keeps missing its numbers and now the subject of rumour breakups. A Dividend Champion – and depressed share price now leaves it at at historic dividend yields. Time to top up.

January 2020

Quite a lot of activity this month but mostly shuffling from one account to another. Blog post to follow..

- Sell RTN. I’m overweight this horror story, but I’ve been convinced its share price would climb off the £1.10 floor. I’ve been right; at >£1.50/share I have reduced my position.

- Sell Wood (John) Group. Miserable share price performance in this holding that my private bank got me into years ago. I’m decluttering my account and it’s time to bail.

- Sell WPP. It’s slowly getting back to the Sorrell era. But strategically I am less and less convinced of relevance of mega agencies in world of Google/Facebook. Shareprice climbs reduce the losses I have been nursing; I’m out.

- Sell BAB. I hold this for very random reasons and have nearly sold many times before. Time to clear out.

December 2019

- Buy ADBE. I am underweight US stocks and like Adobe more than its relatively small weighting in my portfolio suggests. Time to top up (even at record high share price, gulp), a tiny bit.

- Buy ITX. I am underweight International equities. I feel Zara is one of the rare B&M retailers that has a convincing story in an Amazoned world. Time to top up, a tiny bit.

- Buy EL. EssilorLuxxotica is a giant business with a giant governance problem. On the Buffett ‘ham sandwich’ principle, I think it is oversold on those governance concerns. I’m buying, a bit.

- Buy IUSA/VUSA. As last month, I am topping up as part of my reinvestment rebalancing.

- Buy VFEM. I am also somewhat underweight ‘Intl equities’. This emerging market ETF will do for now.

- Buy ALU. I don’t know quite why this microcap stock is so unloved but I still like it so I am topping up.

- Buy AEWU. This unloved UK REIT is delivering >8% yield. I am reinvesting dividends, in my ISA.

- Buy BLK. I am underweight US equities, and need to reinvest dividends. Time to continue building my position in BlackRock Inc; with equity markets on such a tear this can only help their short term numbers.

November 2019

- Buy IUSA/VUSA. I am underweight US Equities and in the absence of any clear stock tips I am topping up the index.

October 2019

- Buy EQN. I’m a customer, via Selftrade, of Equiniti, and it does OK. It isn’t as good as ii/Hargreaves but it isn’t so bad I want to swap. Sticky business, high margins. Growth of all key metrics by double digits. OK dividend yield (2.7%). And P/E of 11. A value buy?

- Sell T. AT&T has been a longstanding holding of mine – but mostly in my High Yield Portfolio. Since its acquisition of Time Warner, and taking on $100bn+ of debt, I have been looking for a way to exit the position. A limit order recently triggered so my position has finally closed out.

September 2019

I’m underweight on UK and US equities, so am taking the opportunity to enlarge some small positions:

- Buy DOMinos Pizza. Market leader, albeit in a fragmented space chased by excessive, irrational capital. Crap CEO now replaced. The next direction is up, methinks.

- Buy SCS. Extending a small position in this very lowly valued regional retailer.

- Buy INForma. Small, new, position in this leading information services business. One of the few sectors that probably does OK post Brexit, I reckon

- Buy ALUmasc. Topping up a position I have held for a while in this microcap business. As a specialist manufacturer of building products there is plenty of downside risk here, but with an Entity Value of .3x Revs and ~5x recent profits I think this is a Buying opportunity.

Pruning the portfolio.

- Sell VOD. Always been a miserable way to create value, and I am finally calling it thus.

- Sell LLOY. Have held for a long time and share price has resolutely barely budged (well, to be fair, 50p->65p->50p). At least there is a 5-6% divi yield. But with recession coming and neobanks having so much capital thrown at them, this feels like it has downside risk.

August 2019

As of 26th August I decided to withdraw all my funds from P2P savings sites. I have had small sums with both Zopa and FundingCircle for years. I took out about half the funds to buy the DreamHome, back in January 2016, and was pleasantly surprised by the ease/speed of accessing my money. But evidently since then the liquidity has dropped – FundingCircle is now citing 92 days to access funds. For the record, my reasoning to get out is as follows:

- Poor liqiduity. Anything like 90+ days is absurd, for the returns on offer.

- Small sums – not justifying the tax/reporting/admin hassle.

- No FSCS benefit. I increasingly think I’m better off spreading funds across FSCS-protected places, and making sure then I max out the FSCS limit. With P2P I was doing neither.

- Unimpressive returns. I’ve been getting slightly better returns on Zopa than FundingCircle, despite FC’s claims to the contrary, but both are paltry – about 5% pre tax. I can and do get better with, among other things, corporate bonds, housebuilders, etc, all of which I can put in FSCS-protected places.

- Business model scepticism. But that is another story. Suffice to say a well-placed social media campaign could sink these players.

Other than that, there’s not much to do this month as dividends are low. However, the bond rally is really eye-opening; a lot of my bond holdings are up >10% on a six month period, and are pushing my overall allocation close to ‘forced sale’ levels.

- Sell VUCP. I’ve taken some profits out of this Corporate Bond holding, which was in an ISA (despite yielding only 3.5%); I’m less in favour of corporate bonds than I was so now is a good time to reduce.

- Buy PSN. I’m tempted by Persimmon. I’ve got a significant holding already, and have watched both a) its high dividends and b) its public humiliation over its egregious CEO compensation. The politicians now hate it. However its recent share price fall seems to represent a buying opportunity and the FT’s Lex column, no less, recently agreed that PSN represents good value. I’m buying, into my ISA.

July 2019

I’m slightly underweight UK equities at present, as the dropping pound boosts my overseas holdings and even though the FTSE 100 is rising it isn’t enough to compensate.

- Sell LLOY. I have stubbornly held on to Lloyds, the market leading UK clearing bank by miles. However it has stubbornly refused to prosper, weighed down by a) legacy tech b) bureaucratic culture and c) political oppression. Right now there is asymmetrical downside risk (ie UK economy droops, Lloyds gets clobbered) so I am closing out my position.

- Sell BT. Not sure why I have got BT – I think originally I took it over from the private bank discretionary portfolio, and then the unrealised capital gain put me off selling it. Now it’s share price has gone backwards by 10 years I can sell at no gain. Ho hum.

- Buy ALU. Microcap manufacturing biz. Shares are dipping, as UK manufacturing shares wilt under the Johnson “no deal nirvana”. P/e of 5-10.

- Buy DOM. Pizza remains the best suited cuisine for takeaway, Just Eat or not. And the Dominos brand and platform remains the best. The only issue is the idiot CEO who has trashed franchisee relations. He won’t last, but he’s making the biz cheap. The brand’s strengths will endure.

June 2019

Context – I find myself underweight on USA equities, for some odd reason.

- Buy ADBE. Market leader – hard to see how MSFT/Google/AAPL attack it – with good growth momentum. That I own none of. Doh. I’ve just opened a small position.

- Buy DOCU. We all use this, right? Yet it’s still small. I suspect MSFT/ADBE/similar will buy it but in the meantime I think it’s on a roll. I’m buying.

- Buy MMM. Topping up, with share prices still in the doldrums.

- Buy GOOG, MSFT, FB. All of which took a bath due to some anti-trust noise emanating from the Trump administration. I view such news as a buying opportunity.

- Buy HL. Hargreaves is a business I love to hate. And, boy, is it taking a whipping. But on the basis that ‘no publicity is bad publicity’, and that it is a market leader in a price-insensitive market, I think the recent share price fall may be a buying opportunity. I’m opening a position.

May 2019

- Buy S&P500 – via VUSA, IUSA in roughly equal measure. I am underweight US equities so playing catchup.

- Buy CXN1. Opening a position in NASDAQ-100 which long term has outperformed S&P, and Moore’s law has enough legs left in it to suggest that will continue.