This, my annual review for 2021, somehow was overlooked in January. But better late than never, let’s ensure 2021 is not forgotten – it was a rather extraordinary year.

2021 was the 9th year that I’ve been tracking my portfolio (reasonably) rigorously, every month.

Following the format I used last year, I’m setting out here to tackle seven generic questions that I think all prudent investors should ask themselves at least annually.

Q1 How did ‘my’ markets do?

The first question is ‘what happened out there?’.

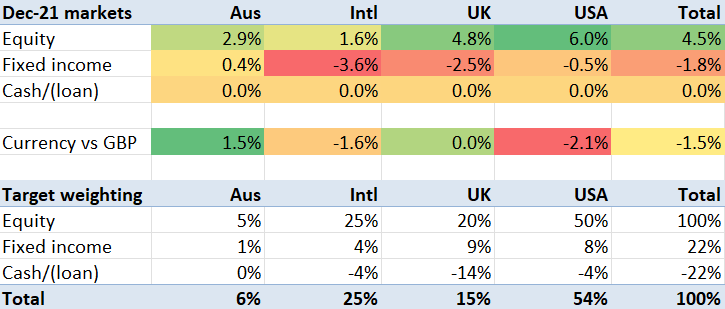

Firstly, how was December?

I won’t dwell on a single month in this post, but here are the figures, in the markets that I’m in:

And secondly, how was 2021?

This left the year as a whole looking as follows:

All the equity markets I track returned more than 1% a month, on average. And the USA posted more than 2% a month. Surely, the signs of overvaluation. Just as surely, we’ve said that before… In the meantime, how strong anybody’s portfolio was in 2021 was essentially a question of how much USA (and, in particular, tech stock) weighting they had in 2021. In my case, based on my year end target exposure of 50% USA equity, the markets provided a +15.2% contribution to my portfolio.

Bonds did not have a great year. They fell by 2-6%. Inflation worries, the hints of monetary tightening, the continued covid uncertainty draining government balance sheets, all played a part. In my case, with a 22% target exposure, mostly in the UK and USA, bond markets created a 1.1% headwind.

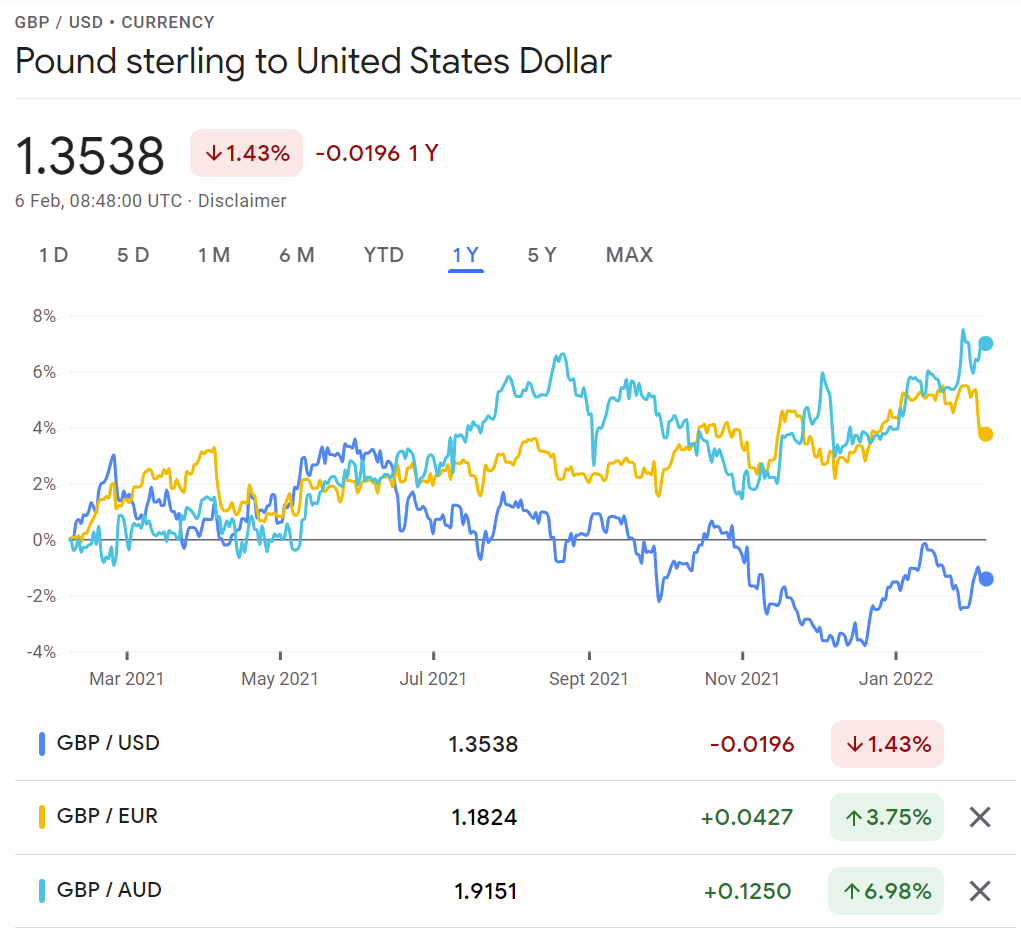

As to currencies, the GBP and the USD were pretty tightly coupled over the last 12 months, moving between £1:$1.32 and £1:£1.42. Meanwhile the GBP steadily rose against both EUR and AUD, ending up over 5% above where it started.

What these annual numbers don’t capture is how the tide appears, with almost a year’s hindsight, to have turned on “Spec(ulative) tech” as early as March 2021. This downturn started nibbling at the smaller, more speculative end of tech early in the year, and was then starting to ripple into bigger tech by the end of the year – but not by enough to materially dent the S&P annual numbers.

Q2 How did I perform vs ‘my’ markets?

The markets I was in, levered at the level I am targeting, went up as a blend by 20% in 2021. Against that, I underperformed – my portfolio returned ‘only’ 19% in the year. So much for any value I am adding through my judicious stock picking!

In terms of how closely I tracked my target exposure, this is a bit hard to say at the end of 2021. For starters, I changed my target towards the end of the year – upweighting the USA, and upweighting bonds slightly. For much of the year I had been a little bit underweight (and versus a lower target than now) against the USA, which accounts for how my portfolio didn’t quite obtain the full +20% that my final weighting would have suggested. As I finished the year my deltas versus my target are shown below:

As to particular ‘heros’ and ‘villains’ in my portfolio, my top gainers included 9 stocks that grew by 40% or more:

- Alumasc (+103%)

- Ashtead (+73%)

- Hubspot (+66%)

- Google (+65%)

- Microsoft (+51%)

- Macquarie (+47%)

- Dominos Pizza (+45%)

- AEWU (+45%)

- Diageo (+40%)

Whereas only three firms dropped by more than 20%, a Chinese one, a USA one and a UK one

- Alibaba (-49%) – which has suffered from a Chinese government choke hold

- Docusign (-31%) – which was firmly in the ‘spec tech’ decline

- LSE (-23%) – which has struggled with negative sentiment to the UK stock exchange generally, as well as indigestion over its Refinitiv acquisition.

Q3 How am I doing versus my retirement goals?

Regular readers will know I don’t really have straightforward retirement goals.

However given that I have just bought a Coastal Folly, there is clearly an argument (made particularly by Mrs FvL) that I have taken a giant concrete step towards retirement. Not one I planned or foresaw, as my blog roll is a testament to.

Q4 How tax efficient is my portfolio are my finances?

My portfolio has, surprisingly, ended the year with a slightly better tax exposure than ever before.

This is surprising to me, because I have had sufficient influxes/windfalls over the last 2 years to suggest the unsheltered bit of my portfolio has outgrown the tax sheltered bits. I say this, knowing that I haven’t topped up my Ltd company in line with the windfalls. However, what has happened is the tax sheltered bits (the ISAs and SIPPs in particular) have grown nicely. And in December I dipped into the unsheltered reserves significantly in December to buy the folly. So the overall balance leaves me with a weighted tax rate of 29%.

I am changing the question slightly this year, to widen from ‘the portfolio’ to ‘my finances’. This includes my ‘earnt’ income, which has been material over 2021. My working earnings are fully taxed – at the additional tax rate of 45%. And to make matters worse, I / my employer are making pension contributions. Pensions are *not* tax efficient for me – because I am a sufficiently high earner for my annual tax-free contribution to be tapered down to only £4000.

To make matters worse, I expect my personal pension (SIPP) to breach the total lifetime allowance (of about £1.1m) fairly soon, leaving me with >50% tax charges on the excess. I have half-heartedly sought advice on what to do about this, but haven’t found a clear solution. In the meantime I assume that the tax penalties are roughly compensated by my employer’s 1:1 matching contribution, and the markets could still yet fall by 20-30% leaving me well clear of the lifetime allowance at the point I am actually tested on this stuff, so I am ploughing on regardless. If readers have smarter strategies to share I am all ears.

Q5 What does my portfolio cost, in cash terms?

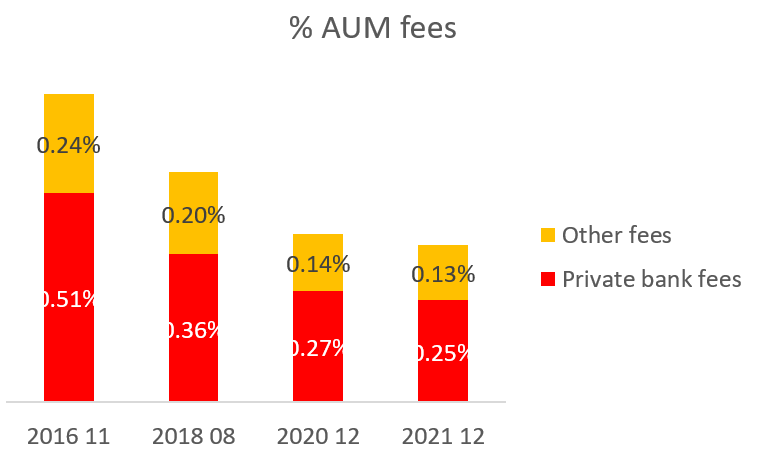

The next question is the fee burden borne by my portfolio. 2021 saw steady progress on this front, with my total burden dropping a few bps. The bulk of the burden remains the private bank fees I pay, but even including these the total fees are now comfortably below 0.40% of my portfolio – so I really am now in the land of diminishing returns.

Q6 What does my portfolio cost, in time terms?

Since early 2020 I have been trying to fight the complexity of my portfolio.

I made slow steady progress in 2021, finishing the year with 120 unique holdings.

Only 5 holdings were smaller than my target minimum. These include:

- a legacy Schroders/Woodford fund that I am loath either to sell (crystallising losses) or to top up,

- a tiny holding in a recent IPO I hold mainly for comedy value, and

- a nasty private debt fund sold to me by my private bank some years ago that, thankfully, has mostly returned the capital but is impossible to either top up or liquidate.

What matters most in the complexity stakes is the number of (not necessarily unique) holdings that are unwrapped – these are the ones I need to report on to the tax authorities. That number has dropped to 71 unique holdings – about 110 including duplicate holdings held in multiple accounts. Still plenty of paperwork, but a level that is both fairly manageable and hard to reduce dramatically further.

Q7 What key risks am I taking?

The last question on my list is about risks.

With my new coastal folly fresh in my experience, a hefty increase in leverage and now, as I finish this post, a dramatic stockmarket drop going on particularly in tech stocks, I face materially more risk than I have for a while. The leverage I finished the year with – before the 8% market drop in January – is shown below.

I have three accounts with leverage, and the negative cash position in each of them is between 30-40% of the total value of the assets in the portfolio. If this percentage gets close to 50% I face the risk of involuntary selling – ‘margin calls’. I have plenty of other assets I could draw on, but largely in tax sheltered accounts which I am very very very reluctant to access. So really I need to find ways to reduce my debt. Based on my experience in 2016-2018 this will take well over 12 months.

I still have the Living Will on my to do list. Not good that I haven’t had the discipline to follow up on this. Must do better.

Conclusion

At the time of writing it appears that 2021 may well prove to be the high watermark of a US tech stock-led boom. In any case, a gain of 20% in the markets makes me a lot more money than I can easily earn in a year.

But whatever happens next with the markets, I will remember 2021 as the year I opened up a new avenue in my life by buying my Coastal Folly. I look back on 2016 as the year I kicked off my Dream Home, which has been a permanent upgrade to my life that I haven’t looked back on. Hopefully 2021 will similarly represent another year my life got better. And just as I can’t really remember what the markets did around 2015/2016 (pace the occasional referendum), at the end of the day I probably won’t remember the market movements of 2021.

Whatever the movements in my personal life, property portfolio and the markets, the basic ‘health stats’ of my portfolio have all improved slightly in 2021 – with one exception, risk. The key risk I face is that I look back on 2021 as the year I overextended myself, and made a giant mistake by buying a Folly. This is a risk I can manage. And how I manage that risk will continue to be something I document on a roughly monthly basis on this blog. As ever, all comments, suggestions or observations are very welcome.

I am aware of one such strategy to optimise the LTA which ZX presented on Monevator.

https://monevator.com/the-annual-allowance-for-pensions/#comment-1178761

Essentially you make two matching trades, one in the pension where you bet the market goes down and one in the ISA where you bet it goes up. You’re net zero over the market, and if the market raises you transfer money from one to the other, net of fees.

But, and I think this is the biggest problem, while you can hold options in your pension, you cannot easily do it in your ISA. If you get the hang of ZX and ask him how he did it, that might be useful for some of us.

LikeLiked by 1 person

“while you can hold options in your pension, you cannot easily do it in your ISA.” Could you find an investment trust that’s heavily into options? Or, if your ISA holdings are all equities and equity funds, and if they and your untaxsheltered investments outweigh the pension investments, you could reckon that you are anyway betting on the market rising.

Or instead: is someone who holds lots of Ruffer Investment Company in his pension and lots of Scottish Mortgage outside it already implementing a strategy that is a rough-and-ready approximation to the ZX ploy?

LikeLike

I read somewhere ETN’s or synthetic ETN’s could be used to achieve the same result – it’s beyond my knowledge so if someone can give a fuller explanation of how this would work in practise pls

LikeLike

Avoid LTA by taking advantage of any major downturn to crystallise the lot by taking the 25% tax free lump sum. The 75% remaining can then grow when markets recover and can exceed the LTA up until age 75, but you can simply withdraw any excess before, without penalty. By taking only the 25% tax free and no taxable withdrawals, you can still make contributions up to £40k p.a. which then forms an uncrystallised part of the pension, which can also grow up to the LTA.

LikeLiked by 1 person

Enjoyed reading the post. Thanks fir sharing.

LikeLike

[…] financially. I’m following the same structure I’ve used for the last few years (2022, 2021, and 2020). Overall, 2023 was a good year on almost all measures – thanks in particular to […]

LikeLike