Longstanding readers will know that I have been an avid user of leverage, ever since I used it to buy my Dream Home in January 2016. At that point I was able to borrow funds, very flexibly, secured on my portfolio. And rates were well under 2% in all major currencies.

When I started my leverage journey, I was borrowing over GBP1m, in a ratio of 3:2 GBP:USD. The rates on both were, from memory, between 1% and 1.5%. At this point the interest is more than covered by the after-tax dividend income on the securities, leaving any capital gains or untaxed income as leveraged upside. My main concern from having debt was not the financing cost, but the leveraged exposure it left me with – a 10% drop in markets would have hit my portfolio’s value by around 15%, and potentially left me vulnerable to the bank calling in some of the debt (via ‘margin calls’).

Since January 2016, base rates have started to climb – for the first time since the Global Financial Crisis in 2008. This change was long heralded and a long time coming.

I’ve been aware of the change in rates posture, but not been paying too much attention. After all UK base rates have risen to only 0.75%. Euro rates haven’t changed. But I must admit I had somewhat missed the fact that US base rates have risen above 2%. Two per cent! That’s becoming a proper base rate.

In the meantime, I’ve succeeded in reducing my leverage very significantly. In debt terms, by around half. In loan-to-value terms, by more than that – because my portfolio has grown as my debt has shrunk.

I recently reviewed the rates I’m paying for my margin loan and finally clocked that now my USD debt is costing me over 3.25%. IB’s rates start at 3.7% and then drop to 3.2% up to $1m of loan. This much higher interest rate has made me reconsider my target leverage.

With USD rates over 3%, but my loan to value being around 15%, my main concern now is the financing cost / spread, not the level of exposure/risk. Paying interest of over 3.25% out of after-tax income now requires yields of 6% or more, which is getting into ‘high yield’ securities only – something that I know from experience tend to deliver pretty poor total returns. Of course capital gains may yet deliver an overall gain, even after tax and interest costs, but that is much more of a gamble than I faced two years ago, especially with October’s correction still a very recent memory.

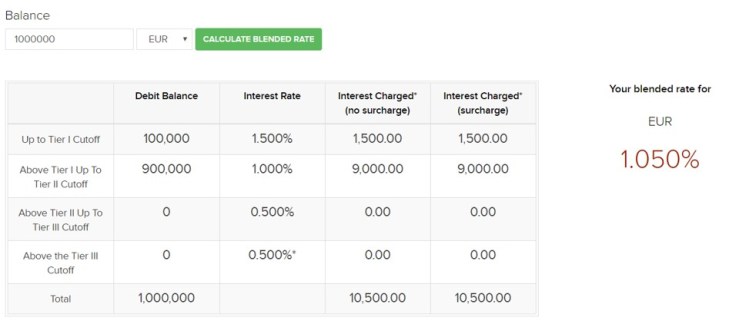

My immediate response is to shift my target allocation out of USD and into EUR and GBP. EUR in particular remains conspicuously cheap. Euro LIBOR is currently minus 25bps; a friend of mine has a margin loan (for his Eurozone ski chalet) which is costing him 100bps above base, i.e. 0.75%. IB’s rate isn’t quite this good but on €1m the blended cost would be 1.05%. My loan is smaller than this so I’m paying closer to 1.5%, this is still relatively cheap.

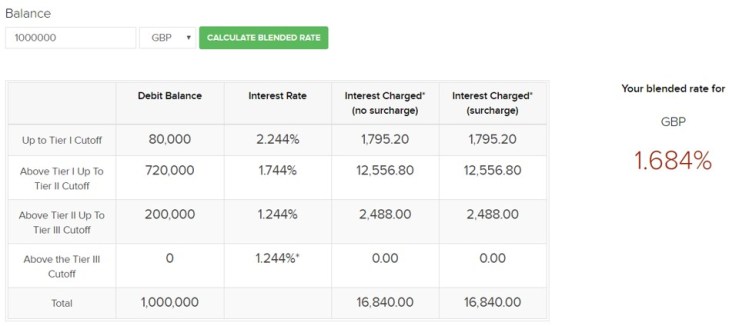

GBP rates start at 2.24% and drop to 1.74% for borrowing above £80k. Borrowing £1m costs 1.68%. This is slightly more expensive than EUR, but then the GBP is generally a weaker currency (not that you’d know it if you listen to Brexiters) – so GBP debt tends to fall in value vs EUR debt.

I know the forex experts like ZXspectrum48 will doubtless shake their heads in horror at my approach, but to my simple mind the idea of borrowing at <2%, when I have commensurate equities yielding 3% or more, makes me much happier than borrowing in USD at over 3%, against a pre-tax dividend yield of less than 3%. I don’t have a particular view on the direction of USD vs EUR so I am assuming they stay pretty constant relative to each other (cue more head shakes).

The actual like-for-like costs at IB of borrowing £1m in different currencies work out as follows: 1.684% for £1m GBP, 3.130% for $1.28m USD and 0.982% for €1.14m. This saving for borrowing in EUR feels pretty compelling, so I’ve adjusted my target debt allocation today from 2:10:3 Eur:GBP:USD to 3:10:2, and I’ve made the change in my actual exposure too. This doesn’t feel like much but results in a chunky five figure forex trade between USD and EUR.

Don’t try this at home.

Hi – Why not have the equities and the margin debt in the Investment Company? Then the dividends are tax free, and the margin interest is tax-deductible… Am I missing something?

LikeLiked by 1 person

Very good Q, @CyclingHedgie.

Even having tax-free divis only reduces, not eliminates, my general point about the spreads between financing costs and dividend income being much lower.

Yes, I do indeed have equities and margin debt in the Investment Company. I don’t have as much margin there as I should – it arguably should be margined up to the max, and let me reduce debt in other accounts, but in practice I haven’t bitten that bullet yet.

More to the point the Inv Company still has a minority of my total portfolio. I could be more efficient but I worry about the loss of flexibility/etc that would result, and I’m a bit afraid that I don’t know what I don’t know yet about it.

LikeLike

In conjunction with the loan currency change are you changing how you’re deploying the capital you’ve borrowed? I.e. you are now buying EUR assets with the funds from the EUR loan? Or has the underlying deployment of the borrowed capital not changed, and you’ve just taken an EUR loan, converted it to USD and paid back your USD loan?

LikeLiked by 1 person

@Grasmi – good Q. I increased my International Equities allocation significantly a few months ago, and I have been persistently underweight vs the target since. Slowly buying into VFEM, H50E, MEUD, and others to up my exposure.

With yesterday’s loan shuffle, I also opened new positions in BMW/DAI (~6% yield and reasonable valuations) to accelerate this behaviour. So, a bit of both approaches.

In effect my upping of my Intl loan target (from -2% to -3%, a 50% increase in the loan) was playing catch up with my upping of my Intl Equities target (from, if I remember rightly, 15% to 20%, a 33% increase). This still leaves my International column relatively underleveraged, at -3 versus 24% (20% equities, 4% fixed income), about 12% leverage. Most of my leverage is UK, which feels appropriate.

LikeLiked by 1 person

Very difficult to square these things away entirely. Really need to look at the sources of earnings from underlying components of the ETF (e.g. US listed behemoth – MSFT – with earnings coming from intl sources) which is quite some task.

All the same, I guess it wouldn’t be a bad thing to try and keep the assets and liabilities FX balances somewhat in mind when managing your target allocations, just in the off chance there’s some major unexpected event which drives a large move up in your debt balance currency, and sends your assets, relatively speaking, south. Although with the Italian budget and bond situation at the minute, perhaps the opposite is more likely!

I’m not using any margin at the moment – I’m trying to hold off until we have a large leg down in the markets. Will I actually be able to pull the trigger in the Armageddon scenario (and will rates be reasonable in this environment to warrant it?) – only time will tell.

Very interesting to hear about your endeavours all the same! Best of luck with it.

LikeLiked by 1 person

Geared to the gunwales? Extremely courageous, Minister.

LikeLiked by 1 person

Interesting window, as ever. My concern this time is “I must admit I had somewhat missed the fact…”

Full marks for the candour — people too rarely admit their flaws online — but think might be appropriate to take action to ensure this doesn’t happen again!

(I was fully aware how the US yield curve have shifted, and I’m not in hock in $$$ 😉 )

Perhaps there is there some kind of service you can sign up to that sends alerts when 25 basis point moves or similar? (Heck, maybe even Alexa and Siri will do it for you nowadays).

Would be more comfortable with this whole operation if we didn’t sit on top of the Forex equivalent of a case of TNT, but as we’ve discussed before You Have Dared And Won So Far so just take my fretting as an extra margin of mental safety! 😉

LikeLiked by 1 person

All good comment. My leverage strategy is not so sensitive to interest rates that me failing to notice for a few months exactly where the US yield curve had shifted to is a worry for me.

I’m curious about your TNT / Forex analogy… I consider my strategy to be fairly appropriately hedged for TNT explosions – what am I missing?

LikeLike