Longstanding readers will know that I have been an avid user of leverage, ever since I used it to buy my Dream Home in January 2016. At that point I was able to borrow funds, very flexibly, secured on my portfolio. And rates were well under 2% in all major currencies.

When I started my leverage journey, I was borrowing over GBP1m, in a ratio of 3:2 GBP:USD. The rates on both were, from memory, between 1% and 1.5%. At this point the interest is more than covered by the after-tax dividend income on the securities, leaving any capital gains or untaxed income as leveraged upside. My main concern from having debt was not the financing cost, but the leveraged exposure it left me with – a 10% drop in markets would have hit my portfolio’s value by around 15%, and potentially left me vulnerable to the bank calling in some of the debt (via ‘margin calls’).

Since January 2016, base rates have started to climb – for the first time since the Global Financial Crisis in 2008. This change was long heralded and a long time coming.

I’ve been aware of the change in rates posture, but not been paying too much attention. After all UK base rates have risen to only 0.75%. Euro rates haven’t changed. But I must admit I had somewhat missed the fact that US base rates have risen above 2%. Two per cent! That’s becoming a proper base rate.

In the meantime, I’ve succeeded in reducing my leverage very significantly. In debt terms, by around half. In loan-to-value terms, by more than that – because my portfolio has grown as my debt has shrunk.

I recently reviewed the rates I’m paying for my margin loan and finally clocked that now my USD debt is costing me over 3.25%. IB’s rates start at 3.7% and then drop to 3.2% up to $1m of loan. This much higher interest rate has made me reconsider my target leverage.

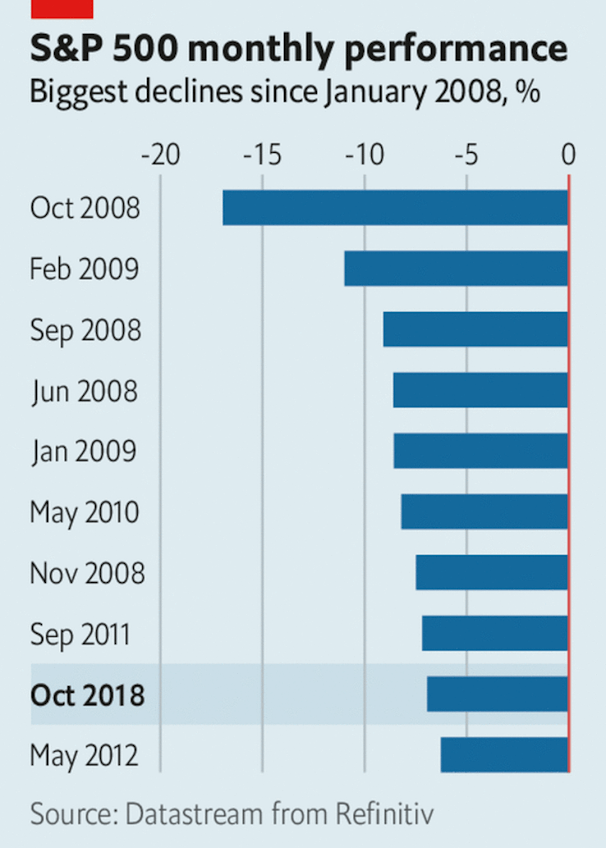

With USD rates over 3%, but my loan to value being around 15%, my main concern now is the financing cost / spread, not the level of exposure/risk. Paying interest of over 3.25% out of after-tax income now requires yields of 6% or more, which is getting into ‘high yield’ securities only – something that I know from experience tend to deliver pretty poor total returns. Of course capital gains may yet deliver an overall gain, even after tax and interest costs, but that is much more of a gamble than I faced two years ago, especially with October’s correction still a very recent memory.