It’s been a beautiful month. I’ve been about a bit, taking in Lincoln, the New Forest, and Oxford as well as enjoying London town itself.

The Iran conflict rumbles on, with the USA and Israel having effectively finished the military engagement.

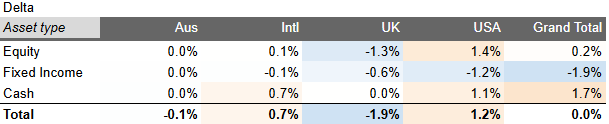

Markets have had a very strong month – bouncing back from the March drop completely. The pound rose (though the AUD rose more). The standout story though was Asian equities, which rose around 14% in the month, with the AI boom lifting Asian semiconductor players and a sense of relief about the Straight of Hormuz (which most clobbers Asian energyt supply chains). US equities also did well, though this was largely due to the drop they suffered in March.

The ‘SaaS-pocalypse’ continues but big tech has shown resilience. Google, my biggest holding, is up at record highs – how I look dumb for selling out at $265 only a few months ago.

My portfolio rose 8.7%, which was the strongest single month since I began monthly tracking over 13 years ago.

Spending capital

I’ve spent a lot of money in the last few weeks. I’ve replaced/upgraded the heating systems at both the Coastal Folly and the Dream Home. I’ve spent money on my boat. I’ve also replaced my car. And I’ve paid for an expensive flight to Australia.

A year or two ago I’d have been trying to make these purchases out of income, not capital. These days I’ve given up. Partly because markets have been so rampant. Also because these sums are fairly clearly capital investments, not current spending. And partly because I have a much bigger purchase coming at me – so there is a sense of ‘in for a penny, in for a pound’.

Time to buy a house

Over in my portfolio I am in the process of supporting a family member buying a property. So far all I’ve done is pay the 10% deposit on the house, which I’ve done by liquidating assets (and incurring a capital gains liability, in about 2 year’s time due to it being right at the start of the UK tax year).

I had considered liquidating more assets / repositioning my portfolio in anticipation of a significant loan drawdown. It felt like just my luck that markets dropped 6% just as I was committing to support the property purchase. But having done nothing material to my portfolio, I am lucky that the markets have in fact resoundingly recovered.

The remaining funds for the house purchase – over £1m – I will do via a portfolio loan. This will save me crystallising capital gains. I am expecting a £100k+ payout on the takeover of a public equity I hold, that will go against paying down the loan when I receive it. I am also expecting (touch wood, but not relying on) a ~£1m payout from the sale of a private business I was an angel investor in 10+ years ago (with £20k invested), which should be a) tax free and b) almost exactly the amount I need to pay off the remaining loan. So the flexibility of the margin loan – from the private bank this time – is much appreciated.

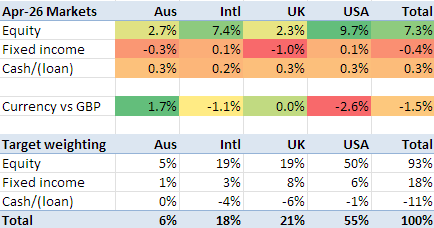

As at the start of May here is my delta from my target allocation. I am long on cash/short on my portfolio loan, in anticipation of a big drawdown against that facility to complete on the house later in May. I’m also short on fixed income, which I don’t immediately understand – though I think it’s a hangover from some of my portfolio simplification in February.

Once I draw down on my portfolio loan, and take the money out of my portfolio, I am going to be very underweight on cash and overweight on equity. I will have to decide whether to adjust my target allocation or accept that it will be at least a couple of months before I pay back the loan and restore equilibrium. I’ll see how I feel at the end of May.

Beautiful photos thank you – sunny days in UK are to be treasured. You will be coming out here to Oz when we are hitting bad weather, or was it for end of year ? Lots of changes coming in the AU budget shortly but unless you have Australian trusts or property probably won’t be too relevant.

LikeLike

thank you!

my next trip is end-of-year in fact. And as you say I don’t have any tax exposure to the place, yet.

LikeLike

Is anyone actually gaining anything by reading this blog? Genuinely asking. I thought this was a blog about FIRE in London, not about the extravagant lifestyle of one rich person…

LikeLike

Another great update, thank you.

LikeLike

That’s a sensational monthly return! Let’s hope it sticks.

All I can say regarding the house purchase is ‘lucky family member’.

20k to 1m in a decade is a cagr of almost 50%. Chapeau!

LikeLike

[…] I mentioned last month, I have been helping to complete on a property transaction – which went through in […]

LikeLike