A new UK tax year has just begun, and with it a new annual ISA allowance of £20k each. ISAs are an amazing tax-break for investors who are UK taxpayers. I love them, and have a goal to get my ISA portfolio to £1m+. I’ve been posting updates annually about this (e.g. here, and the one before).

Why is being an ISA millionaire cool? The £1m mark is just an arbitrary number, after all – unlike UK pensions which are capped for most of us at £1m. A million quid maintains an allure, even after the ravages of inflation. And sensibly invested it should produce an annual income of £35k-£40k, tax free – whereas a £1m pension’s income is taxable, if it is taken.

Since the government lifted the allowance to £20k per person a few years ago (an un-noticed marriage tax break for wealthy, i.e. mainly Tory, voters), even ignorant ultra-conservative investors using just Cash ISAs can become ISA millionaire-couples in ‘only’ 25 years. But their £million won’t be worth as much as it would have been when they started, and they won’t benefit from tax-free compounding over the 25 years.

£20k here, £20k there and, pretty soon, you’re talking real money

ISAs in their current form started in 1999, when they replaced other tax-friendly savings arrangements such as PEPS, TESSAs.

Any single person who’d topped up their ISA to the maximum every year since 1999 would have, if they have just topped up their 2018/19 ISA, invested £206k in their ISA. If this money was invested in a low-cost FTSE All Share index tracker, with no withdrawals, it would today be worth around £380k. A married couple who have doubled up the whole way will be sitting on a combined ISA pot of double this, which is over $1m. So, in dollars, a pair of wealthy ISA-loving investors would be ISA millionaires if they have achieved market average returns over the last 19 years.

Being an individual ISA millionaire in pounds is much harder. But if you were saving hard using the PEPs/TESSAs that preceded ISAs, you had a crucial starting advantage. This is one of the ways that the most famous UK ISA millionaire, Lord (John) Lee did it. But if, once ISAs came along, you achieved only average market returns, you’d have had to begun your ISA journey with £187k of savings.

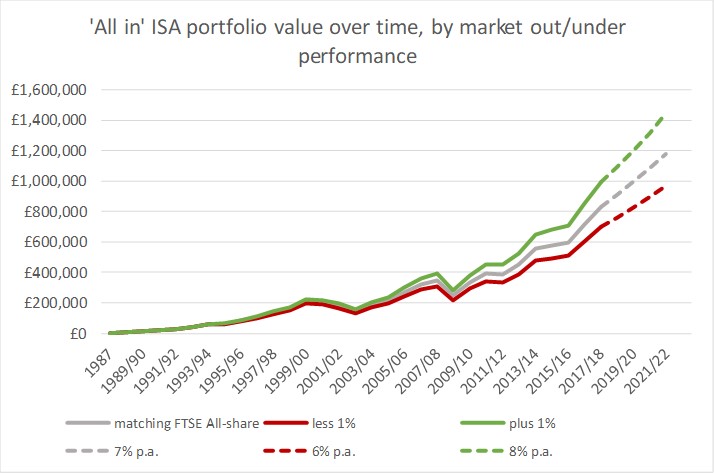

How could people have begun their ISA journey in 1999 with £187k savings? The Capital PEP, which would have been the best vehicle to have used, started in 1987 with an annual allowance of £2.4k. By 1990 it had risen to £6k. But this means the most you could have invested before 1999 was £64.2k.

What were the chances of turning £64k into £187k in 12 years? As it turns out, the chances were very good. The 1991-95 boom saw the FTSE All Share return over 20% per year in four of the five years. So an ‘all in’ PEP investor, achieving average returns, would have had £159k in their ISA account on day 1. Maintaining average returns and continuing to be ‘all in’ would have got them to around £850k today.

In fact, an ‘all in’ investor like John Lee would have only needed to outperform the market by 1% per year in order to cross the £1m threshold, which they would have done in the last 12 months. Outperforming the market by 1% per year is no mean feat, but there are certainly countless UK investors who have done it. Of course, in the recent Brexit-y era, the more of your investments were outside the UK the more you’ll have beaten the UK market.