Picture the scene. You’re an entrepreneur / widow / recent inheritor / recent divorcee or similar. You don’t work in financial services. You find yourself receiving a lump sum of cash – more than you have any immediate plans for – and, as surely as a carcass on the African plains attracts vultures, you end up talking to a private banker or an independent financial adviser.

If this scene is familiar to you, then I think this blog post is the most important blog post you will find on my blog.

The charming, well-dressed and thoroughly presentable financial professional makes arguments along the following lines:

- I am a very experienced financial professional. You can tell from the quality of the tea and biscuits, my dress code, and perhaps my accent – suggesting that at least my parents and grandparents had a lot of money.

- You are a talented and clever person. Either because you created value some of which you have just ‘cashed out’, or because you married a very talented/rich person who sadly(/happily?) is no longer with us and/or you.

- You realise that leaving your money in cash gets it nowhere, before tax.

- You understand that all the rich people do not just leave their wealth in cash but instead have their money ‘invested’. I invite you to believe that this has helped them to protect, maintain and increase their wealth.

- There are a lot of clever things you can do about tax. [For the purposes of this blog post I am not going to expand on this further].

- You do not have the time and/or expertise to manage your money yourself. Picking stocks is gambling, complicated and your money can be at risk.

- I and my firm manage money for a living (therein lies a clue which I don’t want you to dwell on, and heaven forbid don’t ask what I do with my own money).

- In fact at my firm we can do various particular things for you:

- We have many clever analysts. I can introduce you to some and ensure you have ready access to them whenever you want it.

- We have economies of scale which allows us to negotiate better rates than you or our lesser rivals can get.

- We can invest in overseas investments.

- We have access to special investments that aren’t generally available. These include investment products made by some of the most famous and successful financial services firms of all time, who do not deal with mere mortals such as you.

- We, or some of our most trusted friends, can structure special products which

turn base metals into goldeliminate all risk and practically guarantee fantastic returns. - We can look after whatever tax filings you need in whatever jurisdictions / etc your tax planning / divorce court / similar lands you in.

- We will review your finances carefully against your objectives and give you professional, bespoke advice – a complete financial strategy, along with all the help you need to execute it.

- Fees? Well, since you ask, yes there are some fees but they are very modest. Essentially only just 1% of all that money we manage for you, along perhaps with occasional incidental expenses.

I invite comments about how well I have captured the thrust of a typical IFA/wealth manager’s pitch. I have quite a bit of experience of being on the receiving end here and think I have captured the key pitch; indeed, I would even say that it does sound quite compelling.

I myself took the bait about 15 years ago. I have had a pot of money managed by a private bank since around 2000. I did so as part of a ‘test and learn’ strategy in which I put various pots of money to work in various places – some went to private banks, some I managed myself, some went into structures I found with an IFA. I tracked all of it quite carefully with some professional investment-tracking software (alas that is no longer on the market). Since 2013 I have been more rigorous and have done full month-end tracking which I post on this blog, but I have most of my portfolio tracked pretty accurately (albeit updated sporadically, not monthly) since around 2000.

What I gradually learnt from 2000 to 2010 was that the money I managed myself did better than the money I invested with the professionals. I didn’t really think about why this was – other than my ineffable genius – but it was pretty clear that fees were a part of it. Gradually I moved more and more of my money into pots that I manage myself, leaving the pot managed by the private bank as a smaller and smaller proportion of my net worth.

In the last few years I have become increasingly maniacal about fees. Yet even as I did so I continued to pay my private bank 1% to manage a large balanced investment portfolio. I reasoned that this was the ‘entry ticket’ into that relationship; the private bankers gave me decent service (at a transactional level) and that the 1% fee, when viewed across my entire portfolio (most of which has <0.1% fees), wasn’t an unreasonable fee to pay. My blended expense ratio was well under 1%, or so I thought.

In any case, with the recent FT article about fund managers making 2.5% per year on typical portfolios, I wondered ‘who are the idiots who are paying 2.5% per year?’. And this got me looking more carefully at my own situation. And lo and behold, my ‘1%’ figure turns out to drastically underestimate the fees I’m paying. I discovered I myself am one of the idiots.

The true figure I am paying my private bank, for a ‘discretionary portfolio’ they manage for me, is a gob-smacking 2.04%. This probably excludes a few trading fees within some of the funds that I can’t cleanly see. How do I get from ‘1% of money managed’ to ‘2.04%’? Only by being an idiot.

Here is what is happening:

- The price has gone up. I didn’t realise but at some point in the last few years my annual service fee has increased to somewhere around 1.2%. I don’t get clear invoices for this so I haven’t quite got to the bottom of it.

- VAT. The 1% – sorry, 1.2% – is a service fee. And services attract VAT. 20% in fact. So the supposed 1%, which I now realise is 1.2%, is actually 1.44% straight out.

- The portfolio contains fee-paying funds and ETFs. The structure of the portfolio is shown below. As you can see, funds account for over 50% of the value of the portfolio and the total expenses of these funds amounts to 30% of my expenses – which is over 0.6% of my assets. ETFs, which are about 12% of the portfolio, also have fees but they are much lower – amounting to 2.4% of my expenses and thus only 0.05% of my assets.

| Contents of discretionary portfolio | % of portfolio | % of fees |

| Fund | 53.87% | 29.90% |

| Equity – share | 22.37% | 0.00% |

| Equity – ETF | 12.03% | 2.36% |

| Bond – ETF | 6.97% | 0.68% |

| Cash | 4.75% | 67.05% |

| Grand Total | 100.00% | 100.00% |

The seven largest funds account for 30% of my portfolio and have average fees – on top of the portfolio management fee – of 1.1%. Take a look at the list below: would you pay 1.44% to be placed into these funds?

| Security | Total Expense Rate % | % of portfolio |

| Blackrock European Dynamic Fund | 0.92% | 6.6% |

| Polar Capital Funds Plc – Global Technology Class | 1.15% | 5.4% |

| Findlay Park Funds Plc – American Fund | 1.04% | 5.3% |

| Standard Life Investments – UK Smaller Companies Fund | 0.99% | 4.0% |

| J O Hambro Capital Mgmt Umbrella Fund- UK Equity Income Fund | 0.69% | 3.4% |

| GS Quanto Autocallable Note on SPX, Sx5e, UKX, 22 Apr 21 Sn025-16 | est. 2.00% | 3.0% |

| Barclays Globalaccess – US Small & Mid Cap Equity Fund | 1.00% | 3.0% |

So, having established I’m overpaying savagely for a fund-of-funds, how is the performance of this portfolio doing?

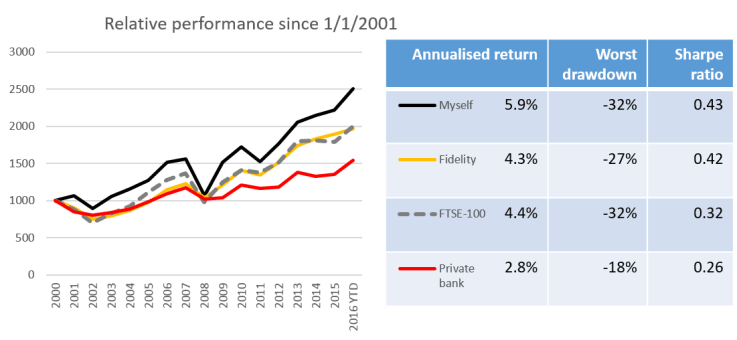

I’ve pulled out the performance of my private banking discretionary portfolio over the last 15 years. I’ve done the same with a small portfolio that I’ve had with Fidelity throughout that period (for which, these days, I pay a platform fee of about 0.3% plus the TERs of the actual funds; my blended cost is about 1.6%). And the same for a portfolio I’ve managed myself, on a low-cost internet broker, since 2000; this portfolio is mostly UK equities but with a few UK funds in there too (this portfolio has no annual fees; my blended costs are less than 0.3%). For all three portfolios I am looking at the year-end net portfolio value, after fees. The results are shown in the figure below.

What you see is that my own portfolio has been averaging about 2.5x the annual net performance of the private banking portfolio. The Fidelity portfolio is pretty neatly in the middle, and very closely (did I say closet-ly?) tracks the FTSE-100’s performance. The private banking portfolio has delivered only two thirds of the FTSE-100. These figures ignore taxes and inflation; after tax, my private banking portfolio has not kept pace with inflation.

The private bank’s 2.04% fee is clearly a major part of this underperformance, but not all of it. It is important when comparing two or more portfolio track records to adjust for relative risk. A portfolio comprised purely of tech stocks might outperform a steady bond portfolio, but it is also far more volatile. An easy way of normalising for this is to look at the Sharpe ratio, which is the ratio between the return and the volatility. On this basis, the portfolio I’ve managed and the portfolio Fidelity has managed are almost identical; but the private banking portfolio is a third worse.

Overall, fact Fidelity has a reasonably good argument for its fees in my view. It hasn’t underperformed the market, but it has delivered similar performance after fees with noticeably less volatility. I recommend Fidelity to family and friends as a sensible place to invest in the stock market if you can’t face doing it yourself. However its Sharpe ratio isn’t better than my own, and the performance gap versus my own funds is almost exactly the blended fee of 1.6% p.a.

The private banking portfolio, on the other hand, is a clear rip-off. In its defence, it clearly is a lower risk portfolio than the others. I was particularly appreciative of this in 2008 when it dropped by ‘only’ 12%, compared to the 32% wound I was nursing in my own portfolio. But actually the performance back in 2000-2002 was worse, with an 18% fall top to bottom. And when you look at the graph those bigger dips on the less expensive portfolios only brought me down to the level the private bank had struggled to reach in the first place. I can’t recommend private banking portfolios to anybody.

In case you’re wondering whether my particular private banking portfolio is a lemon, I don’t think it is. I’ve had three such portfolios over the years. The surviving one has survived because it is the least bad. Investments I made through my IFA have done worse but are so illiquid I can’t even get out of them properly. And I’ve been pitched others’ solutions too and don’t believe anybody has a structural advantage over my private bank. I’m not naming my bank because I think their rivals are worse, and it wouldn’t be fair to my lot to imply they are uniquely dreadful. London Rob’s IFA seems better but is still underperforming London Rob himself.

The lessons here are clear: avoid paying 1%+ of your assets to a middleman. Especially if that middleman then invests in a bunch of managed funds, which just adds fees upon fees. This means you should:

- Ideally, manage your money yourself. See Monevator’s excellent blog for guidance.

- If you can’t/won’t do that, then open a diversified investment portfolio with Fidelity (or Hargreaves Lansdowne, or similar) and pick a handful of their lowest-cost equity-orientated funds. Or go for a Vanguard Lifestrategy fund (which is not quite as easy as it sounds to set up, I think).

- Use IFAs for specific tasks such as setting up a portfolio, tax structuring, dealing with a health situation. But in all cases avoid paying any ongoing fees. What you really want from an IFA is a single page recommendation of how to structure your funds, and what to allocate to whom. Do not let the IFA then implement it for you – go and do it yourself. By all means pay the IFA for the consultation but let that be it.

- Use private banks, if you must, only for transactional accounts and not for any investment portfolios.

And I myself need to stop paying my private bank a ridiculous sum for such terrible performance. I don’t want to close down the relationship entirely so I need to tread carefully. Any tips/suggestions for how to do this would be much appreciated.

Very illuminating post, thank you. I, like you, work(ed) in IB, and closely with WM, and understand the business model. Consequently, to the extent that I use the WM offering of my former employer at all, it’s for liquidity products and equity brokerage/custody with 50% discounted staff pricing.

There are no circumstances under which I would pay anyone a %age of AUM to manage my assets, least of all a private bank. I’m training my wife, and look forward to soon training my children, in portfolio management so they don’t get ripped off when I’m dead.

If and when I lose access to the discounted pricing, I will switch to a number of low cost brokers to spread my counterparty risk but, like you, I value the optionality in the relationship. In the meantime, I attempt to add value to them in other ways – leads, investment opportunities e.t.c.

LikeLike

Thanks for your comments – that’s really useful feedback. In fact I never have worked in financial services but I do follow it quite closely. One thing I would love your best guess on: how low could I push my discretionary portfolio – i.e. what level of management fees would be enough to sustain the WM relationship (for its optionality etc)? £10k p.a.? There are additional custody/etc fees but they aren’t much – probably about £2k p.a. – so I think the management piece is the high margin bit for them.

LikeLike

It depends on the bank and how they’re doing currently, and on your RM and how senior/hungry he/she is. They seem to have a great deal of flex where they see and can justify to their management upside over the medium/long term. So the proportion of your assets held away are key in your case, as well as your network and who you can bring to them e.t.c.. If you are low maintenance and/or you dangle sufficient carrots you should be able to get away with less than 10k

LikeLiked by 1 person

A bit late to this, but a useful resource/reference in terms of ‘Private Banking’. The 2016 FT Private Client Wealth Management report lists quite a lot of the providers.

Click to access 7f6fe70e-7897-11e6-a0c6-39e2633162d5.pdf

The really useful information is the amount of assets held on an execution only basis on page 10. My experience is execution only services are always well hidden and never pro-actively offered, but this does show even some of the big players (e.g. UBS) have much more execution only business than I thought they would.

LikeLiked by 1 person

Great post FvL. Really great to see a real life example of self managed vs managed by the professionals. I fortunately never did quite make it to a Money Manager or Financial Adviser extracting large fees from me. I did however hear their sales pitches though and in hindsight was very fortunate that I did some simple maths afterwards (plus stumbled across the book Where Are The Customers Yachts) which helped push me to my DIY approach in 2007.

Early on my DIY road I think I can possibly top trumps your good self though as I did end up with an Actively Managed Leverage Share Fund with annual expenses of 3.22%! I’m glad I learnt fairly quickly as that sort of approach could have been very damaging to my long term wealth. Today my total wealth is carrying expenses of 0.24%. I’d like it to be less and will continue to look for opportunities but at the same time I’m sort of ok with that level of expense as it will not hinder me taking FIRE in the very near future.

Interesting to see your own CAGR since 2000 at 5.9%. Do you have it since start of 2008? The rocket boosters my portfolio has been attached to this year (up 14.0% YTD) sees my annualised performance since the start of 2008 at 6.9%.

LikeLike

Thanks RIT. Thank you too for your related ‘can anybody afford NOT to DIY’ post. Since beginning of 2008, you meanie, the CAGR on this ‘myself’ portfolio is 5.42%. From beginning of 2009, it is 11.4%!

LikeLike

Thanks for sharing your performance numbers. If I jump forward a year I’m at 9.9% so you have me there.

Why I’m always so interested in your, people like diy investor (UK) and other UK bloggers who share performance is how our performances can vary quite widely month-on-month, quarter-on-quarter and even year-on-year but then as the time lengthens we all start to converge toward similar numbers.

It nicely demonstrates for me the argument for passive low cost investing because while ‘some’ experts can generate out performance over short/medium terms I’ve always questioned if anybody will actually do it over the long term … and when I think long term I’m thinking 30-40 years.

LikeLiked by 1 person

Hi

My first post here, but I have seen your site for quite some time. I started out using an IFA, but quickly realised that I could do the research myself & not need to pay the costs (commission) incurred by them especially when I’d discovered HL in their early days before IPO. From then on, & I am counting 20 years plus, I have managed my own affairs utilising over time HL, Co-Funds & Fidelity platforms, plus my company pension schemes platforms/provision.

Therefore I never went near a Wealth Manager, although I get approached by all sorts to try and take over my portfolio.

I currently hold all my investments, plus my wife’s & my mothers on HL, at the rate for the size of the portfolio as if it was held by 1 person, of .25%, which takes into account that I hold approximately 50% in shares, so taking into account the funds that invest in my fees are less than 1%.

As to my CAGR, over the 20+ year period I am tracking 8-8.5% pa, with a 1 year of just over 10% & I have been in drawdown phase for the last 3 years.

So my advice to anyone who seriously wants to accumulate wealth is to learn to DIY, but I was fortunate that my job involved managing money purchase pension schemes & I took the time & effort to learn from all the professionals I needed to use.

Gareth

LikeLiked by 1 person

Gareth – thanks so much for sharing. Heartening to hear.

If I understand HL’s tiering properly you are paying 0.45% on the first £250k. So your blended fee rate is at least 0.3% plus funds’ fees – is this right?

Out of interest why do you stick with HL? I only cottoned on to them post IPO but I have always seen them as a Fidelity alternative i.e. good for non-DIY-ers. I know I can hardly talk as I haven’t ditched my 2% outfit but couldn’t you get quite a lot better with e.g. Selftrade?

LikeLike

Hi

Nope, the rate that I negotiated was 0.25% across the whole portfolio.

Why do I stick with them because I got this rate and, when I take into account the loyalty kickbacks I get, plus the management fees on the funds that I hold, the costs are below 1% and I’m beating the market.

Also the hassle to transfer out would be horrendous and the customer service is great, probably as I fit into their profile of a significant customer, hence the deal I got when i threatened to leave when they introduced their new rates.

Finally, as you have may have noticed, the other platforms keep increasing their rates i.e. AJ Bell and I’m sure the others will do also, so I will stick with the premier platform where I already get a great deal.

LikeLiked by 1 person

Interesting. Fidelity are being daft at the moment; I have reduced my holdings with them to under their £250k cutoff, but my wife’s holdings are over that threshold. They say that I/we won’t qualify for the tiering discount because my wife’s holdings are ‘secondary’ and primary holdings are what matters. I like Fidelity for the wife’s accounts just in case the proverbial bus comes along. Do you have a contact at HL I could talk to about switching our Fidelity funds into HL 😉 ?

LikeLike

I wrote direct to the Chief Executive Ian Gorham. I had already picked up a thread on a weblog that HL were likely to do a deal on accounts held by a family, especially if the amount being held was over £1 million, which mine was (there are 3 people, myself, my wife and my mother and all their accounts (7 across the 3 people) are linked to mine as I do all the investing etc.)

The key thing was probably the timing as it was when HL introduced their new charges as a result of the RDR and there was quite a bit of kerfuffle at the time due to the amount of the charges and the way they were going effect certain customers.

I did say that if a deal was not reached that there was certainly going to be a platform that would do a deal with me given the size of the holdings that the family held, although I never actually followed up on seeing who would do me a deal, but i was fairly sure I could get one.

Maybe the best route for you especially given the fact that you like Fidelity’s platform is to write to the Chief Exec of that and put forward your concerns and wishes with the intimation that you can secure a deal with another provider if they do not give you a deal.

I think it is definitely a case of money talks and it needs to be big enough to have clout. I would appreciate if you didn’t use my name in anyway.

LikeLiked by 1 person

Very helpful – thank you. Rest assured I won’t mention you. If I get somewhere I will report back!

LikeLike

With regard to private banks, I agree the problem is how to pay them for services, without letting them have any discretion over your portfolio. My solution came up somewhat by accident. When I took fixed protection on my pension in 2012, I decided to set up an offshore life insurance bond. I decided to use a top-tier US private bank that was around 10bp/annum more expensive than the best price. This gave me a better service and better credit quality bank as custodian but most importantly it meant I was paying the PB some fixed admin fees and about 40bp running on the NAV of the bond. This added up to ~ $10k/year.

I could have shaved 10bp/annum off the cost using a IFA/Lux bank combo but that would have only been $2k/year better. The US PB does provide some great services for that extra charge. FX spot and forward transactions are executed at prices very close to the professional market (perhaps 1.5pips wide in GBP/USD). Bid/offer is lower in most stocks and ITs; they work orders far more intelligently than a typical online broker like HL. I can easily short stocks, ITs etc. They provide me with a credit facility at a very low rate which I collateralize with securities (essentially a margin loan). I don’t use it to be honest but it’s nice to have it on tap.

LikeLiked by 1 person

That’s fascinating. Your USA PB sounds rather more value-added than mine. But I think Interactive Brokers offers very similar benefits (amazing fx rates, shorting, loan, not sure about bid/offer) : have you checked them out?

P.s. I was BBC Model B!

LikeLike

The issue with IB is that their pricing deteriorates once you go off-piste. They are fine for G10 fx and single stocks but only ok in EM fx, weaker in longer dated fx forwards and fx options and virtually non-existent in fixed income products (say eurobonds or IRS).

LikeLiked by 1 person

Fair enough. You are well ahead of me here. I don’t even do EM fx, let alone forwards or fx options. But thanks for sharing – very useful perspectives.

LikeLike

First post here, come via Monevator and zxspectrum48k.

Interactive Brokers (IB) is limited as:

– No support for ISAs.

– SIPPs aren’t supported at all well (only a few SIPP providers will work with them).

For those of us 100% tax wrapped, that rules IB them out.

LikeLiked by 1 person

Jon – fair point. Though for unsheltered assets or even Ltd company investments they are hard to beat.

Thanks for your support.

LikeLike

Great post, very interesting to see the numbers. I happened to have a chat with an IFA/broker hybrid the other day, after a friend suggested they had the route that could enable me to raise a mortgage against my investment portfolio (rather than income etc). (I think you and I have discussed this before, when you did your dream house raise?)

I don’t particularly want to buy a property right now, but I was curious.

And what a curious meeting it was. After we both agreed my income didn’t amount to much in buying a hovel in London terms (especially after my big SIPP contributions, which were clearly discretionary to everyone, apparently, but a wealth manager) we turned to the portfolio.

Which let’s remember I’ve built *without* the benefit of an outsized income.

And I’m asked something like: “And of course as part of getting granted the mortgage I take it you’d be happy to move your portfolio into a fund managed by the institution instead?”

Um.

No. Thank. You.

We’re looking at a portfolio that I’ve built, under my auspices, both agreeing it’s turned a little into a relative lot. In any sane world, that’s the bank’s security right there.

But no, they’d rather lend high six figures to somebody who got a big pay rise three months ago.

Ho hum! 🙂

LikeLiked by 1 person

Thanks! I was hoping you’d like this post 😉

Asking for a discretionary mandate is their opening gambit, yes, but they won’t insist on it. Try asking if they’d settle for you moving the funds into an execution-only account. Basically they need the ability to trade it instantly without your consent. But they don’t need discretion to manage it. The downside for you is that any trade you want to make needs to pass credit ctte clearance, which can take a couple of hours. And of course you won’t get £10/txn trading fees. It’s not too bad but it wouldn’t suit day traders.

LikeLike

Cheers for thoughts; interesting a negotiation is possible, though suspect I’m on the low-side of the private banking bell curve to have much leverage. 🙂 I also don’t really think that free-via-Big-Brother solution would work for me either, but it would be infinitely better than a returned-draining managed fund.

The IFA is out hunting for someone who can give me the true flexibility I need. I’m not holding my breath! 🙂

LikeLiked by 1 person

It must be time for you to check out Interactive Brokers. They will lend you £500k GBP at 1.298% or £1.0m GBP at 1.13%. No IFAs involved and rock-bottom-low fees. Paperwork all done online too.

LikeLike

[…] his wonderful post this week about the dangers of private banking, FireVLondon admits […]

LikeLiked by 1 person

Hi FvL,

Thanks for the comment – I feel like I have finally made it in the FI Blogosphere 🙂

I should get my years statement in January, and as I track month on month I can probably do a breakdown of costs, returns and charges for both my personally managed one, and the one managed by my IFA – maybe have a chat in the new year and I can see what we can share 🙂

That said this year it will be skewed due to moving a previous employers pension over to them.

As others above have said – I would not go with one who charges an AUM fee each year – I accept that I pay 0.5% on all contributions, but when I measure my IFA I base it on what I pay in (i.e. the full £100 rather than £99.50) so that this gets covered. For me the Value Add I get is that they look across my entire portfolio (they know what is in my ISA, but openly said they are not interested in taking it on as they know I enjoy looking after it), and also help on the tax planning front.

Cheers and sorry for the delay in replying!

London Rob

LikeLiked by 1 person

Thanks LR. Would definitely be up for a chat in the new year !

LikeLike

Nice one – well when I get my statement I will ping you and let you know 🙂

LikeLike

[…] via Warning: private banking injures your wealth — FIRE v London […]

LikeLike

[…] This post is a follow-up to my September post – how private bankers injure your wealth. […]

LikeLike

[…] partly by banking an unexpected capital redemption from an illiquid high-fee investment the private bankers sold me, and partly thanks to the sale of another illiquid investment. This has pulled my Loan To […]

LikeLike

[…] At some point in Q2 I updated my expenses calculations from scratch. I can’t remember what difference this made, but it suggests my overall expenses are now only 43bps (versus 55bps reported in Q1). I don’t think this drop is completely accurate; I think my Q1 figure was overstated, but some of this drop is real – based on exiting some expensive holdings and deploying incremental funds into low cost places. Whatever the actual number, as before, my expenses are significantly inflated by my stubborn loyalty to a private bank. […]

LikeLike