With all the Neil Woodford news at the moment, you could have missed the fact that world equity markets are up over 12% so far this year. In GBP, at least. This rising tide has taken me over an important high water mark – my portfolio has recovered to where it was at before I raided it to buy the Dream Home.

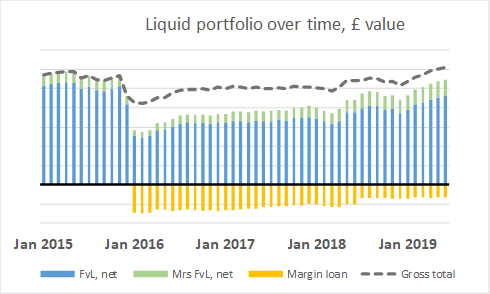

For those of you who missed the whole stressful saga, I bought my Dream Home, on a whim, in December 2015/January 2016. To make this more complicated, I ended up funding the purchase very significantly through a margin loan – basically a loan secured on my equity portfolio, rather than a loan secured on the property.

Buying the Dream Home needed me to sell almost half my investment portfolio. I was doing this in the middle of a minor market correction (global equities were 15% off their peak), which felt like a very painful time to sell. In the end, by borrowing over £2m I was able to keep £2m+ invested that I would otherwise have sold.

In those first few weeks after I completed I was pretty exposed. If the market had dropped 30% I would have been panicking. Fortunately, as hindsight shows, it turned out very differently; world equities are up almost 60% since then. Brexit has ‘helped’ here, because the sharp fall in the GBP after the June 2016 referendum meant my (mostly overseas) investments sharply gained versus my margin loan; this is not easy to see in the graph but it is there if you look closely.

With a combination of my investment returns, some liquidity windfalls, my net position (of the liquid investment portfolio, which ignores properties, illiquid holdings, etc) is up around 90% since my Dream Home purchase. I’ve paid down over half the margin loan, and my leverage now is at a very modest level that carries (I believe) very low risk. Thanks to this leverage, in fact my total gross holdings are now bigger than ever before. My net position isn’t quite at record levels, but it is well within the margin of error – and ahead of September 2015, a few weeks before the fateful Dream Home decision.

As an aside, the rental income I’ve received from the old house (which has become an investment asset, albeit not one that I include within my investment portfolio on this blog) has not been a big factor here, because in practice I’ve used those funds to both pay for the old house costs, as well as fund the significant running costs of the Dream Home.

I didn’t anticipate recovering my investment portfolio in under 4 years, without selling the old home. It feels good to know that my money can work so hard in such a short time. So, time to buy another one? Dream on!