I returned to London from my Easter break to the surprise announcement that Theresa May has called a general election on June 8th. Normally I love elections and am a news junkie about them. Personally I think the PM has missed an opportunity to lance the Scottish nationalist boil by calling a simultaneous #indyref2. So instead of that excitement, I find myself agreeing with piece in The Sunday Times today arguing that for once a foreign election, in France, is more exciting than the anticipated Tory landslide in the UK’s general election in June.

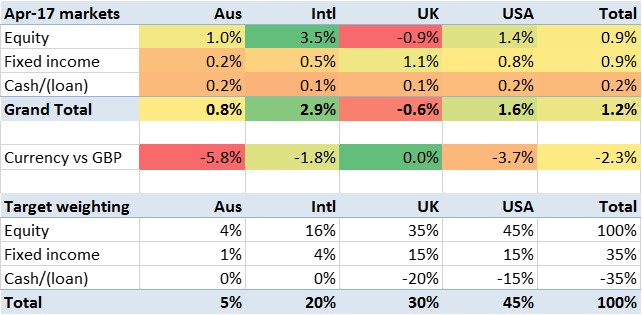

Certainly Macron’s win in the first round of the French election lifted European stocks considerably. The European index I use as my proxy for ‘international (i.e. non UK/US/Oz) equities’ rose 3.5% in April, well ahead of the English-speaking stock markets. While we can’t ignore the prospect of a Le Pen win, it doesn’t appear likely from opinion polls. Much as people are knocking pollsters right now the only result they got wildly wrong in the last few years was the 2015 UK General Election result (where First Past the Post makes predictions particularly tricky). So most likely European markets are going to get better rather than worse.

The other big news in the markets for Brits was the jump in the pound, attributed to the prospect of ‘stronger and stabler’ UK leadership post the general election. Forex markets clearly haven’t clocked that the European leaders who do best in EU negotiations are those with credible domestic oppositions to appease, not those with autocratic majorities. In any case, the pound is still below $1.30 so the Brexit Brainfart hasn’t blown away yet. But the pound rose against the whole basket, particularly the AUD (+5.8%). This led to FTSE, a foreign-dominated stock market, dropping about 1%.