I’ve had quite a lot of culture to enjoy in February.

Aside from some travel for the Six Nations rugby, I’ve been to two shows – one in London’s Royal Opera House and one on the south coast.

Both events were either full or practically full. Covid feels fully behind us now. But the prices have stayed with us.

I was struck by the demographic difference between these two nights out. I know, I know, the demographics of opera and concerts are not a fully reliable guage. But I was practically the youngest person in the audience at Poole’s Lighthouse concert hall, whereas I felt 2nd quartile old in London’s Royal Opera House. Is this a reflection of where the money sits – with retirees only in Dorset, and with well-heeled workers and tourists in London? A rhetorical question, for now.

Markets in February 2024

The USA stock market continued to be the main story in February.

Though if you were paying attention, the Japanese market has been setting new records too – the Nikkei 225 is up 20% Year to Date.

It wasn’t just Japan that’s booming, with Asia ex Japan up 4.5% in February itself. Over in Europe and Australia we had much less excitement; Europe ex UK was up 2.8%, Australia up only 1.2% and the misery-guts UK’s market rose only 0.5%.

My performance in February

Sadly I have almost no exposure to Japan. And the index I track is Asia ex Japan. It is very hard to find a good ETF/benchmark for ‘Asia’ – any suggestions would be very welcome. Ideally I would have a choice of one which excluded China (but included Japan) and one which included China (and Japan). As it is I tend to track ‘Emerging Markets’ (which I assume excludes Japan) or Asia-ex-Japan. So sadly no 20%-in-2-months uplift for me.

Even excluding Japan, the markets I’m exposed to rose 2.6% on a constant-currency basis in February. The currencies then rose an average of 0.5%. For all the talk of the Magnificent 7, they haven’t been that magnificent for me. GOOG is down below $140, from a January peak of $155. MSFT is roughly flat in February. Thankfully AMZN has helped me – up 15% from $155 to $178. But Berkshire Hathaway is not one of the 7, and yet has grown 6% – perhaps boosted by the attention my January blog post gave it.

My portfolio’s performance of +2.6% was a slight lag to the markets I’m in, allowing for currencies. My GOOG position hasn’t helped me.

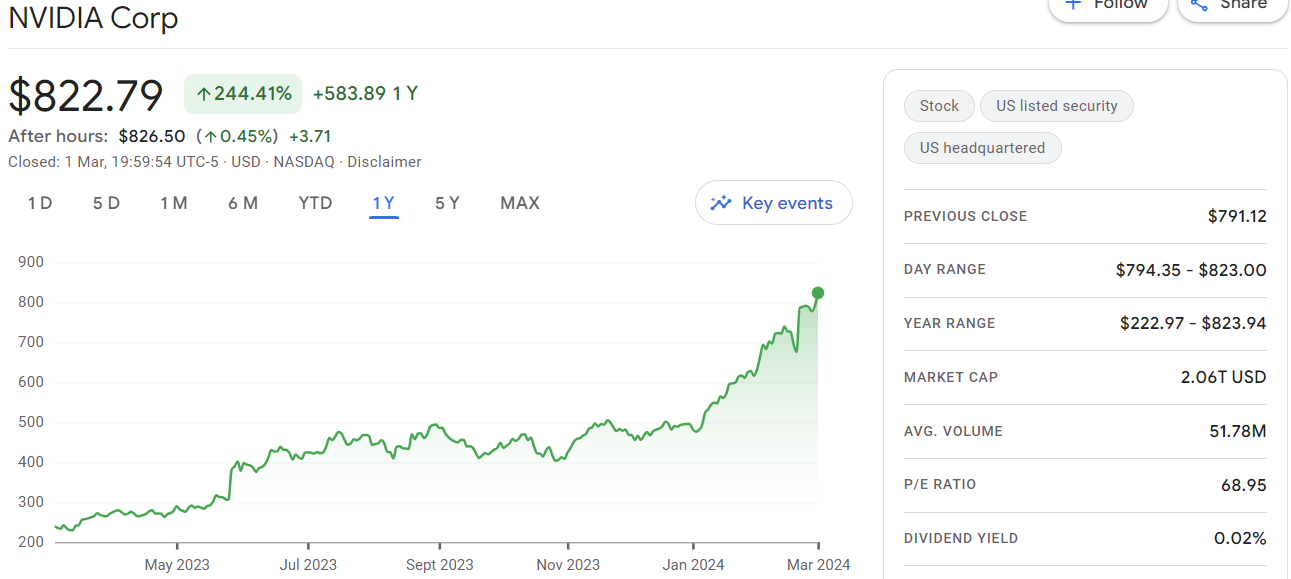

Nvidia envy

I’m also hit by my lack of a direct Nvidia position. Nvidia is talk of the S&P town at the moment – its stock rose from ~$600 to ~$800 in February alone! Nvidia is selling AI chips for $40k+ apiece, and is now worth over $2tn. This AI bubble-fuelled boom feels unsustainable to me. When the history of the next ‘correction’ happens you can be sure it will include “AI DIViNg” – Nvidia in reverse, I guess.

In other news

I have taken advantage of the continued surge in US equities to trim my target allocation a little. My target leverage has tightened from -20% to -18%. Right now I am between those two points.

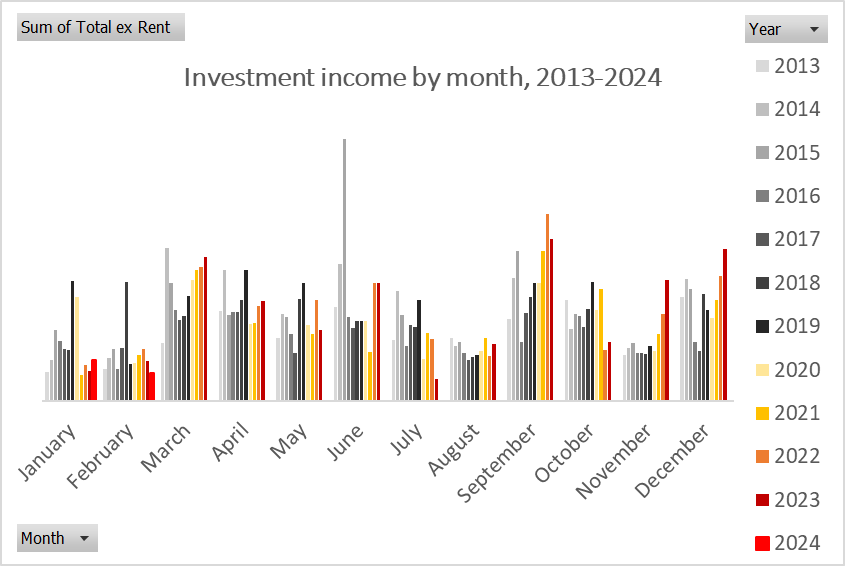

My February dividends were lower than they have been for years. February is always a very thin month for income, but unless my tracking has missed something I think I’ve had less income in February than I’ve ever recorded (since 2013 – see my ‘Weenie chart‘ below). March is usually a bumper month – the second or third highest of the year – and I remain reasonably hopeful for the 2024 edition.

Press clippings