Regular readers will know what a fan I have been of margin lending from Interactive Brokers. No longer. If you’ve read my other posts (like this or this or this) on margin lending, and are interested in exploring further, make you read this post before you do.

Why I used to like IB’s margin loans

IB offers credit secured on its portfolios, priced very competitively. This provides remarkable flexibility, at a low price. I have been an eager user, enjoying how I can stay (more than) fully invested but still find funds fast to make an unexpected angel investment, pay for a home improvement project or settle a tax bill. In reverse, I can repay instantly and very flexibly, and I can convert either cash holdings or loans from one currency to another instantaneously.

These advantages apply both to IB’s loans, but also to the portfolio loan I have from my private bank. However IB is much easier to operate, thanks to their excellent online platform and reporting. And IB is cheaper. So IB has been my ‘go to’ lender.

You told me so

Smarter people than me have warned about lenders’ judge/jury/executioner abilities with margin. The scenarios painted here are where IBKR/etc deem particular securities no longer to be acceptable collateral. This does happen a certain amount. Historically IB has always given a few days’ notice, allowing customers to re-organise funds and portfolios as appropriate. My private bank did it to me once over 5 years ago – with my biggest holding too, the rotters – but never since. But while I know this risk is real (see example below from Nov 2022), I have never worried too much about it – nearly all my IBKR holdings are superliquid, UK/US stocks/ETFs.

Some of those same smarter folks have suggested that I consider replacing some/most of my margin loan with a mortgage. While this wouldn’t necessarily be any cheaper – especially if I mortgaged my second / rental property not my primary home – it would give me control and certainty. With a mortgage so long as I meet the repayments the lender can not change arrangements unilaterally and certainly not overnight with no communications. I have understood the wisdom and logic of these suggestions, but a combination of the faff/hassle of setting up a mortgage and the confidence/trust in IBKR over the last 10 years have seen me stay put with a margin loan instead.

The new reality – don’t touch IB’s margin loans

Those days are now gone, suddenly. As of the first week of May, IBKR’s margin methods have completely changed. Why? It’s hard to know, as IBKR’s customer communication has been terrible and there is no clear rationale.

What appears to be happening is that UK/EU personal customers (I haven’t heard any issues from US customers) can continue to use margin loans, but they can not withdraw any funds from a margined account. This is like your current account having an overdraft but not allowing you to withdraw any funds from an ATM, or move funds to another account, while overdrawn. Your uses for that overdraft have just been drastically reduced. In fact it’s worse than that, because I can’t even decide to take money off the table – as any positions I liquidate must repay the margin loan before I can access any cash myself. This sucks.

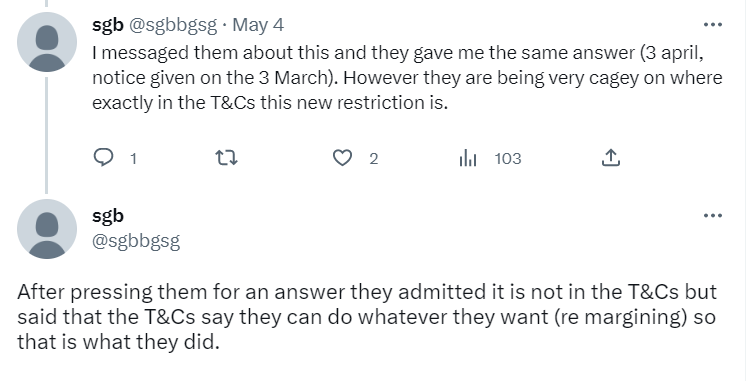

Customers have had no warning of this. Some customers on Twitter have mentioned some IBKR customer support reps citing new T&Cs which took effect in early April, which were notified in March. Aside from the fact that I can’t find these notifications, the more telling comment was this one from an experienced IBKR customer (where IBKR are ‘them’) on Twitter:

It isn’t at all clear why IBKR has changed its approach here. Conceivably, it is under some form of financial distress – though I don’t see any evidence of this and there is no difficulty using margin loans within the existing account to make additional investments. Alternatively, perhaps there is a regulatory angle in the UK/EU – this is possible and regulators don’t like their regulatees explaining to their customers their reasoning. Twitter chatter has wondered if this is just a vanilla cockup, and their systems will spring back to normal before long – I think the exchange with @sgb shown above suggests this is now unlikely.

My Ltd company account still has its normal capabilities. The Ltd can withdraw funds from an IB margined account as normal. Sadly this isn’t too much use to me because I have limited capacity to pull funds from the Ltd company into my personal name – for EIS-eligible angel investments for instance. So while it is nice to know if I was really stuck I could access liquidity from the Ltd, and that IBKR hasn’t totally lost its liquidity marbles, what I really want is that capability in my personal general (not tax sheltered) investment account.

I just lost $1m+ liquidity overnight

This leaves me with several accounts which should have lots of space margin capacity, which I can’t access funds from. One of these accounts, for instance, has the following vital statistics:

- Net liquidation value: £200k

- Net cash/(margin loan): (£40k) (split roughly 2:1 EUR:GBP)

- Total stock: £240k (roughly 60:40 US stocks: UK stocks)

- Initial margin: £70k

- Available funds: £130k

This account has ~£130k of available funds – i.e. I can buy a further £130k of securities, amounting to over 50% of the net liquidation value of the account. Until last week, this would have allowed me to withdraw theoretically a further £130k; in practice I wouldn’t have risked this, but I’d have thought nothing of dipping into the account for say £20k. Now I can’t dip into the account at all. If I want to access even £5k I will need to first sell at least £40k of stock.

This account is only one of several. Across all my IB accounts I have well over $1m of available funds, which in theory I could have withdrawn. Now I can’t withdraw even $10.

Why I suddenly appreciate my private bank

I have long agonised over why I bother with my private bank. The service is lousy, the investment returns are poor, the online platform is rubbish. And the fees, oh the fees. I could go on.

However, one of the reasons I cling on to my bank is that I can talk to somebody. And, it offers margin loans too (more expensively than IB, and with no easy currency convertibility). These advantages are suddenly very much to the fore.

Suddenly, paying 50-100bps more for the margin loan with the private bank feels much better value. They are giving me a proper margin loan, one that I can use for various purposes – including paying a tricky credit card bill if I need to. Heck, even some of the egregious advice/custody fees are starting to feel like a price well worth paying for having a relationship where I know there would be at least an email and probably a phone call too before anything unexpected happened.

I haven’t explored the mortgage options with my private bank, but I am sure they have some. I know Coutts has several useful-looking mortgages. But with rates still rising I am not keen. And while the cheapest mortgage would be against my primary residence, I would have some explaining to Mrs FvL to do if we went from ‘no mortgage’ to ‘mortgage’ on the roof over our heads, and if you’re explaining, you’re losing.

What do I do next?

As at the time of writing, the IBKR ban on liquidity isn’t immediately stopping me do something.

If I wanted to make an angel investment any time soon, my normal ‘go to’ funding source was an IBKR account. No longer.

I still have my margin loan with my private bank. The available funds there are also over 50% of the portfolio I have with that bank, so if I need funds quickly this remains an option – admittedly an option which I am paying over 6% cost of funds for right now. So I have access to funds if I need them.

However, right now I don’t have any IB accounts which are close to being ‘in the black’. My various IB sub-portfolio have the following key margin metrics:

The one which is closest to being ‘cash positive’ has a margin loan of 15% of the value, and available funds of 55% of its value – this is the fund cited earlier in this blog post. I have another portfolio with an LTV of only 14% but a much lower level of available funds, due to some of its holdings not being suitable collateral according to IB.

In aggregate, I have plenty of capacity at IB. For instance I could (until last week) have used some of the 39% available funds in the 28% LTV account (third in the table above) to fully pay off the margin loan in three of the other accounts. But I can no longer do this, because I can no longer pull any funds out of any of these subportfolios until the margin in that account has been repaid.

If markets tumble, via another Moron Moment or similar, my most exposed account is probably the 2nd one in the table – with a 34% LTV and spare capacity of only 28% of the stock holdings. If I want to bail this one out, I can’t even use dividends from subportfolio A to pay off the margin loan in subportfolio B. Instead I will have to find some non-IBKR funds to do so. This changes the game.

I should clarify that I will have several other accounts at other providers, with no margin loan. Though I can’t touch my pension, and won’t touch my ISAs, I have General Investment Accounts outside both my private bank and IB that I can liquidate if I have to. I’ll realise capital gains/losses, I’ll have to wait a few days for funds to transfer, and so on, but I can do it.

I have been making quite good progress at reducing my margin loans, which have shrunk by considerably more than my income over the last two years. But it would take at least 4-5 more years to pay it off completely, without any very unexpected windfalls. And I wasn’t planning to pay it off completely. I had wanted to reduce it to a modest but sustainable level.

I’m still reflecting on the best course of action, but I think I need to restrict my margin lending with IB to only one or two subportfolios, and run the other ones with some level of cash buffer. That is not my preferred arrangement but would be a bit more flexible than what I do now. I am also going to pull my target leverage level down a couple of points – see my historical record here.

Lastly, I can’t quite decide how this changes my outlook on my rental flat. On the one hand, it is another nail in the flat’s coffin because if I sold the flat, the equity released would be enough the margin loan on several IB accounts. On the other hand, the flat would be easily mortgageable, which my IB portfolio no longer is. So maybe I should keep it longer, as collateral that I could raise funds against. Decisions, decisions.

Comments are very welcome, especially from those of my readers with experience of margin loans. Are there any other providers who can hold a candle to IB who would offer good portfolio loans? Anything I’m missing? Anything you’d do in my place?

Ouch. I have always been a big fan of offset mortgages and have them on all my mortgaged properties (they are all paid off, but I still have the line of credit should I wish to use it, for the life of the loan at least). Often the interest rate is not as good as the best “less flexible” mortgage available, but the flexibility to withdraw or deposit cash penalty free on a whim to take advantage of other opportunities is well worth the entry price. Obviously if you aren’t using the credit, there is no cost at all as there’s no interest accumulating. If you’re going to take out an offset mortgage, you might want to give the illusion that you’re not going to pay it all off immediately or the bank might think there’s not any profit in it.

It will vary from product to product and bank to bank, but typically, the available credit you can withdraw is only the amount that you have previously overpaid relative to the monthly scheduled payments. So assuming you took a mortgage for 100 and overpaid the full amount on day 1, the amount you could withdraw that day would be 100, but in year 30 (assuming a 30 year mortgage), the amount you could withdraw might be closer to 0. You could always remortgage later if needed.

They were always very popular in Australia, but I did manage to track one down at a high street bank in the UK (but they were not really widely used / advertised there when I was looking circa 2004). In Australia, the overpayment balances just sit in your other normal bank accounts which can be linked and “offset” against the mortgage interest calculations each month. If you need the cash you just use it from the linked account. Very transparent and easy. In the UK, to overpay and re-withdraw later was more cumbersome – overpayments had to be made into the mortgage account (which I could not withdraw from directly). To withdraw money, I had to call up and speak to someone, and they were asking why I was taking the money etc, so the process was not as fluid. Still worked, but not as seamless as in Australia. In the UK, I used the private banking arm of a high street bank (it only cost £10 a month at the time from memory – makes the whole process a lot less painful).

LikeLiked by 1 person

Damn that’s not good new, I was planning to use some margin soon for liquidity for a property purchase.

Is that not just the annoying restriction which the EU accounts have had for a year or so, where you can withdraw money on margin, but the balance of the particular currency you are withdrawing has to be positive? (it does not sound like it, but I want to double check)

LikeLike

I don’t think so. Enough of us have reported problems this week and none of us can obtain funds.

LikeLiked by 1 person

Very sorry to hear this has happened and glad you have plenty of options for dealing with it. I think your special sauce was always your massively diverse capital base versus these risky broker margin loans.

Obviously it’s telling you to suck eggs re: staying aware of a liquidity mismatch. For example you mention selling the rental flat. At a time of distress (when perhaps you’d need it most) that could easily take several months before you get the cash, even with a haircut. But you know all this. 🙂

Re: why they’ve change the rules, I have no insights but if I had to guess I’d suspect it’s something to do with the general ‘run on cash’ in recent weeks re: the US bank failures. If you look at Schwab over in the US, it’s suffered some market distress as customers have moved cash (which its business model was partly predicated on earning a turn on) over the money market funds, or off-platform altogether in light of the banking woes.

I haven’t at all studied Interactive in detail, but I could well imagine the smoking gun emanating from that sort of direction.

LikeLiked by 1 person

Yes I have wondered about that.

Though their recent results show they are in fact sitting on a lot of cash – they have roughly doubled their revenues/profits from interest earnings (like HL/etc).

And this rule change seems to be UK only.

To me it feels compliance/regulatory-driven. Possibly UK regulators have tightened up on margin rules or are leaning in hard (given the ‘run on cash’ effects) and IB has just decided to tighten up accordingly.

LikeLike

I live in Canada where margin loans against stocks are as common as they are in the USA. No broker in Canada, to my knowledge, has ever prevented the withdrawal of cash from a margin account, and Schwab in the U.S. certainly hasn’t. The issue has absolutely nothing to do with the banks in the U.S..

LikeLiked by 1 person

This very much looks like its driven by UK regulations (or IB’s changing interpretation of them) given you can still withdrawn from your limited company account. It also suggests there may be a solution in getting IB to categorise you as a MiFID Professional rather than Retail.

For European accounts they explicitly say “IBKR Ireland and IBKR Central Europe accounts are not allowed to withdraw funds on margin due to regulatory reasons”.

The workaround in Europe has been to short a stock, get credited cash proceeds from the short, withdraw this cash and then close the short. That doesn’t help you if the cash proceeds will first go to paying down your existing margin loan.

However, the further workaround is to short a stock in a currency different to your margin loan. Cash proceeds in say USD will not be used to repay a EUR margin loan so you can withdraw the USD. That leaves you an additional margin loan in USD which you can then convert to EUR to consolidate into a single margin loan.

A lot of messing around and IB’s communication has been terrible.

LikeLiked by 2 people

I’m sure the regulatory/oversight angle comes into the picture, but the question is why a change or what’s prompted a more cautious interpretation *now*? The banking mini crisis seems a clear candidate to me.

Would defer to any industry insiders with special knowledge though. 🙂

I suppose the Edinburgh reforms might be making themselves felt in some way?

Timetable:

Click to access Edinburgh-Reforms-Timetable-01242023.pdf

LikeLiked by 1 person

This really puts me off using my IBKR account. I used to trade options, but liquidated to buy property, and am focussing now on ISA and Pension contributions into passive ETF.

However I was considering putting a new small grub stake in, and am considered about the safety of the funds. Think I’ll stick with Boring Vanguard

LikeLiked by 1 person

Too many people are worried about Sharpe ratios and Max Drawdowns when in reality the biggest threats to investing success are: your own emotions, politicians, governments, new rules formed by the aforementioned (see MFID, cookie law etc), brokers, banks, fraud and theft. Likely in that order.

LikeLiked by 1 person

Thanks for the warning on this. I’ve been relying on having the IBKR margin loan available for liquidity purposes as and when required. I tested it last year, and would have been blindsided if I weren’t following your blog. Pretty shocking change of terms that should be communicated very clearly.

I’m now wondering whether I should move my whole portfolio (ex ISAs and SIPPs) off IBKR to a bank, to get the margin loan capacity. I’m reluctant to pay the management fees and don’t really want the hassle of moving, but I am deeply disillusioned by the way IBKR has made this change and failed to announce it clearly.

LikeLiked by 1 person

So for now there is a ‘workaround’ – as described by @platformer above – which I tried yesterday and works. So while you are right to be disillusioned – as am I – there is still some access to liquidity in fact.

LikeLike

I would caution against “work arounds” at IBKR. They want you to trade and follow their terms. They are ok with some low activity accounts as long as the amount is high enough, and they are definitely not ok with wiring in, doing fx and wiring back out. They are also not ok with holding currency in their cash yield with low trading volume and a low number of positions. If IB’s system flags your account, they are known to set accounts in liquidation only and close accounts without explanation or warning.

LikeLiked by 1 person

Some guy took 1B from FTX using the margin-buy-wash trade-margin-withdraw trick. He was trading mobile coin so I don’t see the relevance but I’m not infallible like the regulators

LikeLiked by 1 person

Got caught with the rule change this month. Rather pis*d. UK resident. GBP is my base currency and wish to withdrawal in GBP. Wonder if anyone has converted the margin to loan to another currency (eg euro; sell euro/buy pound) and withdrawal from positive pound cash balance despite overall account in the red?

LikeLike

That will probably work, though note the cautionary note from @platformer before you do this too often

LikeLike

It may be possible to request a withdrawal in GBP even when you only have a positive USD balance. IB will autoconvert it to GBP (and not even charge the 2bps fee). I have not tried this before though.

BTW it wasn’t me warning about workarounds. I don’t see why IB should care when they are earning margin interest but maybe they will…

LikeLike

Oops I meant to say @pro’s cautionary note, but @platformer you have been very helpful too!

LikeLike

Can anybody confirm successfully withdrawed cash while the account was overall negative? If so, which technique did you use? Thank you.

LikeLiked by 1 person

Confirmed. Borrow enough eg CHF to buy enough eg GBP to make GBP positive. Then withdraw GBP. Then buy back the CHF.

LikeLike

Made a comment earlier but didn’t seem to appear.

Was saying that I haven’t been impact because I’m a professional under MiFID. So while it may be that US banking woes triggered the specific timing of this move, I feel this was coming at some point. Essentially the trend for pointless, expensive regulation of retail continues apace.

I’ve said before that I think a private bank is a far better option than the likes of IBKR. In my case JPM was actually cheaper than IBKR but that was mainly because my collateral was safer macro hedge funds not highly volatile equity ETFs, hence I received a lower margin rate. Even if it was more expensive I would still have gone with JPM. All the focus from personal finance blogs seems to be on cost cutting (or tax avoidance). In my view, penny-wise and pound foolish.

LikeLiked by 1 person

Thanks – this is helpful context. Can you confirm (1) that you are a UK Professional Client under MiFID rules and (2) that you can withdraw in all currencies?

I might considering switching to professional client if that is the case. The overall requirement are not that stringent.

LikeLike

IBKR recategorised me as a Per se Professional client, not an elective professional client, under COB3.5 a number of years ago. Not certain if the differentiate for this issue. Don’t use IBKR much but have done 7 fig USD and GBP withdrawals with no issues.

LikeLiked by 1 person

There’s a discussion on the IBKR subreddit about using a box spread to achieve a margin loan and the fact that our Continental neighbours have had to put up with IBKR’s ever-changing rules.

As for me, I’ll send a stern email to customer support and then twiddle my thumbs, since I don’t see any good broker alternative for my situation.

LikeLiked by 1 person

New from British bank with blue eagle on margin loans / portfolio financing. From Nov2023 they require assets/collateral of £3m+ before they would consider lending against. I was paying BoE + 2% on loan (& 15bps on collateral). Unfortunately it’s au revoir for me. Looks like releasing equity from property might be the best solution…

LikeLiked by 1 person

I’m surprised no one has suggested using futures to get your leverage. You’re guaranteed to get libor + zero financing. The cost of rolling is a few bps a year which is way less than the premium you’re paying now. It also has the benefit of converting divi tax into cgt. Or into no tax if you spread bet it.

LikeLiked by 1 person

Hello Ben, I think the issue isn’t leverage as such. Everyone seems to be having trouble figuring out how to access liquidity when they need it. Sometimes accounts are not leveraged. I have a case where I’m using interest rate futures to hedge against rising rates. Cash is available in the F account, but it’s posted as collateral and cannot be withdrawn, even when my Available Funds are more than enough to cover a tiny withdrawal. The new rules don’t allow you to have a negative balance in your base currency in the securities account (hint: if you trade futures you have another cash account to withdraw from if your futures moved the right direction). I suppose you are correct that if you have a leveraged portfolio then it would make more sense to do it with futures because you will have your cash account funded with minimal cash posted to the F account to hold your futures. Just to note that with futures your exposure is marked to market daily, and the amount of cash to be posted as collateral changes daily. If you’re dealing in foreign currency, it gets pretty messy with tax accounting.

LikeLike

Hello. First time posting here, but it’s worth it. I do believe it is the regulators elevating supervision and scrutiny of liquidity risk management practices at all brokers. And, yes, IBKR UK has every right to make these changes to protect its clients from sudden runs on cash.

All broker dealers in the UK received this letter from the FCA back in January:

Click to access wholesale-brokers-portfolio-letter-2023.pdf

IBKR UK is doing the right thing by introducing some friction for provision of liquidity. The new rule seems to be that your base currency being GBP has to be funded before making a withdrawal. You can fund with a negative USD balance, and it would work. Presumably, it’s easier for IBKR UK to access credit lines with its US parent for its own liquidity needs in times of stress.

To quote the FCA letter:

“Over the recent period we have also particularly focused on the subset of clearing brokers that face heightened liquidity risks as a result of having to post collateral to clearing houses at short notice to cover their positions before having been paid by their own customers. During these periods, we found that some firms’ liquidity risk management and stress testing was not fit for the current market environment.”

“The structure of financial markets has changed a lot since the last major downturn, with a changed role for banks, the growth of non-bank finance, and often a reduction in liquidity in times of stress. It is plausible that the next two years sees heightened systemic risk and episodes of market stress, as we have seen in energy, metals and government bond markets in 2022. Boards should consider this context and reflect how their business models may expose them to risk, and how this can be mitigated.”

Regards,

Zaid

LikeLiked by 1 person

Excellent comment, thanks.

I am slightly in the dark about how IB’s new approach actually helps them reduce risk but as you say it is friction and maybe that is enough for now at least.

But that Dear CEO letter is a pointer and the timing fits. Thanks for highlighting.

LikeLike

Liquidity is always withdrawn when you most need it. Having been burned during the covid crash (forget trying to buy more on margin – I was worried about being margined out and the vague communication from IB made things worse – and impossible to clarify as all lines were busy). In the end, to avoid disorderly liquidation, I pre-emptively de-leveraged creating significant losses.

I still use margin, but judiciously and since last year, actually eliminated margin and built up a large cash/bond position with a view to investing if there is a downturn/recession caused by the rising interest rates.

LikeLike

That’s unfortunate. Maybe it had to do with Brexit or some sort of regulatory change. Good thing your had other options.

No two brokers are alike. IBKR also won’t lend against stocks with less than a $600 million U.S. market cap. Bank of Montreal will lend against stocks with lower market cap than that. Plus the instant transfers to your regular chequing account or even MasterCard or Visa are nice, but the bank is quite a lot more expensive. I maintain a margin account with both.

I think it’s pretty standard with any margin account that the bank can change the margin rate or even call all or part of the loan even if it the account has sufficient margin, at any time and without warning, though.

LikeLiked by 1 person

[…] I wrote last month about trouble on the margin loan front, with IB. In response to that post I had the following comment from Hackney Boy: […]

LikeLike

The regulators probably changed the rules, making it harder or more expensive to comply, and I imagine Interactive Brokers adjusted their offering accordingly.

I don’t think the problem is with Interactive Brokers. I think that the U.K. regulators simply don’t like the idea of mass-market loans against securities, being offered to the general public.

Apart from the Interactive Brokers exception, it seems you need to be well-heeled to qualify for that kind of a loan in the U.K..

LikeLiked by 1 person

£ is my base currency. Converted my £ margin loan to euros so my £ cash balance is positive. (Sold euros to buy £) Then able to withdrawal my positive £ cash .

LikeLiked by 1 person

[…] With interest rates as high as 6%, there is very little advantage in leverage in a world where returns average 8-9% and dividend yields are around 3%. So while I have resisted (fortunately) an abrupt sell-off to reduce my leverage, I will continue slowly to bring my target LTV down – to at least 10% and maybe lower (over the next couple of years, I expect). I don’t see it going down to zero though, as the flexibility that margin loans provide remains something I still value significantly – even though it is not what it used to be at IBKR. […]

LikeLike

I’m in the process of moving some portfolios to IBKR, drawn by the lower Fx fees and availability of margin loans. I spoke to them on the phone before moving funds and they confirmed margin loans were withdrawable as cash for me as a UK based investor. Like others, I’ve found this isn’t the case.

Now we’re some months down the line from the original article, what’s the recommended workaround for this? A margin loan would be very useful for liquidity.

p.s. I am recognised as a professional investor by other institutions and meet the EUR 500k+ criteria etc set by FCA if relevant.

LikeLike

The workaround, for a GBP-denominated account that you want to withdraw GBP from, is to buy GBP first, using e.g. EUR, USD, etc to do so. You can withdraw a positive balance of GBP even if your overall net cash position (because of those borrowed EUR, USD, whatever) is negative. After the withdrawal, I usually buy back the EUR, leaving my GBP balance negative.

LikeLike

[…] view, by source – where you can see I used my Interactive Brokers margin loan (despite it being an annoying faff these days) to raise cash in a […]

LikeLike

can IBKR IE clients withdraw from a positive currency if another one is made negative by a margin loan?

LikeLike

Yes, in the base currency of the account. I’m not sure about another currency.

LikeLike

ibkr just responded to me about this today and said it isn’t allowed because it is still withdrawing cash in margin. maybe the rep was wrong but it sounds such a loophole has been taken out ? in Switzerland he said you can do it, like other global Ibkr accounts but nowhere else in the EU. it is very odd..the government doesn’t want you to use leverage indefinitely as a line of credit which makes moving to Europe as a resident somewhat difficult if you don’t plan to sell investments before spending them.

LikeLike