What an amazing twelve months it has been. And what an amazing month March 2020 was.

March 2020 saw global equities down 25% on peak, just a few weeks earlier. VWRL dropped to £57, a level it hadn’t been at since 2016. That left my ISAs feeling very down in the dumps.

Since March 2020, VWRL has climbed to £83, almost 14% above its previous cycle’s peak. My ISAs are looking very plump indeed.

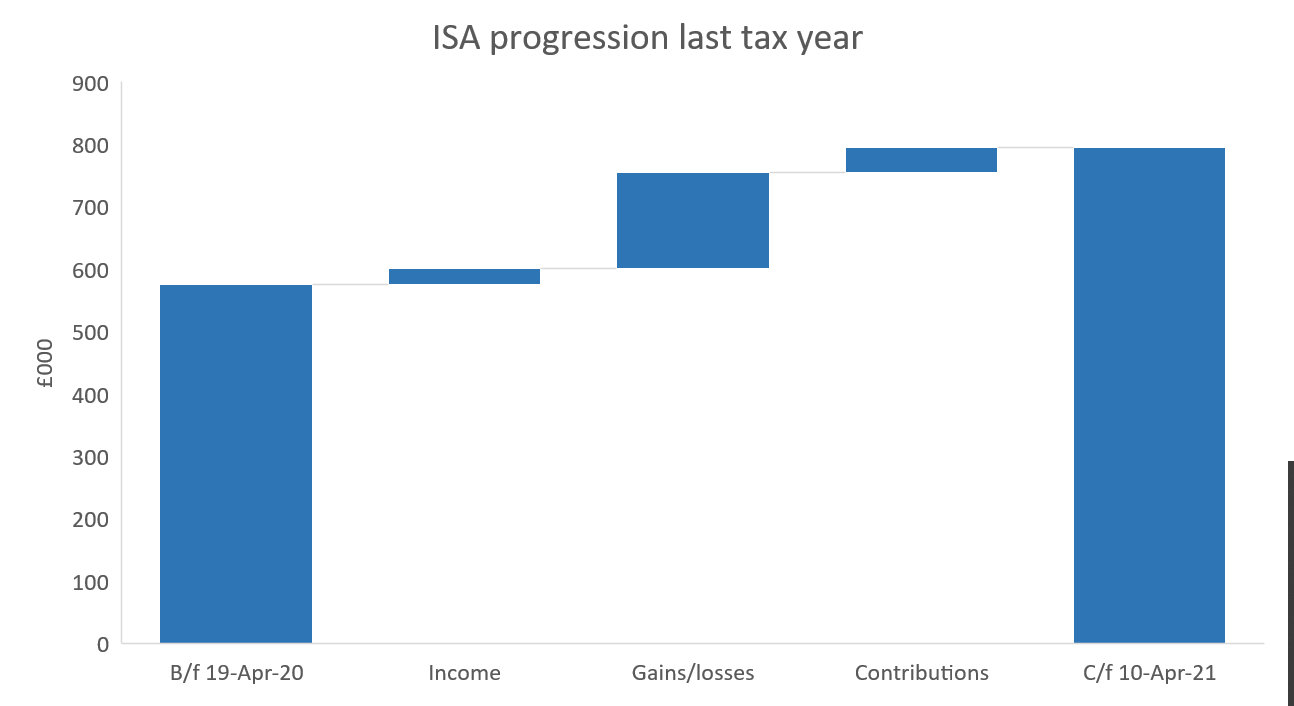

ISAs grow in three ways.

- The existing ISA investments generate income. In my case the income over the last tax year – just over £24k – was almost identical to the preceding year. All such income, in an ISA, is tax free.

- The existing ISA investments grow/(fall) in value. The preceding year, mine fell by over £50k. But last year they roared upwards – increasing by over £150k. Any capital gains that I realise in an ISA are tax free.

- We top up /(withdraw from) the ISA accounts. I top up to the max – both my ISA and Mrs FvL’s ISA – i.e. the pot increases by £40k each year (out of other savings or taxed income). Until recently, this was the biggest source of growth of my ISA pots. But with the market’s rapid climbs since March 2020, now my ISA is growing by itself more than I can top it up. I think this is the first time that has happened. In the future this should become the norm.

Only six years ago, my total ISA pots amounted to ‘only’ £330k. They have much more than doubled since then, to £795k. The £millionaire status is in sight. But already my ISA pots are worth more than USD$1m.

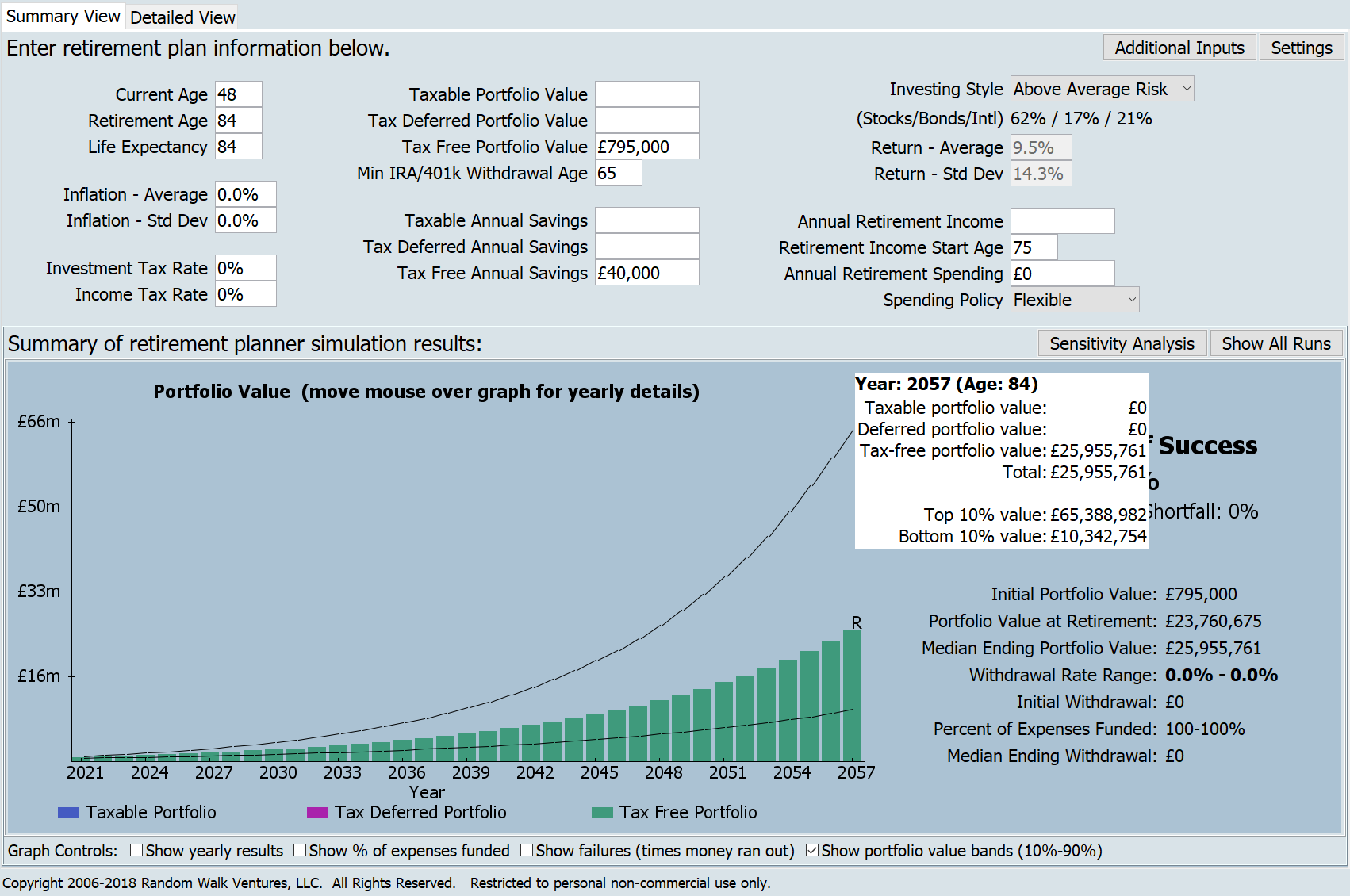

The Flexible Retirement Planner now suggests the median outcome when I pop my clogs (aged 84, apparently) is £26m (up from £21.3m, last year), in today’s money (simplistically – by setting inflation to 0%). There is a 10% chance my ISA ends up worth more than £65m. This lot assumes my average return is 9.5%, with no inflation; in the real world I have been obtaining over 11% over 8 years, but inflation has been 1-3%, and my 11% figure is probably unsustainable, as this period hasn’t included a sustained market crash.

As I say every year, I don’t expect the ISA tax break to remain unchanged until I am 84. But while it and I last, it is fast becoming the single biggest tax break I benefit from.

Congratulations, that represents dedication to the ISA cause!

It has been a crazy year for sure. If you measure returns over the last financial year the returns have been spectacular (just don’t go an extra month further back 😉

My best unitised return was son no. 1 JISA at just over 40%

Overall I was at about 24%, best FY ever (since I unitised everything in 2014), but prev FY was -9%

Next best was FY ending 2017 at 19%

LikeLike

Yes, my 1 year (actually to 1 April 2020) return is +31.5% according to my live daily-returns page.

Best calendar year was 2016 at +24%, tho 2019 was not far behind at +23%.

LikeLike

Nice one, what’s your view on the outlook for markets?

LikeLike

In general I don’t have much of an outlook on markets – as set out in my Investment Policy https://firevlondon.com/my-investment-policy-statement/ .

Tech drives a lot of the market – I think valuations of 2nd tier tech are rather crazy, but top tier tech (google, amzn, fb, msft) not so much, and they are big. If interest rates rise everything would change, but policymakers have massive incentives to keep rates low, and inflation remains largely hypothetical (except for Brexity UK). Keep hanging on in there, rebalancing will look after you.

LikeLike

As I said in a recent Monevator article, a 70/30 portfolio of S&P/long-dated Gilts would turn the total S&S subscriptions of £246k (from 1999/00) into around £738k now. A 100% S&P portfolio would be £849k.

The balanced portfolio needs an extra 2.7%/annum, the 100% S&P portfolio 1.5%, to have got you over the £1mm line. So ISA £ millionaires are becoming far more common. Then again, £1million used to be “wealth” but now it’s just a vague feeling of comfort (and in London not even that).

The main issue I have with S&S ISAs is how restrictive they are. That’s not a problem when the amounts are small, but when you get into seven figures you want more flexibility. I want my best funds in my ISA, not second rate ones, yet a requirement for an archaic attribute of “reporting status” excludes them. Plus, no derivatives or options, no efficient way to trade FX without paying huge fees to rubbish brokers.

Yet, via the Innovative Finance ISA, we’ve been allowing retail investors to invest into speculative property development loans at 12% on some dubious P2P platform or buy toxic private equity via Crowdcube. The IF ISA is very well named: it’s very iffy

LikeLiked by 1 person

[…] The graph below shows the bridge over the course of the tax year. As mentioned above, since the start of this tax year my portfolio has dropped significantly in value – by around £100k. But, despite the fall in the strength of the pound, my ISA has retained the USD value of around $1m. […]

LikeLike

[…] Regular readers will know that I never withdraw funds from my tax-free accounts. In the case of my pensions, that is because I am legally unable to until I hit retirement age, and in the case of my ISAs I see the tax advantage as so strong I will do everything I can do leave the investments in those accounts free to compound up indefinitely (and reasonably successfully). […]

LikeLike