I was pleased to have reached the 10 year point of tracking my investment portfolio last month.

But my net worth includes an important asset class – property – that I don’t normally track, but which I have held in some form for over 20 years.

So, this post takes a look at how my real estate assets have performed.

Real estate works completely differently, for me, than my investment portfolio. For starters, I have never bought a home as an investment. But let’s start at the beginning.

My property owning history

I nearly got on the property ladder in the mid 1990s.

I hadn’t realised, until a friend pointed it out a few years too late for me, that in fact one of the easiest times to get on the property ladder was the moment when I graduated and moved to London. My first job earnt a reasonable London salary of just over £20k, and 1 bed flats in a reasonable part of Zone 1 in London were available for under £70k (now £800k-£1m, sigh).

Mortgage rates had dropped from >13% in 1990 to around 7%. The interest costs could have been around £5k, a quarter of my first-job income. That was in the mid 1990s. It didn’t occur to me to buy a place, and of course those property prices were so high…..

By the late 1990s, buying a property had become a lot harder. But once I was earning £40k+ I decided to take the plunge. I found a reasonable 2 bed place very close to Zone 1 for £200k (now £500k). The mortgage (at around 7% interest, i.e. interest costs were £13k, a third of my gross income) and the deposit (£20k, if I remember rightly, for a 90% mortgage) were a massive stretch….. and then I was gazumped. By the time I reorganised, the places I wanted cost £220k+ and I couldn’t quite afford it.

A couple of years later, I had made a six figure windfall through work, and I was in a position to buy my first property without stretching myself. I plumped for a 2 bed Modern Flat in Zone 1, for around £400k. Having read skimmed Rich Dad, Poor Dad, I decided to leverage it – so I took out a £300k (75%) mortgage. By this point interest rates had dropped a bit – from memory my mortgage was about 5%. So interest costs were around £15k, and by this point I was earning £80k+, so I was relatively unstretched.

A few years later, with another windfall under my belt, I moved into my first Proper House, in a leafy London suburb. The Proper House (a.k.a. Former Dream Home) cost me around £1m, and I bought it with a 50% interest-only offset mortgage. I decided to keep the Modern Flat, and let it out. Along the way I stupidly tried a currency mortgage (for the Modern Flat), but after currency movements increased the size of the mortgage by about 10% I shifted it into a straightforward buy-to-let mortgage with a cheap provider I have stayed with ever since. I have repaid more than half of the mortgage, which now amounts to less than 15% of the value of the property.

I sold the Proper House a few years ago, after buying the Dream Home. And I have retained the Modern Flat, which has been let to tenants almost continuously over the last 20 years. I haven’t set foot in it now for several years.

So now I have two homes (the Dream Home and the Coastal Folly) and one ‘buy-to-let’ flat. I have only sold ever one home, the Proper House.

Analysing my returns

Considering the performance and returns of my assets is not a straightforward process.

For context, UK inflation over the 20 years from 2000 to 2020 averaged 2.0%.

The headline figures are reasonably straightforward.

Sell price versus buy price

The starting point is what has happened to the property values.

It’s such a shame that I didn’t buy a 1 bed flat in my neighbourhood in my first year in London. I could have achieved roughly a 10x price gain, over around 25 years. That’s around 10% a year. If I’d borrowed the majority of the money required, my equity would have grown a lot faster than that.

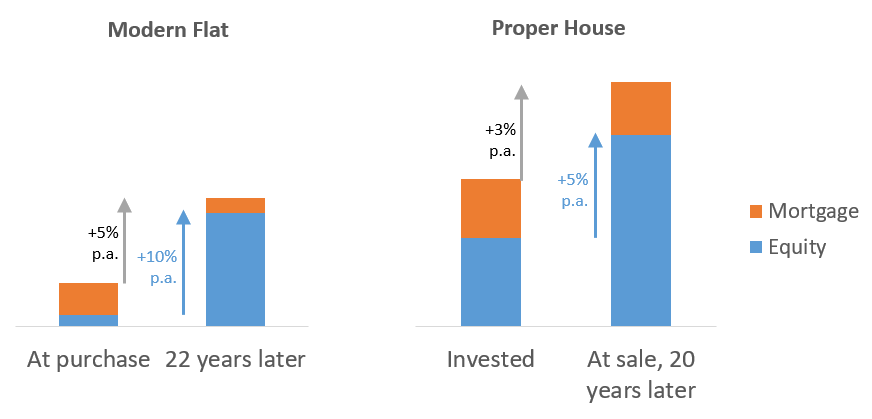

As to my Modern Flat, while I haven’t sold it I have a good idea what it is worth. It is worth around 3x what I paid for it, after over 20 years. That is about 5% a year. And I have invested no additional capital in the property after purchasing it, so this gross return figure is reasonably accurate.

For the Proper House, I have unambiguous entry and exit prices. And they make clear that the Proper House was not a particularly good investment. I sold it for roughly double what I paid for it, after 18 years. That is a gross return of around 3% a year. Allowing for the fact that I invested over £200k in upgrades along the way, my actual return was in fact a tiny bit lower than the gross return.

So the headline returns here are reasonably clear, and clearly not that impressive. But, just as when looking at a stock price now and then, it is not as simple as that.

Complexity one: leverage

The first adjustment to apply to my gross return is the leverage I took on. For both properties under discussion, a lot of the money involved was the bank’s.

For my Modern Flat, if you consider just my equity (without any financing costs taken into account), it increased 9-fold, an IRR of around 10%. That compares favourably to my equity/bonds investment portfolio. Crudely reducing my total interest expenses reduces the average return to 8.5%. Still quite an attractive number.

However for the Proper House, leverage makes much less difference. My level of leverage was lower, at around 50%. But the equity left when I sold the house had not much more than doubled, an average return of 5% pre tax.

There is a lesson here: when the equity returns are similar to the cost of debt, leverage doesn’t help. The average annual house price increases of around 3% were very similar to my average mortgage costs. As a result, for my Proper Home, leverage hasn’t helped me (ignoring the fact that I was able to use my own funds to invest in stocks/bonds, at a somewhat higher rate of return). Whereas for my Modern Flat, leverage has turbocharged my returns.

Complexity two: rental returns

I haven’t yet brought in either running costs nor rental income.

Again, the Modern Flat shines. Ignoring the few years I lived there myself, I have had rental income for around 15 years. Deducting interest expense, service charges, letting agent fees and so on (but not taxes), I have made a taxable surplus of over £10k-£20k per year from the Modern Flat (a very good return on my original ~£100k equity investment, though a much lower yield on a ~£1m asset). This surplus significantly juiced my returns, resulting in an IRR (pre tax, and on my equity investment) of over 12% p.a. That flattens anything I could have achieved via a normal equity-led investment portfolio. I have in fact been repaying my (cheap) mortgage; if I had not done this, returns would have been even higher – close to 15% IRR pre tax. Which of course is why debt is not always as evil as your mother warned you.

My Proper House is a different story. For most of my time owning this property, I lived there myself. I only rented it for a few years at the end. The rent resulted in a taxable surplus, after interest expenses and letting fees, of over £50k per year – partly thanks to how cheap my mortgage was at this point. As a rental yield, this was low. Though versus my total equity investment of over £700k, it doesn’t look too bad. But a few years of this doesn’t really touch the sides; my overall IRR pre-tax was still only around 5%.

Complexity three: running costs / imputed value of a ‘home’

So far I’ve ignored the period I actually lived in these homes.

During my occupancy, I had interest costs – quite high ones back in early 2000s. I had other running costs – council tax, utility bills, energy costs, etc. If I hadn’t lived in these assets, I’d have needed to rent a home elsewhere.

For the purposes of this analysis, I’m treating all the interest costs during the period I lived in a home as just ‘living cost’, and excluding these costs from my IRR calculations. Interest expense when the home is not occupied I treat as an investment expense.

For both properties, the capital gain is the most important driver. A simple assessment would equate mortgage interest to rent. The return then comes to the gain in value – on both the equity portion and the borrowed portion of the property. As the UK gives you 100% tax relief on the capital gain for your principal residence, those gains are literally where the money is.

When I moved into my Modern Flat, it was rapidly gaining in value. So even though I had interest costs of over £1k a month, the property was probably adding over £2k-£3k a month of value.

At the Proper House, I did quite a bit of work to the house after 10 years, which required over £200k of capital. I didn’t top up the mortgage so this was all additional equity. I don’t think I got this money back in full at sale. This work, while it improved the quality of my experience in the house, depressed my returns.

Complexity four: era analysis

In the discussion so far I am discussing the average annual return, by looking at the value at the end, the value at the start, and any sums committed/received along the way. That has produced average annual returns from 3% to 12%, depending on which property and which measure you look at.

In reality however, returns have varied considerably over the last 20 years.

It is hard to know for sure but I suspect my Modern Flat rose strongly for the first 10+ years I owned it, and probably reached £1.2m in value 5 years ago, and hasn’t moved since then. It may even have fallen thanks to the pandemic (as it has no outside space) and now rising interest rates.

Meanwhile I suspect that I overpaid for my Proper House, so it probably didn’t gain in value at all for the first five years I owned it. Thereafter I suspect it did gain by 5%+ per year, at least until the Brexit referendum. Since then, it’s not entirely clear – but I imagine it has done better after I sold it (just before lockdown, doh) – due to its outdoor space etc commanding a premium.

So from a returns optimising point of view, I would have done best to sell my Modern Flat five years ago. I think I could have achieved compound equity return of over 16% with perfect hindsight.

And finally, taxes

I’ve been ignoring taxes in this analysis so far. Well, almost – I have allowed for the stamp duty paid on purchase.

I’ve mentioned principal private residence relief, which ensures that had my homes been owned consecutively and sold as soon as I ceased having them as private residence, the returns cited above would more or less be my net returns.

In fact by turning a former principal residence into a rental property, you get walloped with two sets of taxes:

- Rental income is taxable as income. And mortgage interest is, these days, only partially deductible. So I have an ongoing tax bill of around 0.6% the (latest) value of the property (p.a.) for my ongoing Modern Flat. Expressed as a percentage of my original equity (not a very useful measure), this tax bill is around 6% per year.

- Capital gains tax relief is withdrawn. Capital gains on rental properties, on eventual sale, will be taxed pro rata to the portion of ownership spent as a principal resident (plus 9 months, in fact). This is a cashless tax charge, only paid on sale. But for my Modern Flat, it is quite a big number. Assuming my gain right now is around £800k, roughly speaking 5% more (about £40k) of this gain becomes capital gains taxable (at 28%) every year. So I have a roughly £11k additional tax bill every year. That almost wipes out any economic surplus I make from my rental property.

The combination of these two taxes means that unless my Modern Flat appreciates in value it is barely covering its costs, and its ongoing rate of return is somewhere less than 1% per year. When my current tenant moves out, I intend to sell it.

Conclusions

I need to re-state that I didn’t buy either the Modern Flat nor the Proper House with an eye to the investment return. I had read Rich Dad, Poor Dad before buying either – and so accordingly I viewed my own home as outside my investment scope. But by keeping the Modern Flat when I moved into the Proper House, I was effectively turning the Modern Flat into an investment asset.

Viewed as an investment asset, the Modern Flat has done well. Better, even, than my investment portfolio has done over the last 10 years. These figures don’t allow for the lack of transparency or liquidity, nor my time/effort with the property (which is low, to be fair), and involve making an assumption about what the flat is worth today. But either way, if you offered me the prospect of the same again over the next 20 years, I’d take it. You can certainly see the allure of property, when the prospect of gains like my experience over the last 20 years exist.

Unfortunately, the figures for the Modern Flat mask the current poor performance – which is lousy, thanks to stagnating London property prices and a Capital Gains tax liability that is increasing by £11k per year.

If I ‘bed and breakfasted’ my Modern Flat, i.e. replaced it with another similarly flat, I would crystallise and fix my Capital Gains liability. But I would now own an asset with a 3% gross yield. That wouldn’t be worth leveraging up, given that buy-to-let mortgages cost more than 5% currently. I could probably increase the rents, but not above 4% yield. Further capital gains could yet occur, nudging my returns up. But expenses, stamp duty and taxes all diminish returns dramatically.

And as to the Proper House, the only positive spin I can see is that it has protected me from inflation. But it has provided with only a 1% return above that. Compared with my investment portfolio, this sucked. And that’s before you consider the lack of liquidity or transparency that I have endured.

I strongly suspect that my two current homes will suck as investments. Both were bought for an emotional attachment and the appeal of living in them, not with an eye to the investment return. One was bought six months before the Brexit referendum. One was bought a few months before the Ukraine war spiked inflation, leading to interest rates climbing off their 15 month floor. So be it.

My future self won’t have any help from properties as investments. I need to stick to the public market portfolio, which suits me fine.

Informative analysis.

Looking back both your investments were great! You lived in them, experienced physical real estate, made money with them from tenants as well as protected your capital from inflation. With property you really need to be right about two things: time and location.

Still better than owning something like Land Securities where you had crazy volatility and no price appreciation in 20y but it was throwing out a yearly 5% taxable dividend yield.

Besides it’s good to own something outside of the electronic capital markets, just in case…

LikeLiked by 1 person

I am quite attracted to Land Sec / British Land / etc myself! But agreed you can’t come home at night to them.

LikeLike

I followed a similar path and ended up with a string of properties (unfortunately mine are scattered across the globe, which makes management somewhat interesting) in places I have lived over the years. Overall they weren’t terrible investments, but with hindsight, the money would have been better invested in equities. Unfortunately despite having done similar (but not as in depth) analysis a few years ago, I didn’t listen to the output and recently added another property to the portfolio by building a “dream home” on a tropical island. There’s something intangible about owning the place you live in that doesn’t show up in the spreadsheets.

With the most recent “project”, I acquired the land during the depth of the pandemic in a popular tourist area at favourable prices and I think I could double my money or more if I sold now, but I have no intention of doing that – I built it to live in – it’s not an investment, but the paper gain is nice to have in the back of your mind. Had I not built, I would be exposed to an out of control rental market – it’s not uncommon for landlords to put up rent by 50-100% when renewing contracts here at the moment for long term rentals, given that the tourist market is back in full swing. This is one of the factors that don’t show up in the spreadsheets.

I think I’m going to get rid of one of the properties soon just to minimise the management overhead and simplify my positions. I’m also sitting on a large capital gain in a zone 1 London flat, but the thought of paying the large CGT bill puts me off selling it, so I might hang on to that one (probably irrationally, but who likes handing over large sums to HMRC?).

I’ve had a nightmare with a property in Australia over the past few years where leaks were coming into the flat from outside of the building (outside my control) and the managing company were slow to repair it, which meant the flat was empty for the best part of a year. Originally the insurer said they would cover it, but then when I tried to finalise the claim they tried to wriggle out (not mentioning any names… Chubb) . Eventually, after threatening legal action, the insurance company paid up for the loss of rent, but I wasted a lot of time applying pressure to them and escalating to the ombudsman. It’s for this reason I’d like to cut down the properties. It’s just not worth the headaches like this, even if the returns were better (which they’re not), I just don’t want the headaches. To be fair though, I’ve had relatively few major issues over the past 20+ years I’ve had my places rented out – it’s mostly been fairly smooth sailing, but I look forward to a time when I never again wake up to a “the XXXX is broken” email from a tenant!

LikeLiked by 1 person

All good points, thanks for sharing! That ‘leak, outside my control’ scenario is one of my worst nightmares. I hear you on CGT bills tho I hate the thought of the unrealised number hitting my P&L ‘intangibly’ every year.

LikeLike

Interesting analysis, cheers! And I share your pain re: mid-1990s London property prices. Though I was stupider than you and had actually done the maths.

I was looking at a two-bed South London flat in what would eventually become a chi-chi sort of area (Clapham Old Town) near where I was working at the time… renting one bedroom to a friend even at a less-than-larcenous mate-ish rate would have covered the mortgage leaving me with just bills to pay!

Unfortunately I was £3-5K short when it came to getting the mortgage (the best LTV offer I could find) and I was too dumb to bite the bullet and buy down the road in Brixton (where I’d already lived and liked, but which hadn’t yet really started gentrifying and made me nervous as an investment. It would have done great!)

So began a 20+ year renting odyssey that only ended when I finally bought a London flat five years ago, at the thick end of your price appreciation, which I believe has indeed stagnated in price since (though the bank revalued it higher thankfully when it came to remortgaging / LTV bands).

Anyway, why not keep the London flat washing its face for a few more years in the hope that the tax situation changes? You never know, there might be some kind of regime change or offsetting capital loss (from memory you have unsheltered assets?) or some other use you can put it to. It hardly seems like a liability that you can’t afford to carry, and if you haven’t set foot inside in several years then it looks like you have the admin burden sorted too?

Just a thought, good luck whatever you do! 🙂

LikeLiked by 1 person

Useful input as ever – thanks! You are not the only one querying why I would sell the Modern Flat. There is a chance regime changes help me. There is also a chance CGT gets worse. So if the opportunity arises in the near term, I will try to take it.

LikeLike

I’m terms of investing, property is my clear area of underperformance. I always wait to long to buy, never buy large enough and always have too small a mortgage (or no mortgage at all). I’ve ended up with four of the buggers, all unencumbered, they are nothing but hassle and have underperformed my portfolio by around 8%/annum (14% for portfolio v 6% for property over 23 years).

Nonetheless in terms of asset liability management, I’m keeping them since it means I’ve essentially hedged my need for shelter. If the two rental properties assigned to my kids fall in value by 50% then the properties they want to buy when adults have also fallen by 50%. Conversely, if they double. I take some basis risk, in the sense that one is in London, the other Australia, so if they want to live in Manchester or New York, this may not be a good hedge. It’s the best I can really do though. I can treat myself as marketweight and just forget about houses entirely. Which suits me fine.

LikeLiked by 1 person

A nice example of your hedging approach, thanks.

The underperformance both you and I are chafing about implies that the portfolio represents the opportunity cost – i.e. I could have invested at 14% if I didn’t have that property giving me 6%. Of course, for one’s primary home, it isn’t quite that simple. Tho at this point in my life I am certainly not looking to invest more marginal dollars into real estate.

Another way to think about it thoughis that the portfolio is there to provide us with resources/etc to do things with – things we enjoy and get value from. Buying properties is one of those things. And on that basis, the property is not an investment. If it happens to deliver a return / track inflation as well, so much the better. Michelin star restaurants do not do this, Dream Homes might.

LikeLike