Supposedly Albert Einstein called compounding the 8th wonder of the world. Certainly the wonder of compound annual growth rates is something I feel quite viscerally, the more so with each month that I track my portfolio. But I’ve been struck recently by a radical improvement in my portfolio’s dividend income, far in excess of the portfolio’s return, that has occurred thanks to the margin loans I’m using. For anybody curious about margin loans, this blog post shines a light on what’s happening.

While my portfolio has grown 14%…..

As a quick visit to my Monthly Returns page can see, my portfolio has returned around 20% over the last twelve months (to September 2024 inclusive). This is a good, but not exceptional period over the 10+ years I’ve been tracking my portfolio – which has returned just over 9% p.a. since inception over 10 years ago.

As it happens, despite the underlying returns of around 20% my own portfolio (and I’m excluding Mrs FvL’s in this analysis) has only grown in size by 14% over this twelve month period, thanks to some significant withdrawals to pay tax bills, make ‘off balance sheet’ investments, and such like.

… my net investment income has grown 56%

What caught my eye is that my expected investment income, something I record monthly, has grown 56% during the same time period.

This post drills in to the niche that I have found myself in – of having an uncomfortably high level of leverage margin during a bear market. None of this is worth trying at home so for you to continue reading I assume you are anticipating some schadenfreude, car crash blogging, or perhaps some material to share with your crazy crypto mates.

I have become quite a fan of margin lending. Just reviewing first of all the journey I’ve taken…

Normal mode: 10% leverage

I first dabbled with margin lending, literally on the margins, about 10 years ago. More recently, about five years ago, I decided to use the lending strategically, and for several years I set my target asset allocation to include approximately a 10% level of margin – i.e. I own assets amounting to 111% of my portfolio value, having borrowed 11% to fund the purchase; the 11% loan is 10% of the total asset value. I consider this level of leverage to be minimal risk, because the dividend yield off such a portfolio will, under auto pilot, pay off about a third of the loan every year, even if the markets suffer significant falls.

Two key leverage ratios

For completeness, I should mention the rest of the debt I hold. I have a modest level of mortgage debt on investment properties, on a mixture of interest-only and repayment arrangements. These investments generate significant free cash flow, which is mostly used to (over)pay down mortgage principal. I have no other significant debts. Unless otherwise stated, I ignore the mortgages when talking about my leverage level.

In terms of affordability ratios, in normal mode my total loans (including mortgages) amount to about 4x my income (including investment income), and about 10% of my net worth (including properties). Nothing here that would give my bankers too much trouble.

Unorthodox procedure 1: buying House 1

A key moment for me was when I took a large risk in 2016 by buying my Dream Home with a margin loan. I pushed my Loan To Value temporarily up to almost 40%. To be fair the Value here wasn’t my entire household net worth, it was only my own liquid portfolio, but it was still a level of leverage that could have caused me trouble. Fortunately, for a reason of anticipated reasons (windfalls I was expecting) and unanticipated reasons (Brexit hitting the pound, which reduced the value of my loan against my global portfolio) and the extended stock market boom, I never looked back from that initial high level of leverage, and four years’ later I had my leverage back down to 10% again.

It is worth highlighting the simple arithmetic behind my leverage fall from 38% to 10% over four years. Falling from 38% to 10% is a drop of almost 75%. And indeed during that time, my loan shrank significantly, but ‘only’ by 55%. At the same time my gross assets increased in value by 51%. The combination reduced my loan as a % of total value by ~75%, to 10%. Rising markets hide naked swimmers, and they rapidly reduce leverage (which is why we should expect western governments secretly to support inflation for a few years yet).

Last week was the worst week since, well, a very nasty week quite a long time ago. And this week has started even worse. We are now officially into S&P correction territory.

Jeremy Grantham types (thank you @Monevator for the link) will tell you this wolf has been lurking just around the corner and we had it coming.

Typical, really. Just after I have leveraged up. And published a piece about ‘feeling rich’. Maybe I caused the global stock market drop, through sheer hubris? Just to compound the sense of nemesis , I am about 3% overweight on USA equities going into this correction.

When is a fall a fall?

Mind you, the fall has barely started. Jeremy Grantham describes how these corrections start with the riskiest stuff. Maybe that is why, until today, FTSE hadn’t moved yet.

In fact my portfolio – and its graveyard – are full of surprises.

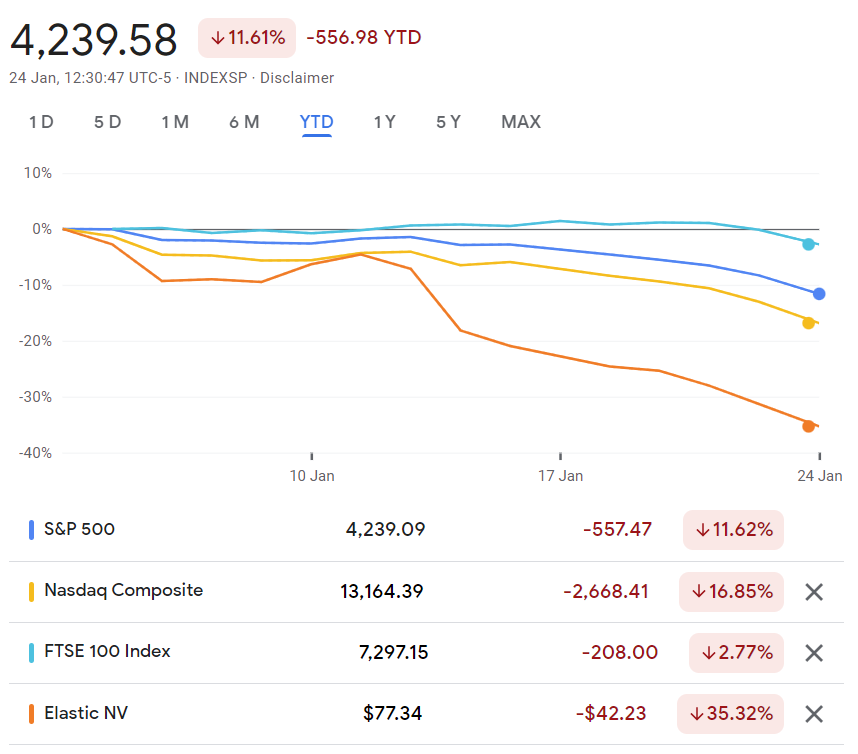

I have a few ‘spec tech’ holdings that are down over 30% – e.g. HUBS, DOCU, ESTC. So is Homeserve, though Homeserve’s decline pre-dates the recent woes by several months.

And my big tech is down materially – Amazon down to $2800, MSFT, GOOG and so on down 12-15%. Not nearly as big a drop as the ‘spec tech’ but more impactful to my portfolio due to my substantial holdings in a couple of these.

Key indices, and a sample ‘spec tech’ stock, performance year to date

But, reflecting FTSE remaining at 7300+, some stocks I gave up on a while ago though are doing OK – HSBC is above £5, and Shell is above £20.