It’s been a much calmer month in the markets.

Of course it’s been the month that the UK’s Prime Minister went to hospital, with a “50:50” chance of making it out alive.

Lockdown has been the word on everybody’s lips. I spent the entire month working (hard! Even a bit over the long Easter weekend) from home. And, while the UK extended its lockdown from 3 weeks to 6, by the end of the month the lockdown mood music from across Europe and beyond had noticeably improved.

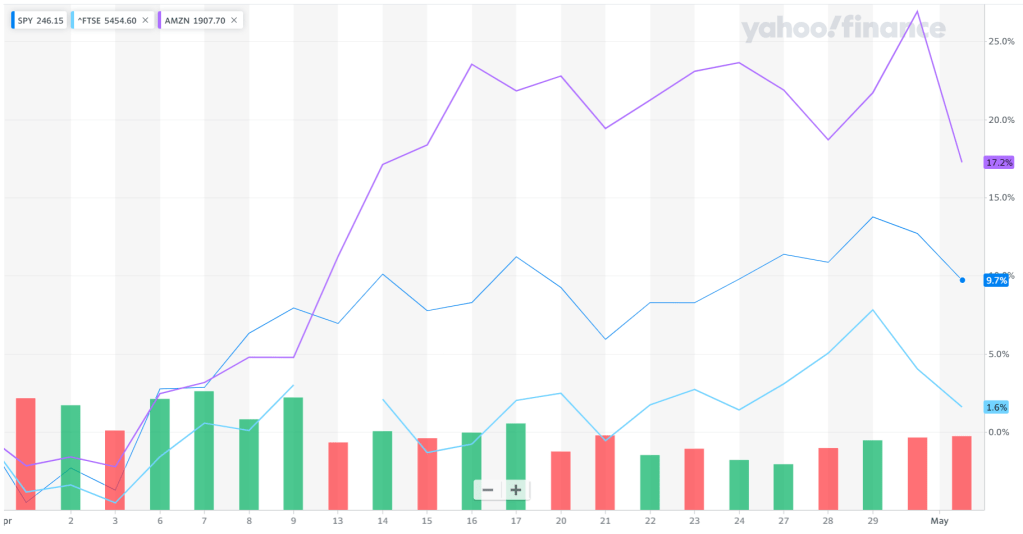

Markets up almost 10%

And, my, how the market’s mood had improved. The US, the S&P rose from 2462 on 1 April to 2923 on 29 April, a rise of 19%. In a month. If you had the courage to burn dry powder on US equities in late March you could have seen over 20% gains since. My (slightly leveraged) “US tech” equity subportfolio rose about 25% – led by Amazon breaking to new highs above $2400.

US equities were in fact the standout winner, up 13% in the month, while other equity markets rose 4-6%. In part, this reflects ‘big tech’ (which account for >10% of the US market). Bonds had a pretty good month too, aside from in Oz – where the currency recovered 4%.

What’s going on : is it QE?

I have been finding the market hard to fathom.

It feels like the chances of a quick, temporary disruption before we all spring back to normal (as suggested by Larry Summers, who likened lockdown to Sundays and returning to work to Mondays) have faded, but I think also the chance of 2 years of lockdown have receded too.

What is reasonably clear is that there is going to be fundamental damage to large sectors, such as energy, aviation, travel, and parts of the leisure industry.

It looks more likely than ever that the ‘too big to fail’ banks are going to take quite a hit, though as yet there is still no talk of any liquidity problems.

Thanks to the above, FTSE remains firmly down, still below 6000, having touched 7500 early in the year.

It is also obvious that ‘big tech’ should do OK out of this, although this felt reasonably obvious in March, which fails to explain the 20% post-March hike in Amazon’s stock price.

And, big though tech is in the US stock market, and much as several US states seem to prefer Medicare bearing the brunt of covid rather than the economy as a whole, I don’t think the S&P should be worth as much as it was worth less than 12 months ago, and up 6% over 2 years.

My portfolio is back where it was less than 12 months ago. Why have markets recovered so much of their losses, even when lockdown continues?

Part of the answer clearly likes in the Fed, which has intervened to buy assets – printing money which is clearly filtering through to equities.

Part of the answer presumably lies in Donald Trump Sr who, with an election now only six months away, is frantic for good news on the stock market and the economy and, I imagine, is finding innumerable ways to influence short term movements in his favour.

Part of the answer lies in the drop in base rates, which effectively makes even lower income streams more valuable.

But part of the answer may be that Mr Market is calling it wrong.

Could the market be wrong?

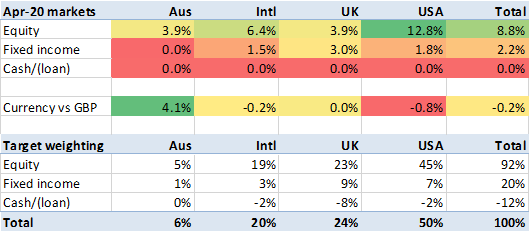

Far be it from me to time the market, but having 92% of my portfolio’s net worth in equities right now makes me less comfortable than I would normally be. And so, I’ve deliberately been running a slight ‘tactical underweight’ on equities. I say slight, because my equities exposure is only 3.4% below target – i.e. at about 88% of my portfolio net value – approximately evenly down across geographies.

I normally regard a delta of more than 1% as something to be corrected. My deltas now include a 1.2%, 1.4% and a 2.8% (as I am overweight in home country cash). This is very deliberate. While I can hear a Market Timing gremlin on my shoulder, it gives me a margin of safety that makes me feel calmer.

I have the lowest level of margin loan that I’ve had since splurging on the Dream Home in January 2016 – running about 25% lower than my normal target allocation would suggest. If the market returns to ‘fear mode’ I have some buying power, and my leverage is mild (almost at the level of some popular Investment Trusts). And if equity markets resumes their incomprehensible surge, my 88% exposure to them should see me good.

It does feel a bit too optimistic, and tech, in particular, seems to be invincible.

Let’s see if Friday’s 3% wobble presages anything more significant. If there’s one thing I learned over the years it’s that betting against the governments is a bad strategy.

LikeLiked by 1 person

All of the market timers who sold at the bottom expecting a further decline will be shaking in their boots right now; this may just be the greatest lesson in “You can’t time the market,” of all time.

As you said, it does seem strange to have rebounded so much, but who knows 😕

LikeLiked by 1 person

The markets are always right though….. right? Until they aren’t. I think with all the “fake” supports that’s coming from government is giving the markets support that they wouldn’t normally have. Hence, what I think, is why we are seeing bizarre increases that really shouldn’t be there. What happens if/when the government(s) step back? Will they ever be able to do so…..

LikeLike

Yes Amazon and big tech are the winners. Personally we’ve bought more items than usual from Amazon and using technology more at home, so it makes sense they’d go up, if everyone is doing the same. And the markets are looking ahead and saying this is only getting better for them.

LikeLiked by 1 person

[…] Firevlondon reviews a bumper month (34) […]

LikeLike

Hi greatt reading your post

LikeLike