As I mentioned in my January 2020 report, January is the tax deadline month in the UK. And it is the annual tax filing process where the overcomplexity in my financial affairs becomes most visible, and any problems created by that complexity become urgent and pressing.

In previous posts here and here I’ve discussed the complexity that has arisen in my financial affairs. Partly this is a quality problem, reflecting my higher than average net worth, and the journey I’ve taken to build my wealth. Partly this is deliberate strategy on my part – to diversify across providers, to make use of tax sheltered accounts where possible, to spread funds between me and Mrs FvL. And partly this is just creep – the equivalent of middle aged spread: it happens without you really noticing, until one day in January somebody takes a snapshot of you and you realise how unappealing the image is to outsiders!

Reflecting on the consequences of my overcomplexity, I think three problems nag at me:

- The burden I shall impose on my executors. I struggle sometimes to manage my finances. My other half, or my family/friends, or a trained financial/legal professional, would be left with a genuine labyrinth to navigate.

- The time I spend managing my money. As it happens, I am sad/bored enough to quite enjoy this. But I suspect I would enjoy it just as much if it took half as long, and I would find more productive/enjoyable things to fill my time.

- The hassle/time/expense of the annual tax filing process. Let me dig into this a bit below.

I have used the same accountant for years. She knows my affairs pretty well and we have developed a reasonable system/way of working over the years. My limited company has a separate accountant and process, who/which I am largely ignoring in this blog post. Here are some stats from my personal tax filing process for the last tax year:

- 82 files that I’ve sent to my accountant. These are statements, EIS certificates (for the UK angel investing tax breaks), payslips, etc. These 82 files do NOT include some important material my accountant gets direct from my broker/private bank.

- 69 pages: the number of pages in my tax return.

- 110 emails, exchanged between me and my accountant, over the last 12 months. This is going to cost me….

- 570 rows in my investment tracking spreadsheet, covering both me and Mrs FvL. One row represents one holding in one account across all our publicly traded investment accounts. We have about 200 holdings in total, so each holding is coming up in almost 3 places (e.g. in my ISA, Mrs FvL’s ISA, and my General Investment account).

- 10-20 hours a year of my time is spent specifically working on my tax admin each year. Plus at least double this on tracking my activities.

- 1800+ investment-related transactions for just 12 months in my tracking system on Quicken. This covers me, Mrs FvL, and my personal limited company’s liquid portfolio. Every single one of these transactions has been typed in by me. Of these, about 500 are of a dividend payment of less than £50.

I reflected over the Christmas break on what I might do to curb this complexity.

Firstly, I have multiple providers/brokers. I consolidated this list down significantly when I bought my Dream Home. However now I am consciously reexpanding the list, looking for more FSCS protection / diversification in case of Woodford/MF Global/etc blow-ups.

Secondly, I have a large number of holdings – around 200 in total, across me and Mrs FvL. Our portfolios contain over 100 individual stock picks, as well as 40+ ETFs and 30+ funds/investment trusts. But my smallest 50 holdings amount to only 8% of my portfolio’s value. This could be cleaner.

Next, my personal tax filing workload has made me appreciate that the complexity of my tax admin burden arises only from unwrapped accounts. For my SIPPs/pensions, which have a few dozen holdings in them, no filing is required at the moment except the amount of my annual contributions. For my ISAs (tax-free accounts), with another few dozen holdings, no filing/etc of any sort is required – I don’t even need to tell my accountant about them. So the ‘executor complexity’ is even greater than my ‘accountant complexity’.

Finally, I am an angel investor. The main complexity this creates is from EIS. Claiming the relief when I make the investment is fairly simple. However the reporting process upon exit can be quite tricky – especially if the exit is 10 year after the investment and you didn’t keep good records of what you invested in. If the exit happens less than 3 years after the investment, or if the company gets wound up, or the exit is paid for with another company’s shares, the complexity skyrockets. I don’t see much that I can do about this complexity; it is effectively a different form of tax.

Most of these factors are deliberate. Making changes is hard. But on the tax/admin point, I resolved over the Christmas period to undertake some radical actions, and significantly reduce the complexity of my unwrapped accounts. To this end I want to:

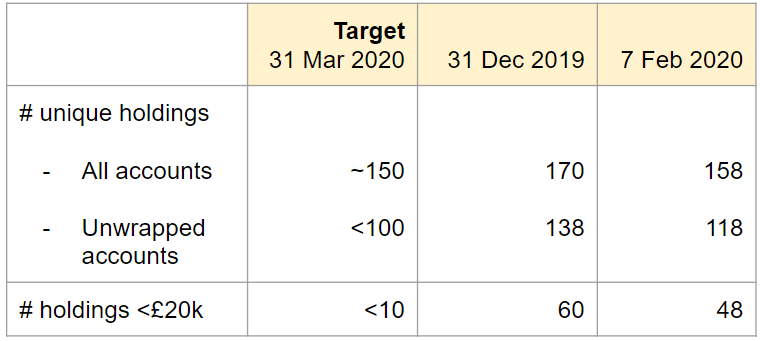

- Reduce number of unwrapped unique holdings to 100, from ~140. This might not sound that dramatic but it is quite a big step. And it needs to happen before the next tax year, beginning 6 April.

- To achieve this reduction in holdings, I need to concentrate my smaller single stock holdings in wrappers (ISAs/SIPPs), especially if they pay dividends. In several cases, to do this I am selling the unwrapped single stock, as well as a wrapped ETF, and then re-buying the single stock in the wrapper and the ETF in the unwrapped account. Warren Buffett would not approve – thanks to hefty dealing costs. Nor would @TheAccumulator – because I may end up with higher yielding/less tax efficient holdings unwrapped than before.

- Lift my minimum investment size to £20k, from £5k. This feels like good discipline. I also have in mind making <£50 dividends a rarity – so at least the effort of typing them in feels more worthwhile! In practice what this means is keep <£20k holdings on ‘watch list’ – either to build the position or close it. This is a natural consequence of consolidating my holdings. But it also says ‘play holdings’ are to go; they outweigh in complexity/hassle what they deliver in learnings/fun/etc. With the imminent influx of funds from selling the Former Dream Home, I will have an opportunity to top up my smaller holdings.

- Keep using the same range of brokers. This diversity is valuable to me. And the FSCS limit of €100k per account encourages multiple brokers. There is an argument for ensuring that my smaller accounts are only used for tax wrapped accounts, thus eliminating any tax reporting, but that adds even more complexity. So for now, I just have a lot of General Investment Accounts.

I’ve been doing quite a bit of work on this pruning exercise already this year, as shown below. My unwrapped accounts are already becoming significantly less complex. But I have a couple of large unwrapped portfolios that I will need to close out a lot of positions, and either open equivalent positions in a wrapped account or dispense with some much-loved holdings. Head and heart are currently fighting it out.

In any case, I hope to report more progress before too long. Then the real test is the size of my statements/accountant dialogue/log file next January. Talk about long term investing, tsk.

By my reckoning your compound annual growth rate is about 3.20% higher than that of the FTSE All Share Total Return Index over the past seven years. What impact do you think these changes to reduce complexity will have on your returns? Could they actually improve your returns?

LikeLike

Good question…. I have been wondering if, by reducing my long tail of investments, concentrating more on passive, etc I alter my returns profile. I don’t think I will; I think my ‘outperformance’, if anything, is my allocation (more to USA, some leverage at a crucial juncture), than my active stock picks.

LikeLike

I have a relatively complex portfolio but not as bad as yours …

I’ve never found the need to use a tax accountant for the personal self-assessment. Once you’ve got the data, filling in the self-assessment is fairly easy. I do use an accountant for the LLP and PIC but those are businesses. The process of collecting the data takes most of the time; adding an accountant into the mix would actually make it more complicated since these guys are pretty clueless. I think I’d apply the rule that if you need an accountant, it’s too complex!

I think your issue is simply the amount of transactions. I suppose you do trade single stocks and I don’t. So that maybe a major difference. I’m somewhat confused, however, why you have so much in unwrapped portfolios. Ok, the ISA/pension wrappers can be easily exceeded. I thought, however, you had an offshore life bond and a PIC? Why isn’t most of the residual portfolio in those vehicles? For me their value is a much about reducing tax points as about deferring tax. GIAs are a complete PITA.

LikeLike

@ZX48k – thanks for this – somehow I didn’t spot it – I blame wordpress.

You ask why I have so much in GIA. Broadly speaking because I have too much for wrappers, and somehow haven’t completely got my head around how I would ever get money out of the Ltd company. The Ltd has felt like ‘one of many’ pots, not ‘the main pot’.

As to my accountant, there are numerous aspects of my return that I would really not comfortably/confidently manage myself, and am grateful I have a professional overseeing it. EIS I have mentioned. My buy to lets are another. Charity donations/pension contributions I probably could get my head around, but I’m not 100% sure.

A key reason why I started with an accountant was multi-jurisdictional issues. These are now behind me, but having never had a scrape with HMRC in 20 years I do feel part of the reason why is that I use a belt-and-braces accountant, and I am pretty sure that the moment I stopped I will get an investigation!

LikeLike

re multiple providers/brokers:

I understand the FSCS protection issue, but, putting that aside for the moment, at some point the more providers/brokers you have the more likely you are to be with one (or more) that gets into difficulty. Do you have a method for deciding the “safest” number of providers/brokers to use?

LikeLike

The downside risk of one entity is the argument for diversifying into multiple entities.

I don’t know the number I’d use if I had £100m. The richest guy I know, a billionaire uses one main custodian so far as I know, choosing based on balance sheet rating (AAA, or similar) and relationships.

LikeLike

I have exactly the same problem. A tendency to dabble, lot’s of accounts, a wack-a-mole problem every time one gets significantly above the FSCS limit. I’ve worked in investment management long enough to be a bit cautious. Still I’ve had to relax a little: banks and v. large brokers I’ve allowed to grow to 3-4 x the FSCS limit, smaller, cheaper, riskier ones (x-o,IG,T212) I try to keep at or only slightly above.

It’s annoying that the risk vs fees and complexity incentives pull in different directions. But I guess there’s not much political capital to be made from increasing the FSCS limit, at least, not until the next crisis.

LikeLiked by 1 person

The FSCS maximum is one bit of EU red tape I’d be happy to diverge from! If it went up, obvs. As you say, not much political imperative for it.

LikeLike

I sometimes compare your returns to my implementation of the Tim Hale Return Engine portfolio which is passive and globally diversified. The returns are very similar e.g. 22.0% for calendar year 2019, with no bonds and no leverage. Scope for simplification there?

LikeLiked by 1 person

FvL returns can be compared to something like VWRL. VWRL has produced returns of +3.4%, +29.6%, +13.2%, -4.7%, +22.0% for calendar years 2015-2019. By comparison FvL has produced +3.6%, +24.0%, +13.0%, -4.5%, +22.7%.

So with the exception of 2016 (Brexit vote so probably down to different GBP/XXX currency weightings), the returns are quite similar. This is a bit odd given FvL has a 20% fixed income weighting (vs. VWRL which has zero) and some leverage (albeit not much). I haven’t looked at the monthly return numbers so there could be more obvious divergences at that level. FvL has a decent Sharpe so his portfolio might be somewhat less volatile due to the bonds.

The problem is that in a world where asset rallies it’s hard for any portfolio of conventional assets to show much divergence. The real test will be when markets go down.

LikeLiked by 1 person

[…] Fighting complexity – FireVLondon […]

LikeLiked by 1 person

[…] Fighting complexity – FireVLondon […]

LikeLike

[…] not sure why I ‘outperformed’, but I know that I was very busy in March. My complexity reduction activities went backwards, with many positions falling below my ideal minimum holding size of […]

LikeLike

[…] ignore my angel portfolio from the point of view of any net worth / FIRE / returns / allocations / complexity analysis. If I receive an exit from an angel investment, this windfall cash is often partially reinvested in […]

LikeLike

[…] the portfolio on autopilot the dividend income alone will pay off the debt automatically. Yet with my recent portfolio simplification, I now have very few holdings that pay out EUR income – and those that I have are mostly not […]

LikeLike

[…] Since early 2020 I have been trying to fight the complexity of my portfolio. […]

LikeLike

[…] and one I have been taking increasingly seriously since 2020, is how complex is my portfolio. I took significant steps in 2020 to simplify the portfolio. And I doubled down again in early 2023. This has left me with fewer […]

LikeLike

[…] next question in my annual process is: how complex is my portfolio? I took significant steps in 2020 to simplify the portfolio. And I doubled down again in early 2023. 2024 saw further continued […]

LikeLike