I was lucky enough to go to Monaco for the F1 in June.

Something I feel quite strongly about and have written about before on this blog is how strong the monkey brain wiring is for us all to peg ourselves off the next rung up on the ladder. No matter how high up on the ladder we are ourselves, we instinctively compare ourselves to people who are ‘above’ us – i.e. “I’m not that rich, because I am not as rich as [X]”. I’ve argued before that we all know somebody doing 2x as well as us.

May was an enjoyable month. I kept reasonably busy, as well as doing a bit of travel around the UK. I visited King Charles’ Poundbury for the first time, as well as the south coast and the Cotswolds for a weekend.

Meanwhile, the news has been dominated by Trump’s Iran war, and in the UK Labour’s leadership dramas – now heightened with a forced by-election (“the most consequential in British history”) in Makerfield.

Markets in May

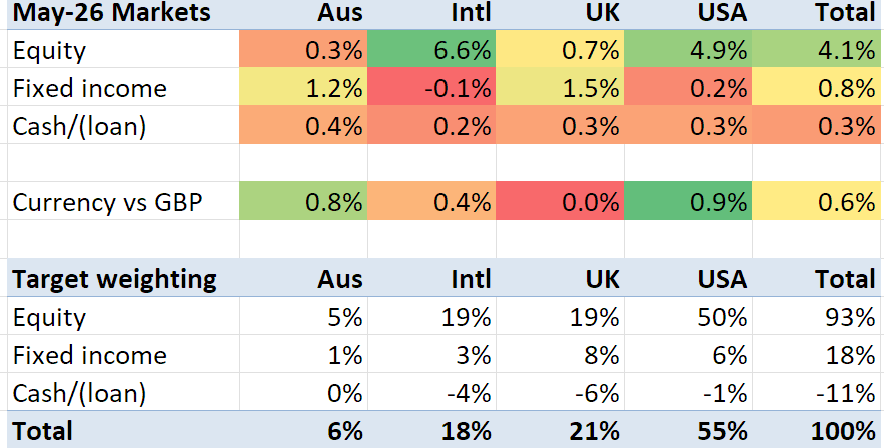

Tech stocks did well in May – both in the USA and in Asia (where silicon stocks are flying). My ‘international’ benchmark is half Asia/Pac and half Europe; Asia/Pac was up over 10%, while Europe rose ‘only’ 4%. Poor old tech-less UK and Australia equities rose only 0.7% and 0.4% respectively, though at least their bonds provided some consolation.

My portfolio buys a property

As I mentioned last month, I have been helping to complete on a property transaction – which went through in late May. I now co-own another property, sigh.

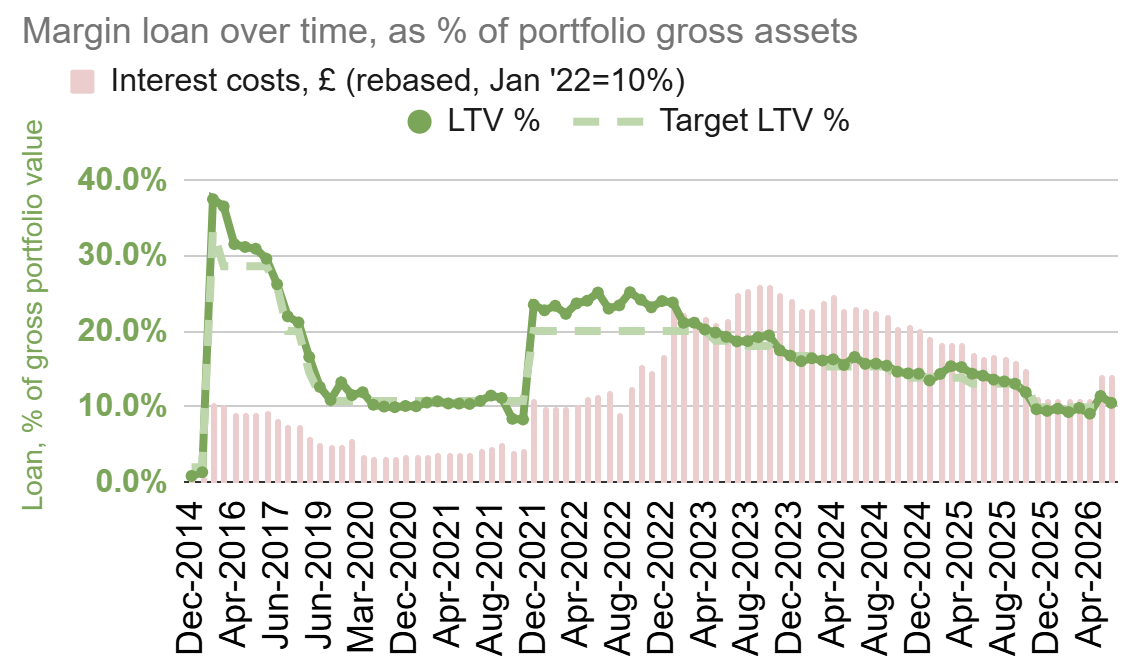

I had expected to borrow around £1m for this purchase, via my margin loan, but at the last minute I had a very welcome surprise: literally the Friday before the property transaction completed, an angel investment I made over 10 years ago was sold, netting me almost exactly £1m – entirely tax free (as it was made under the UK angel investing tax break EIS).

I have taken the opportunity to top up my ISAs to the £40k annual maximum and make a couple of significant charity donations too – something I try to do when I receive tax-free angel windfalls.

As a result my margin loan has expanded only slightly, and my total investment portfolio size has barely changed – and by among within the monthly volatility I experience. As a reminder – my investment portfolio excludes illiquid investments, so I do not count either properties nor angel investments within it – only investments in liquid, tradeable securities.

My interest costs (the pink columns in the chart below) are up due to the loan expansion, though my Loan-to-Value ratio (the solid green line) has not moved much (thanks to the >10% increase in the portfolio value over the last two months).

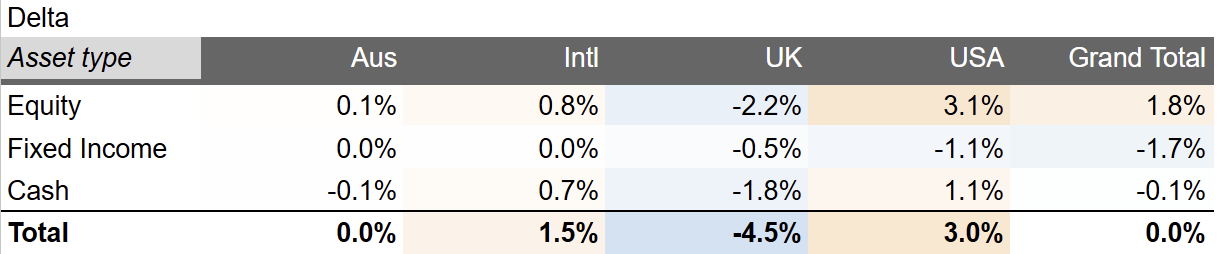

Having been long on cash before this property transaction, my portfolio has now returned almost to the target level of leverage. It is a little bit out of kilter on the geographic exposure though – with recent US gains making me overweight on US equities (and the US in general), and the takeover of a median UK holding for cash leaving me underweight on UK equities (and the UK/GBP too).

In the meantime my investment portfolio (that portion not being used to buy property) rose again in May. this time by 4.3%. Slightly less than the market-weighted benchmark which rose 5%, after an April in which my portfolio beat the market by over 1%.