A recent piece in the FT by Jason Butler mentioned some advice the author received from Peter Hargreaves, one of the UK’s richest men, a few years ago:

I asked Peter if he could share some of his money wisdom. He thought for a moment and then replied: “As you know I’ve got a few quid and I can pretty much have anything I want in life. I’ve got one car, one house and one wife, and that’s the way it’s staying. No matter how much you own or earn, keep your life as simple as possible.”

Now, (both) long time readers of this blog will know that I am not a fan of the firm Hargreaves Lansdown (though I have professional respect for it as a very effective way to part wealthy fools folks from their money). Nor, for various reasons I won’t cover here, am I generally an admirer of its founder Peter Hargreaves, notwithstanding that he is clearly a very talented entrepreneur/businessman.

However, this blog believes in playing the ball not the man.

I can recognise wisdom when I see it. And I think Mr Hargreaves’ advice to keep life as simple as possible is profoundly good advice.

How financial progress breeds complexity

For those of us who manage to grow our net worth, saving money, simplicity is an uphill battle.

That first thrill of making more money than you need to live will invariably result in some temptations. Time to ‘treat yourself’ with a new holiday? What about new clothes? Or some art? Or some furniture? Maybe even a new car? Carry on this way and pretty soon you’ll need more space, parking, garage, a yard, who knows.

But, once you’re making decent money regularly you will start wondering how/where to save it. Now, don’t misunderstand me, there are definitely simple ways to save/invest. But if you are tempted by property, EIS/angel investing, or extreme diversification, then care is certainly required. All of this increases your financial complexity pretty quickly. Carry on this way and pretty soon you’ll need an accountant to help with your tax return, and you will probably seriously consider talking to a financial adviser.

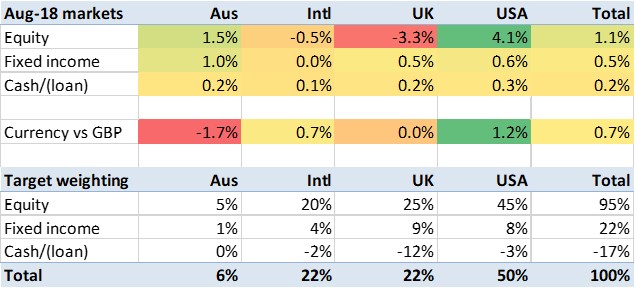

Once you start investing, time can be a surprising enemy. Most of us investors learn about ‘buy and hold’ as a strategy pretty early on. And twenty years in, I would say that ‘buy and hold’ works pretty well. But buying and holding can nonetheless result in an increasingly sprawling portfolio – as my recent ‘overdiversification‘ blog highlighted.

Property is particularly beguiling. As a reader of this blog, you probably don’t consider property to be the only way to invest. But is certainly one way to invest. You might, like me, consider that property has a place in a diversified portfolio, either via REITs or via ‘buy to let’. But have you considered / aspired to owning a weekend place? A holiday home? A ski chalet? Carry on that way and you’ll probably need a gardener, a handyman, maybe a builder. That’s one thing if it’s local but it’s another prospect if it’s in another country. Carry on further and you’ll be tempted by a second car, you’ll want access to the business lounge every trip or, worse, you’ll start seeing private jet ads follow you round the web.

Or perhaps, like me, you have become an ‘accidental landlord’. That ‘accident’ – your first place – is, in London, more likely to be leasehold than freehold, so maybe the maintenance/etc is not your responsibility. But if it’s leasehold you will have some form of service charge/sinking charge to budget for, and it’s freehold you’ll know all about every roof repair, damp patch, and boiler problem. Repairs and maintenance are all tax deductible, but make sure you keep those receipts. Carry on this way and even your accountant will start complaining.