With all the Neil Woodford news at the moment, you could have missed the fact that world equity markets are up over 12% so far this year. In GBP, at least. This rising tide has taken me over an important high water mark – my portfolio has recovered to where it was at before I raided it to buy the Dream Home.

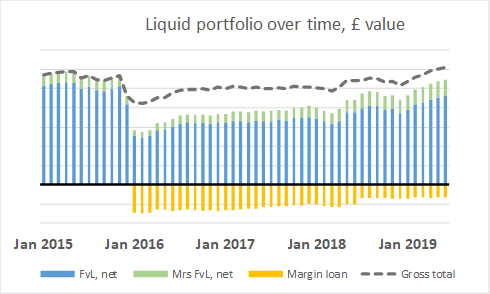

For those of you who missed the whole stressful saga, I bought my Dream Home, on a whim, in December 2015/January 2016. To make this more complicated, I ended up funding the purchase very significantly through a margin loan – basically a loan secured on my equity portfolio, rather than a loan secured on the property.

Buying the Dream Home needed me to sell almost half my investment portfolio. I was doing this in the middle of a minor market correction (global equities were 15% off their peak), which felt like a very painful time to sell. In the end, by borrowing over £2m I was able to keep £2m+ invested that I would otherwise have sold.

In those first few weeks after I completed I was pretty exposed. If the market had dropped 30% I would have been panicking. Fortunately, as hindsight shows, it turned out very differently; world equities are up almost 60% since then. Brexit has ‘helped’ here, because the sharp fall in the GBP after the June 2016 referendum meant my (mostly overseas) investments sharply gained versus my margin loan; this is not easy to see in the graph but it is there if you look closely.

With a combination of my investment returns, some liquidity windfalls, my net position (of the liquid investment portfolio, which ignores properties, illiquid holdings, etc) is up around 90% since my Dream Home purchase. I’ve paid down over half the margin loan, and my leverage now is at a very modest level that carries (I believe) very low risk. Thanks to this leverage, in fact my total gross holdings are now bigger than ever before. My net position isn’t quite at record levels, but it is well within the margin of error – and ahead of September 2015, a few weeks before the fateful Dream Home decision.

As an aside, the rental income I’ve received from the old house (which has become an investment asset, albeit not one that I include within my investment portfolio on this blog) has not been a big factor here, because in practice I’ve used those funds to both pay for the old house costs, as well as fund the significant running costs of the Dream Home.

I didn’t anticipate recovering my investment portfolio in under 4 years, without selling the old home. It feels good to know that my money can work so hard in such a short time. So, time to buy another one? Dream on!

Hi FvL – that is a great achievement, taking that risk has really paid off.

Now here’s a question that I often ponder. What are your thoughts on Sterling? Are we going to suffer shortly when it strengthens again? Or do you think this is the new norm?

LikeLiked by 1 person

‘thoughts on Sterling’ – first and foremost, I don’t believe my thoughts on sterling are worth tuppence, versus the market’s. I always take the current forex rate as broadly right.

This being said, it feels to me that if we ‘no deal’ Brexit, then GBP will fall further – my hunch is to parity with the Euro – i.e. about 10-15% more. If for some reason we revoced / sustainably remained (I can’t see how) then I think GBP would bounce upwards by about the same number – i.e. about 15% – here I think in terms of the USD and think we’d be back up to $1.45-$1.55. If we exit under a deal then my hunch is we will remain roughly in the GBP1:€1.15:$1.30 sort of rates for a while yet.

LikeLiked by 1 person

Amazing achievement FvL, congratulations.

You’ve successfully traversed margin lending, rollercoaster markets, FX fluctuations, political uncertainty, a weakening property market, opportunity cost, and the inevitable fear of the unknown. That is a remarkable achievement, given the backdrop of the last four years. Simple in hindsight, but hair raising while living it.

I’d be very interested in reading a write up about the psychology of that journey in retrospect, perhaps with an annotated chart illustrating the impact your FX denomination decisions and so on had along the way. It would make a fascinating compare and contrast exercise against the occasional posts you had written mid journey.

LikeLiked by 1 person

Thanks {indeedably}.

My quarterly writeups are really your best guide to my psychology in retrospect. I don’t think of myself as making FX denomination decisions. But perhaps I do – maybe I’ll find the time to do the annotated chart for you!

LikeLike

That’s pretty good going FvL!

I think you must have a stronger constitution than me to have psychologically coped with the first bit. On the other hand, I don’t think there was an outcome which would have seen you in complete penury.

That’s definitely an advantage to working towards ‘fat FI’: once you’re comfortably wealthy, you can take reasonably big risks and know that even if you have to eat the downside, you’d still be reasonably comfortable.

LikeLiked by 1 person

Massive congratulations, well done FvL!

Four years ago, it seemed (to me) a gigantic mammoth task to recoup the equity, but you’ve gone and done it in a relatively short space of time.

With a record like that, you could market yourself as ‘Fire v London Income Equity Fund’ and do better than Woodford – I’d take my chances and would make an investment! 🙂

LikeLiked by 1 person

Doing better than Woodford is a pretty low bar – you have been thrashing him yourself! Maybe we should team up….

LikeLiked by 1 person

It looks to me like you were geared about 41% which uplifted your returns from 49% to 69% and then your liquidity windfall and presumably extra savings from income have added another 21% to put you 90% up. Is that about right?

If so, then 41% gearing was brave, and 49% returns against 30% for the FTSE All Share is very good.

LikeLiked by 1 person

Not sure about exact numbers but yes that is broadly right. Main reason for outperformance vs Ftse is global particularly USA exposure when Brexit ref hit uk economy/GBP by 20pc.

LikeLike

[…] Firevlondon has paid off his dream home in four years (31) – Envy aside, massive congratulations that the margin loan gamble paid off! […]

LikeLike

Wow congrats. I hadn’t realised how wealthy you are. If you ever get tired of London, or want more space, then you can get a footballer’s mansion near where I live! Not sure I’d want a massive garden to maintain but they get local firms to do all the work.

Not sure you blog needs renaming?, as Fire to me as I see it, is for more modest wealth, where you build up to a 4% SWR and retire early, and draw it down from that point.

Each of us are different, but surely comes a point of “enough” or is the point to leave the max poss to your family? Take care, summer is here!!

LikeLiked by 1 person

[…] saw me both recover my investment portfolio to roughly the level I started at before blowing a large chunk of it…, and also finally officially Double my portfolio (ignoring additions/withdrawals) since the start […]

LikeLike

[…] recently declared victory on his approach of using margin lending to purchase his dream […]

LikeLike

Greate article. Keep writing such kind of info on your blog. Im really impressed by your site.

LikeLike