It’s that time of year again. The start of the new UK tax year (for ancient reasons, UK tax years begin on 6 April). My favourite time in the financial calendar.

It’s time to top up the annual ISA. ISAs are the tax-free savings accounts we are – unusually in the world – blessed with in the UK. While the funds we put into an ISA are net of tax, with no pension-like tax relief when we save, all subsequent returns are tax free. Forever. If you are fortunate enough to have £20k lying around, and you move it into an ISA…. by the time it has doubled, say, four times (which it probably will, if you invest in low-cost equity trackers and live long enough) it may well be producing £20k a year of tax-free income. If you can do this enough times, when you are young, your ISA will knock your pension into a cocked hat.

There are no upper limits on how much you can have in your ISA pots, unlike pensions. Hence, one of my ambitions is to (live long enough to) build an ISA pot worth potentially $100m.

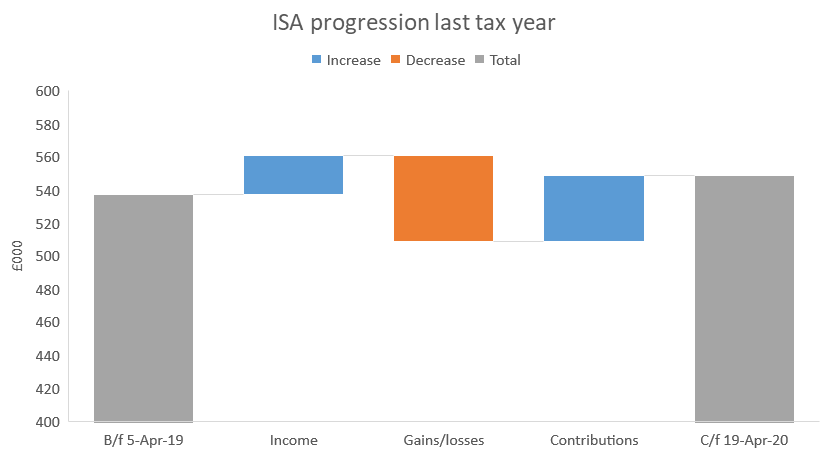

However, with markets melting down over the last two months, it is definitely a case of two steps forward, one step backwards. Nonetheless, my ISA’s income is £24k – up about 10% on last year – so our (two) ISAs are generating more than one of us can top up every year.

For the last few years I’ve been using the Flexible Retirement Planner to project where my ISA might end up, if I live to a statistically average age. Apparently HMG now expects me to live to 84, which is a year younger than they thought last year – and four years younger than they predicted a couple of years ago. Odd.

My planning tool now suggests the median outcome when I pop my clogs is £21.3m. That’s 20% lower than last year. One fewer year and a diminution of value over the last twelve months are both impacting this long range forecast. But there is still a >10% chance my ISA ends up worth more than £50m.

I continue to think these tax breaks can’t last forever. But this Tory government just (in March) bumped the Junior ISA allowance from £4k per year to £9k per year. A well off family with 3 kids can increase their family’s tax free pot by £67k per year. This March increase, admittedly before Covid-19 had properly hit, suggests this is not the government to be tightening the wealthy’s ISA tax breaks. Hooray, for me! And bad luck, other taxpayers – you’ll have to fund all this Covid-19 relief a bit more.

Presumably ar some point you will need to take an income, try running some scenarios on what it would be worth once you do that

LikeLike

@Gareth – I’m hoping my non-ISA funds can provide sufficient income. I’d rather take income out of fully taxable funds, than raid an ISA. So, touch wood, my ISAs can just carry on compounding up unmolested.

LikeLike

Probably worth a mention, if you’re under 40 there’s also the option of using the Lifetime ISA which the Government will (currently) very kindly top up with £1K each year when you put in £4K. However there are restrictions on when/how it can be withdrawn.

LikeLike

Can I ask what expected return is used to aim for an ISA pot of $100m? I have been projecting 5% after inflation and even if you made contributions for 50 years you would only end up with £4.5m! Actually just noticed the image shows 9.5% return in the calculator, with 0% inflation… is that realistic? FIRE just got a lot more interesting if so!

LikeLike

Jamers – good Q. Screenshot shows the returns assumed yes. 9.5% is the number this projection uses. I am assuming all numbers are *after* inflation, i.e. in today’s money. See last year’s post for some good comments pointing out the flaws in that assumption. It is punchy yes but my >7 year compound return is around that. 5% after inflation sounds more realistic though I agree!

LikeLike

I continue to be amazed that the gov allow a £20k ISA allowance each year, especially when you consider that the average wage is only £30k or so (ok, so London is probably higher- but so is property). This basically only allows the rich to make use of the full amount. I can imagine some pretty awful Daily Mail headlines in a few more years- with them telling everybody how certain people “dodged” tax etc. All entirely legally- and I’m sure more would make use of this allowance if they could. Just feels all a little mis-matched. If that makes any sense.

LikeLike

I agree with you – as you can see if you read more of my ISA-related blogs. I am very fortunate the allowance is so high but I don’t know too many people who can avail themselves of it in full year after year. They are only a complete no-brainer if your pension is going to hit the lifetime limit, which reduces the pool of eligible folks even further.

LikeLike

Nice one. We max out our ISAs every year (being tapered down to £4k in my pension leaves me with no other choice) but I am, however, reluctant to make use of the Junior ISA.

As much as I love my kids and would like to think they’ll continue following my advice, giving them effective control of so much money at the wise age of 18 just seems dangerous.

LikeLiked by 1 person

@Damian – Re children’s ISA

I’m funding a daughter’s LISA so help fund a house deposit (I’m selling her a house, hopefully). The 25% top up and restricted use seem ideal/generous.

B

LikeLike

@Boltt

I think that’s a better way to do it indeed. The challenge is that you need to wait for them to turn 18 to start but it sure solves the issues around control / use of proceeds.

LikeLike

You can put £20K per year into a cash ISA at age of 16, then later transfer the money over to Stocks and Shares ISA at 18. So two years tax free – in additon to the JISA allowance, so £29,000 per year for the two tax years after child turns 16. Then after 18 the usual £4000 Lifetime ISA and another £16,000 S&S. Also free of inheritance tax as long as you survive. Would be a shame to lose those tax breaks (if you can afford to use them obviously) at a time your kids wouldn’t be able to and hence would lose them for good.

LikeLiked by 1 person

Interesting read, but not sure I’d want need £1m in an ISA nevermind more. If it floats your boat, but isn’t the point of Fire so you can RE and spend some of those savings?

I think pensions better than ISA for average income person cause of tax relief.

My investments are only up this 12 months cause of tax relief, in solely an ISA would be down.

LikeLike

[…] March 2020 saw global equities down 25% on peak, just a few weeks earlier. VWRL dropped to £57, a level it hadn’t been at since 2016. That left my ISAs feeling very down in the dumps. […]

LikeLike