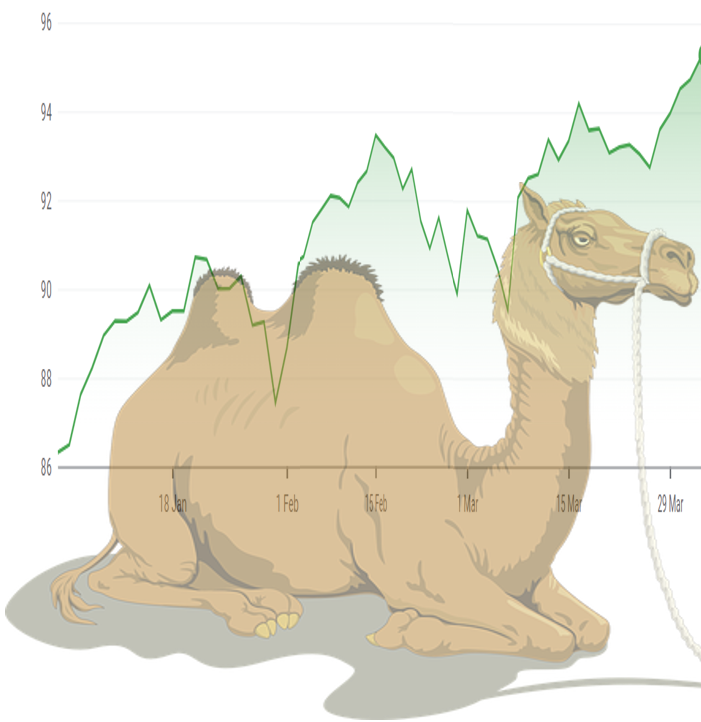

My portfolio went up over 3% in January. But then came down again.

The same happened in February. I concluded the month feeling somewhat ‘humped’ by the market, twice. Hence my post about two-humped camels (Bactrian camels, as it turns out – ahem).

So as the end of March approached, with my portfolio again up about 3%, I kept expecting a correction. But as at the time of writing, no correction has yet occurred.

Meanwhile, the news in March seemed full of vaccines. The UK has now vaccinated over half its adults. The US, about a quarter. The EU, is bringing up the rear, with about half of that. The headlines were full of vaccine wars, blood clots, second doses, you name it.

The other key story in London was the horrible news about 30-something Sarah Everard who was abducted and killed on one of the popular green spaces, Clapham Common, by a stranger – a policeman no less. The story hit the headlines because of how rare this sort of stuff is these days. There are only around 20 women killed in the UK every year by strangers, which suggests 5 or fewer per year in London.

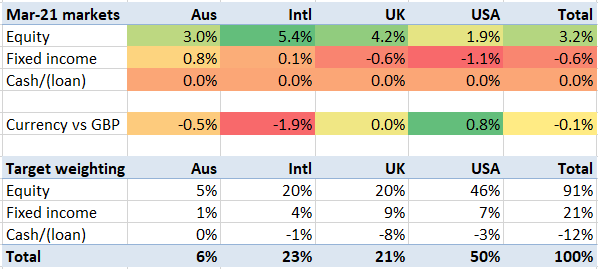

In terms of the markets, how different March 2021 was from March 2020. In March 2020, US/Australian equity markets dropped 20%. One year on, equities rose over 3% in the month. The USD gained a little versus the EURo. Otherwise, not a lot to report.

Regular readers will know that I run my portfolio on a slightly indebted basis, via a margin loan – with my target leverage being ‘-12%’ – i.e. for £112k of investments, I have £12k of borrowings, leaving me with a net worth of £100k.

I made a tiny tweak to my target allocation, near the end of March. This is because part of my approach here is having the psychological comfort of knowing that if I leave the portfolio on autopilot the dividend income alone will pay off the debt automatically. Yet with my recent portfolio simplification, I now have very few holdings that pay out EUR income – and those that I have are mostly not in the brokerage account that has the EUR margin loan. Most of my borrowings are in my domestic currency, GBP, where my leverage level is much higher than -12%; it is -8/29% (i.e. 28%), a level that UK dividends themselves are going to take a long time to repay. But plenty of my non-UK exposure is held in GBP-denominated securities, like Vanguard/iShares’ ETFs, which pay out dividends in GBP, so in practice I think I am within about 4 years of autopilot payback.

Before my tweak, the target borrowing of £12k would, ideally, be £8k of GBP borrowings, £2k of EUR borrowings, and £2k of USD borrowings. I have tweaked this slightly to shift the target slightly from EUR to USD, because my actual EUR-denominated holdings are now so low, so I receive very little EUR income, and I have far more USD holdings – admittedly including a lot of tech stocks that don’t pay dividends. So now my target borrowing, while remaining at -12%, is -1:-8:-3 EUR:GBP:USD.

With markets moving up almost 3%, my portfolio delivered a very similar result – in fact it was up 3.2% in the month. That marks the first concrete progress in the year so far, after the ‘camel back’ January and February.

We’re a few days away from my annual ISA topup, right at the start of the tax year. I’m going to take the opportunity of the new tax year to realise some more capital gains and rationalise the portfolio a bit further. In the meantime, my complexity/similar remains at about the same level as last month.

As we enter the UK’s next tax year, I remain modestly tactically overweight on cash (/underweight on my margin loan) and very mildly underweight on equities.

Ha! I had called it the curse of the Loch Ness Monster, the cartoon hooped-back version, for my Future Fund progress during Jan and Feb. Like you, I know I shouldn’t be getting concerned over the monthly gyrations of the markets but I can’t help peeking every day. Glad I’m not the only one seeing creatures, real or mythical, in the stock market charts!

LikeLiked by 1 person

Thanks for the insight and for your other posts. They’re highly informative reading.

I noticed you utilise margin loan as part of your positioning and wonder if you might be able to comment on taking margin loan from a private bank vs. broker (i.e. Interactive Brokers). On the surface, private banks seem a little more expensive (margin, custody charge, transaction costs) although provide more flexibility (LTV, personal services, etc)?. My investments are mainly in UK based funds and investment trusts. Many thanks!

LikeLiked by 1 person

Well, check out some of my previous posts to give you a feel:

* https://firevlondon.com/2016/12/07/injuring-private-bankers-wealth/

* https://firevlondon.com/2018/01/07/two-years-of-the-margin-loan/

* https://firevlondon.com/2018/08/13/recalibrating-my-portfolio/

LikeLike

I find the opposite for margin loans. IBKR margin rates tend to floor at around be at best around 5/8 of a percent over over Fed funds (so say 0.75% currently) and can be even higher for small amounts. A $1mm loan costs about 1.125% on a blended basis. Even $5mm costs 0.825%. By comparison my PB charges 3/8 of a percent flat on any amount (so 0.50% currently). That does depend on the quality of the underlying collateral for portfolio VaR margining. I use higher quality/lower vol hedge funds, rather than say high-vol equity index funds to achieve a lower rate.

I find you want to use a PB is to take advantage of their transactional capabilities (much tighter bid/offer in FX, bonds, equities; better derivative execution, lower funding costs) whilst not allowing them to manage my portfolio on a discretionary basis (as much due to their terrible asset allocation as the fees). The issue is they do want recurring income coming from somewhere. So I let them takes fee for holding my offshore bond. That gives them around 40-45bp of zero risk income. I consider the 5bp they charge for being custodian very cheap. I much prefer their “fortress balance” sheet at 5bp to say paying a European bank 3bp. I wouldn’t touch the IBs of this world for that role.

LikeLike

Thanks for your input ZXSpectrum48k. Sounds like your PB is giving you a much better deal. I’m talking to a well know British bank with a blue eagle on its logo, and they’re charging for 165-200bps over BoE base (depending on collateral/diversification). They also charge 15bps as custodian fee on collateral held with them. Agree discretionary managed portfolios are expensive, and I would look to utilise their execution only services.

The problem I have with them however is that they want 0.5% transaction charge for trading funds/IT/equities, which in my view is very expensive considering that you can trade these next to nothing on DIY platforms. Although this bank also offer cheap execution only platform, trades on that platform cannot be used as collateral for lending.

Could it be size as I’m only looking to post £500k as collateral, or am I talking to the wrong PB?

LikeLike

Ok that is what I paid my well known PB too, of a similar spec. Originally over 1m loan, now down to barely six figures for this reason.

LikeLike

ZX48k – i like the sound of your private bank! I assume you have more with them than I have with mine. Tho I have similar amount with IB to my PB. Why wouldn’t you touch IB, do tell?

LikeLike

Once the camel’s nose

is in the tent, the brute

is soon to follow

LikeLike

FvL. For some reason can’t reply to your embedded comment above. I have nothing against IB and use them to some degree. I just wouldn’t hold large amounts of capital with them. They are a retail broker, not a very large global custodial bank. Chalk and cheese. I just like holding my largest sums with players who have a strong balance sheet, track record of prudent risk management and (especially important) access to the Fed funding window! People tend to forget that 2008 was not a banking crisis, it was a ‘shadow banking’ crisis. Lehman wasn’t a bank. Nor was AIG, Fannie Mae or Freddie Mac. Most financial crises always stem from the shadow sector. It’s agents, broker-dealers, funds etc that tend to trigger the issues, not money-centre banks.

LikeLike

Another question regarding IBKR. One thing that has put me off is that they are in the USA. Last time I checked how it works, even UK customers need to go through the USA’s process in the event of death. Aside from the bureaucracy involved, it means your non-USA personal tax status exposes you too US estate tax on US securities above $60,000:

https://www.irs.gov/individuals/international-taxpayers/some-nonresidents-with-us-assets-must-file-estate-tax-returns

Non-US domiciled securities (e.g. ETFs in Ireland or Luxembourg) seem to be exempt. Maybe that’s the solution.

I was curious if any of you have investigated this in detail?

LikeLike

Stefan – I have not investigated in detail. I believe my relationship is with their UK firm – and my funds are all wired in through UK banks (citibank/etc) – so I would be very surprised to get caught up in USA inheritance. They have a very UK compliant setup, albeit without support for ISAs.

LikeLike

“Interactive Brokers (UK) Limited acts as an arranger for Interactive Brokers LLC. Interactive Brokers LLC holds clients funds and assets.”

https://ibkr.info/article/956

https://www.bogleheads.org/wiki/Non-US_investor%27s_guide_to_navigating_US_tax_traps

LikeLike

I found the document that explains the relationship between IBKR’s UK and USA entities in more detail. It confirms that the USA entity holds funds and assets:

https://gdcdyn.interactivebrokers.com/Universal/servlet/Registration_v2.formSampleView?formdb=3207

I do eventually expect to open an IBKR account and this is why I’m interested in understanding the associated tax consequences and risks. It seems if you hold non-US domiciled assets and don’t leave a large amount of cash deposited then it’s okay.

Worst case your IBKR holdings need to go through the USA probate process in the case of your death, I’m not sure.

Similarly, if IBKR LLC were to go bust in the USA, I wouldn’t count on IBKR UK ensuring that you get back your holdings. The agreement linked above explicitly mentions that the USA entity may not follow UK practices in segregating client funds and assets. You may need to make your claim in the USA.

Would be interested if anyone has experience of how exactly these things work…

LikeLike

Well well. That’s a reasonably scary edge case to consider. Thanks for highlighting! I wonder whether the US/Swiss private banks like GS/UBS/JPM face the same issues?

LikeLike

I read these comments with interest, I’ve always dismissed our PB (Coutts) (are they even a real PB any more?…) as being a ludicrously expensive option for anything and everything, which has meant we have far too much of our equity-based NW linked to IB (with a similar 10ish% margin loan as you have FvL). Maybe I should reconsider…

I’ve always adopted a low cost/simple approach but am starting to wonder the NW level at which it still retains relevancy, we literally chuck ISAs to iWeb, SIPP money to AJB, GIA funds to the IB margin accounts and then bank with the bank, who I’m sure will ditch us eventually because they don’t make enough money from us. It feels like ‘Cheapskate HNW’, but maybe it’s just sensible?…

Aside from the inability to fund a GIA at lower NW levels I’ve always considered that this strategy would be my method for a NW anywhere from £0 to £XXm. I wonder what the trigger point is for exploring something more exotic, expensive and hard work, but potentially less ‘risky’ and more ‘appropriate…

LikeLiked by 1 person