Well well. It’s the 31st of March and we appear to still be in the EU. Much as I am delighted we haven’t left, this does leave some much-sought-after clarity postponed. More on this later.

The wider world

In ‘mover and shaker’ terms, what’s been going on?

- Mueller reported on Trump’s alleged collusion with Russia. Rather anticlimatically, from a London point of view.

- Trade-related noises continued to emanate from the White House. Without much clarity.

- Apple announced, erm, that it has spent $2bn on TV content. Yawn.

- And UK democracy wriggled and writhed around the incoherent fantasies of Brexit and politics combined.

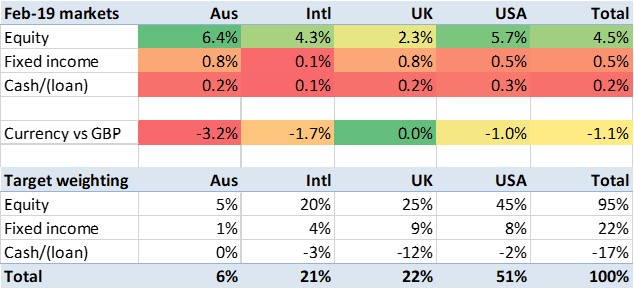

The markets

From a markets point of view, this backdrop felt rather similar to January and February, and sure enough March markets felt fairly similar to January and February markets.

As a ‘no deal Brexit’ scenario looked more likely, the pound declined off recent highs. We are back to £1:$1.30. That was the major currency movement to note; in the meantime the Euro has been declining against other currencies and the AUD is bouncing around in its own electorally-driven world.

Bonds had a stronger month than normal. The logic here evades even an avid FT reader like me. I think what matters is well put by Monevator:

A quick way to be called a moron by people who know more than they understand over the past 5-10 years has been to suggest that bonds still have a place in most portfolios. A wealth-destroying crash was “obviously” imminent, you see.

But markets often move in the way that surprises commonplace assumptions, and that’s certainly been true of bonds.

Monevator’s Weekend reading: Oops, bonds did it again, 22 March 2019

This lot left March markets looking as follows:

Looking back 12 months, March saw equities return (admittedly briefly) to a positive return, leaving the Q4 20% correction very much behind us – though equities haven’t yet recovered to the heights of last summer. In the meantime bonds, which have been losing value through 2018, are now up about 5% from their Q4 nadir. A blend of both would, as so often, have stood an investor in reasonable stead.

My portfolio

The March market movement, weighted for my target allocation, was up 2.6% (0.75% from FX, the rest from the leveraged play on equity/fixed income). My portfolio lagged this slightly, rising ‘only’ 1.9%. But for the year to date, and indeed over 12 months, I’m up 9%. That’s despite the Q4 correction setting negative records.

Continue reading “March 2019/Q1 review”