I returned to London from my Easter break to the surprise announcement that Theresa May has called a general election on June 8th. Normally I love elections and am a news junkie about them. Personally I think the PM has missed an opportunity to lance the Scottish nationalist boil by calling a simultaneous #indyref2. So instead of that excitement, I find myself agreeing with piece in The Sunday Times today arguing that for once a foreign election, in France, is more exciting than the anticipated Tory landslide in the UK’s general election in June.

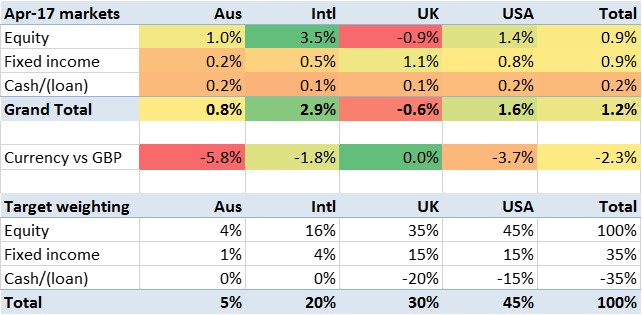

Certainly Macron’s win in the first round of the French election lifted European stocks considerably. The European index I use as my proxy for ‘international (i.e. non UK/US/Oz) equities’ rose 3.5% in April, well ahead of the English-speaking stock markets. While we can’t ignore the prospect of a Le Pen win, it doesn’t appear likely from opinion polls. Much as people are knocking pollsters right now the only result they got wildly wrong in the last few years was the 2015 UK General Election result (where First Past the Post makes predictions particularly tricky). So most likely European markets are going to get better rather than worse.

The other big news in the markets for Brits was the jump in the pound, attributed to the prospect of ‘stronger and stabler’ UK leadership post the general election. Forex markets clearly haven’t clocked that the European leaders who do best in EU negotiations are those with credible domestic oppositions to appease, not those with autocratic majorities. In any case, the pound is still below $1.30 so the Brexit Brainfart hasn’t blown away yet. But the pound rose against the whole basket, particularly the AUD (+5.8%). This led to FTSE, a foreign-dominated stock market, dropping about 1%.

The rest of the market saw modest gains. Bonds up almost 1%, US/Oz equities up just over 1%.

When you net off the market constant-currency gain of 1.2% against the 2.3% drop of $AUD/€EUR/$USD, the weighted market I’m exposed to dropped just over 1%.

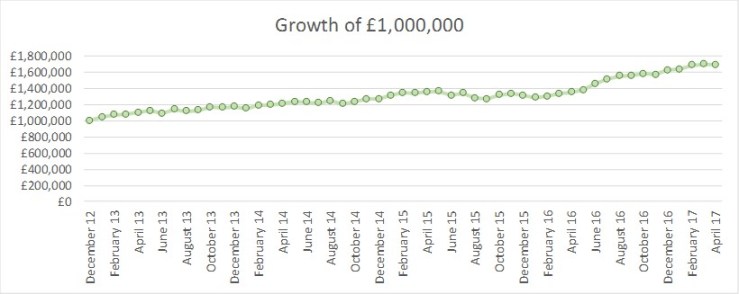

How did I actually do? My investment portfolio lost about 0.4%. My portfolio outperformed my (forex-adjusted) market by about half a percent.

April was a more significant month for my portfolio than the unitised return would suggest. I moved £40k into my+Mrs FvL’s ISA accounts. I had a couple of significant costs for which I raided the portfolio. Overall my portfolio (which excludes Mrs FvL’s) has shrunk more than it appears in the graph.

On top of this, and very pleasingly, I have managed to repay over £100k of my portfolio loan. I have done this partly by using proceeds from top slicing my biggest holding, partly by banking an unexpected capital redemption from an illiquid high-fee investment the private bankers sold me, and partly thanks to the sale of another illiquid investment. This has pulled my Loan To Value down below 27.5%. Changes in my loan leverage don’t affect the net value of the portfolio or the immediate investment returns, but I’m breathing slightly more easily as this number drops.

Correction: I’ve just corrected my April returns because my tracking hadn’t kept pace with the funds into my ISA. Actual returns for the month were -0.1% not -0.5%; this means they outperformed the market by almost a percentage point. No complaints.

LikeLike

Hi FvL,

Congratulations on a good month all round,and in keeping working down on the leverage! The more you can keep filling up your ISA at the start of each tax year then I don’t blame you – slam the tax advantages as much as possible whenever you can!

Cheers,

FiL

LikeLike

Looking at April one month later, the market returns figures seem to have changed since I wrote this update. I am not quite sure why this is but put it down to some of the sites (iShares in particular) having updated their figures retrospectively. The weighted average for the month was more like 0.90%, not 1.2%. Not much of a difference, but I’m noting it for my records.

LikeLike