This post is late.

More than six months late.

The UK’s tax-free savings accounts (ISAs) operate on an annual cycle. Each tax year, starting 6 April, a UK tax payer gets another £20k annual allowance. ISAs are the tax wrappers that administer this allowance. Any account in an ISA wrapper sees all its gains and income become tax free – not even disclosable on a tax return. You can put most type of investment into ISA accounts, certainly including UK/US/EU listed securities. That makes a “stocks & shares” ISA account the number one fundamental of UK taxpayers’ investing, aside from (in some cases) a pension.

£20k might not sound like that much, but if you have £20k to play with as a 20 year old, and you invest it in equities under an ISA, and always reinvest returns, you can expect your investment to appreciate very significantly. At 7% average return it will double every ten years. So by the age of 60, four doubles later, that original sum would be worth £320k (before taking into account inflation). Now imagine that at age 21 you have a fresh £20k to play with. And at age 22. And so on.

I only realised how imperative ISAs were about 15 years ago. But since then I have made topping up my ISA accounts for both myself and Mrs FvL an annual imperative. I try to do this as early in the tax year as I can – in fact I usually start hoarding cash a few months before the start of the tax year in April. And I typically publish a blog post when I achieve it. This tax year, this is that blog post. It has taken me until December to scrape up the £40k readies.

ISAs grow in three ways.

- The existing ISA investments generate income. And in tax year 2021-22, my income was up 50% – to £38k. This is almost exactly the same as the maximum amount of fresh funds I can contribute every year.

- The existing ISA investments grow/(fall) in value. In the 12 months to April 2022, my portfolio grew only about 1%. I don’t explicitly track the asset allocation of my ISAs, but it is a bit more income-orientated and a bit less USA/tech orientated than my wider portfolio. It is also unleveraged, but that hasn’t stopped it dropping significantly since April 22 – by over 10% in fact.

- We top up /(withdraw from) the ISA accounts. I always aim to top up to the max – both my ISA and Mrs FvL’s ISA – by the £40k allowed under ISA rules. This year, due to a variety of other calls on my cash, this has taken me 8 months – far longer than normal. In the meantime the portfolio itself has been generating almost as much income as my topups – all of which has been reinvested.

The graph below shows the bridge over the course of the tax year. As mentioned above, since the start of this tax year my portfolio has dropped significantly in value – by around £100k. But, despite the fall in the strength of the pound, my ISA has retained the USD value of around $1m.

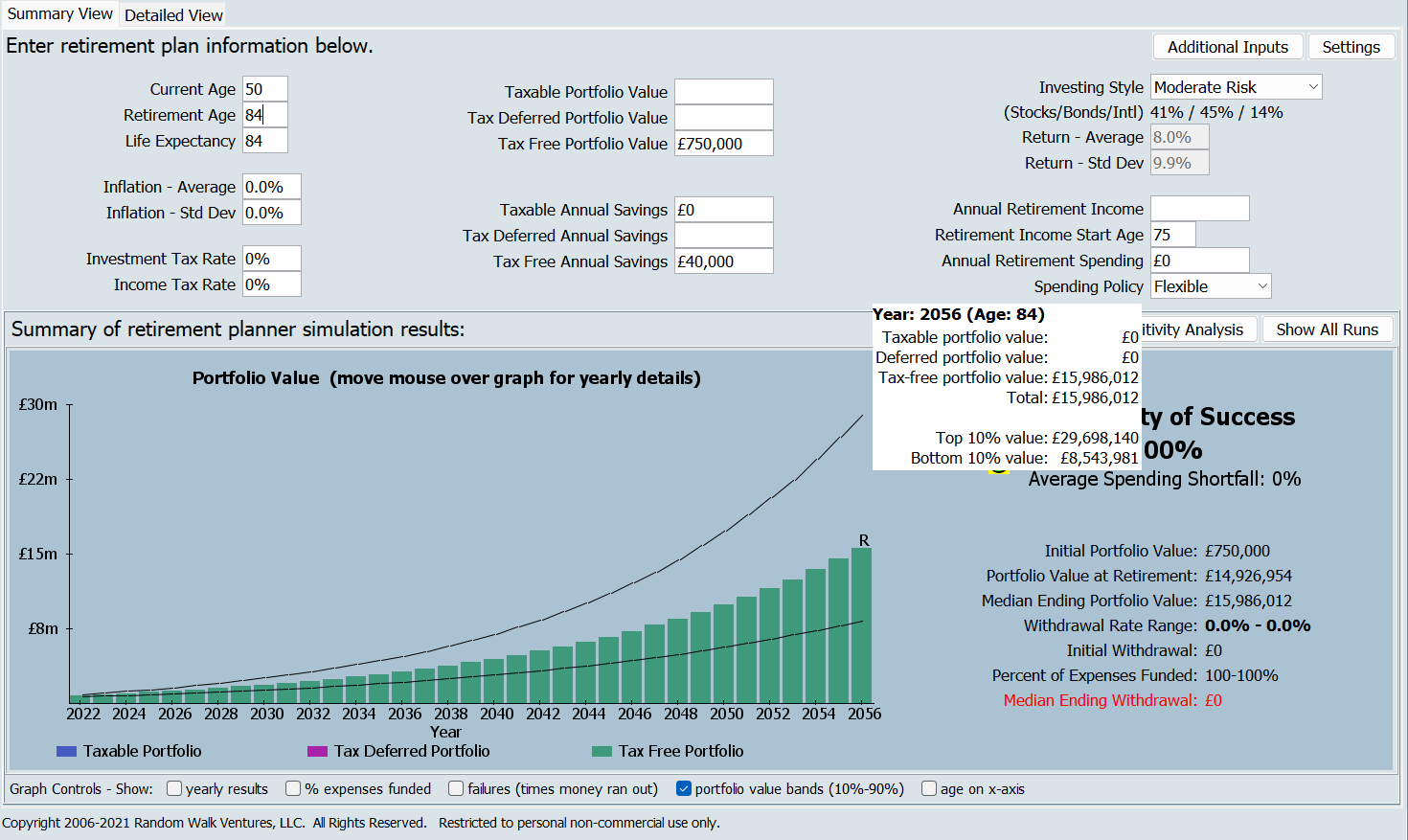

Back in April 2021, the Flexible Retirement Planner was suggesting the median outcome when I pop my clogs (aged 84, apparently) would be £26m, in today’s money (simplistically – by setting inflation to 0%). It showed a 10% chance my ISA ends up worth more than £65m. This was assuming my average return was 9.5%, with no inflation, which back in early 2021 was comparable to my portfolio’s returns over the previous 8 years.

If you roll the clock forward 12 months from my last analysis to April 2022, my future in 2057 looked similar, albeit a million or two smaller.

However, looking at the world now in December 2022, things have deteriorated significantly. The main hit is that my long term returns are now around 8%, down from 11%, suggesting ‘moderate risk’ is a better returns framework than ‘above average risk’ as defined by this planning software. I’m also two (rounded) years closer to the clog-popping moment. And, as mentioned, my ISA portfolio is now down around £100k from April. This combination of factors leaves my median 2057 number at £16m – down 40% from the last prediction. My 10%-chance upside total for my ISA deathbed is £30m, less than half the previous £65m.

Heavens – the real world intrudes and progresses for a few months and it wipes millions of pounds off my long term assets, and half my future. All of which shows

- how hard making long term predictions about your portfolio is,

- why making steady investments over time instead of only one large initial investment is a wiser strategy and

- how remarkably generous the UK’s tax regime for wealthy savers remains

point 2. is debatable I suppose. Evidence being, on average, you are better off investing as a lump sum rather than DCAing over future points in time – and that’s obviously on the assumption you have the money to do so, i.e. a windfall of some sort. For every other use case its moot as the only possible thing to do is invest steadily over time as that is the manner in which money comes into our lives.

Good point about the crazy variability in long-term predictions, and the implicit danger in anchoring to those numbers because of that..

Despite the forecasts, I still think you’ll do alright 😉

Happy Christmas to all the FvLs

LikeLiked by 1 person

Yes I hear you re point 2 (one off vs time cost averaging). Tho I think most textbooks would regard ‘put it all to work within six months’ as a one time activity, whereas I would regard that as about 2x as long as my normal time cost averaging timeframe 😉

LikeLike

Great job on the £800k In your ISA, agree it’s too good to believe in some ways £40k pa per couple and never paid taxes again (and no ceiling yet!)

I’m early 50’s with ~ £500k in ISA. My plan is to get to £1m over the next 5-7 years and then start taking the income/gains tax free (probably maintain the £1m nominally)

Have you given any thought to when you’ll start to withdraw income or capital? The “tax-free”ness of the ISA is slightly addictive and it’d be too “easy” to keep filling it at the expense of enjoying it.

I love my kids but I want to enjoy it rather that gift them too much in 25 years. If I (we) die with £5m in the ISA then I’ve failed in some ways – working too long, spending too little, not sharing enough etc

LikeLiked by 1 person

Boltt – at the moment I intend never to withdraw, but to leave the thing to some worthy cause. This is however because I have greater funds available outside the ISA than inside the ISA, and (touch wood) I won’t run out of funds in the unsheltered pot, so won’t need to raid the ISA.

This being said, I Garee with you that I’d rather spend/enjoy/max opportunities than have any regrets on my deathbed. To that end, my cost of living is increasing even faster than inflation – I am enjoying rather a lot these days!

Watch this space, in a few years’ time.

LikeLike

The problem with ISAs is that funds need to have reporting status to be eligible. That tends to exclude pretty much all the decent hedges for an inflationary bust type scenario (i.e. 2022). So you can’t really expect your ISA to do well.

We have four ISAs, two seven figure ones for us parents and two six figures for the kids. All were chock full of equity trackers. They only made a small positive return in USD terms this year for two reasons. First, the large slug of Brevan Howard IT, where not only did the fund perform incredibly well but it also went to a 20% premium. Second, that I sold some of that BHMG to buy some linker funds post the mini-budget debacle (and then sold most of that back a week later to go to cash). So without trading returns (and tbh Brevan is just a trading shop), it would have been miserable.

End of the day though ISAs (and even SIPPs) are not constructed with people like us in mind. Most ISA money over the last decade went into cash ISAs with rates are zero. Explain that. We need to use more scaleable (and preferably offshore) vehicles by which to invest. The ISAs just become part of the kids’ inheritance, never to be touched.

LikeLiked by 1 person

Love your blog and how you describe in detail your thought process for all your investments. If I may provide a word of advice from my experience…

I fat”FIRE”-ed in 2015, 8 years ago and have been investing since 2005. I’ve made every mistake in the book in the past 18 years and went through all the ‘entrepreneur to investor’ transition: stock picking, leverage, quant factor investing, stops, CTAs, managed accounts, private banking structured products, hedge funds.

A few years ago, a much older and much wealthier friend (no, not Warren!) who has investing bogle style, asked me for my USD returns after fees in various times and we had compared. I was shocked and humbled. After some thoughts and researched I finally gave in and have simplified my portfolio to a few broad ETF positions. I run my portfolio like a close-end endowment with the purpose of maintaining it inflation adjusted over a very long period (30y+) and withdrawing ~3% per year.

I took a look at a globally diversified total return 80% equity / 20% bond passive portfolio and compared. That’s how benchmarking should be done, with a diversified portfolio that matches the equity exposure in the investor’s actual portfolio, not S&P500 price returns or other benchmarks “hacks” that some fund managers use to show ‘outperformance’. Benchmark choice is crucial.

£10M in 2013 (~$15.8M) grew to £27M ($32.5M) after fees in 10y with the £7M being the fx bonus. That’s 10.44% annualized. Using the original fx rate from 2013, it would be £20M, 7.2%, slightly under your actual performance.

I think the various tinkerings are a right of passage for many investors. Some never make it through, and some outliers end up beating the market either on a total return measure or on a risk adjusted basis (with lower ‘risk’). Some keep the tinkers to a small % just to do something but how much value is really added from the tinkering and 150+ position diversification? In reality one good or bad macro FX guess can wipe all the edge or luck out.

We are all better than average investors and better than average drivers…

LikeLiked by 1 person

Very helpful comment – thank you. I think you are in a very small subset of readers who would feel they know their 10 year annualised returns.

My portfolio is a lot simpler than it used to be – check out my ‘complexity’ posts – but continues to contain 60+ holdings and remains somewhat overweight towards big tech. Right now I have other priorities before fixing this – namely to reduce the absolute size of my margin loan.

Right now I am spending more than 3% of my invested portfolio. On that measure I can’t Fat-FIRE retire quite yet. Though on other measures I should be more than fine to do so, and in the meantime I receive some material income that I am using to bolster the balance sheet.

Watch out for a fuller review of the last 10 years before long.

LikeLike

I feel the 3y, 5y, 10y benchmarks against passive portfolios with similar equity allocations are critical to self-evaluate and especially evaluate money managers (after fees!). They are eye opening but tough to do kinda like stepping on the scale 🙂 I would not trust a private fund, bank or money manager that does not provide this. I used to use a well known large private bank, and they went to great lengths to make it uncomfortable to find my long term portfolio returns and fees.

I like tilts, as long as they are not too extreme. Several passive indexes are tilted naturally to tech because of their performance over the last decade.

Good call on reducing the margin debt. In light of recent interest hikes and market volatility, you have to be careful with some brokers which do like to raise margin requirements to 100% even on ETFs if there’s some volatility spike and might automatically liquidate positions. If you have access to a fast credit line either on your shares or homes from a private bank it would be good to have it on standby in case your broker raises margin to 100%.

LikeLike

@Pro. I’ve been tracking my unitized returns for 22 years now and I’ve very glad I didn’t touch 80/20 type portfolios with a 10 foot bargepole. If I had I’d been looking at returns of around 6% in USD with a return vol over 16%. That’s an appalling performance with a Sharpe of less than 0.4.

Thankfully, I stuck to a much more diversified portfolio with never more than 50% equities. Instead, I put my money into multi-managers like Millennium and macro funds like Bluecrest and Brevan. End result is return of 14%/annum in USD and a Sharpe close to 2. One down year of 0.5% in 2015. With an 80/20 type portfolio, my net worth would be over $25mm less. This year I would have lost $2.5mm in net worth (that’s after earning over $5mm pre-tax in compensation). Instead my net worth is up nearly $10mm with a 20% USD portfolio return this year.

So these things do depend on your experience. Yes, over the last 10 years equities have been wonderful. Over the last 22 years, pretty rubbish. Either way I prefer a much lower volatility portfolio than coulfd ever be constructed using just equities and bonds.

LikeLike

Congratulations on your outlier portfolio. That’s what makes capitalistic free markets so fantastic. Some go for 20%pa and 2+ Sharpe, while others are happy with 7.5%pa market returns.

To me, the gated black boxes are scarier than an 1929 equity drawdown.. Didn’t some (or all?) BlueCrest fund get liquidated recently? “Residual holding in AllBlue Limited and AllBlue Leveraged Feeder Limited (“AllBlue Funds”) As previously reported, on 22 December 2021, the Financial Conduct Authority (“FCA”) announced that it had decided to impose a requirement for BlueCrest to pay £40,806,700 for having inadequate arrangements to manage conflicts of interest. The Commission ordered the Respondent to pay $107,560,200 in disgorgement, $25,154,306 in prejudgment interest, and a $37,285,494 civil money penalty, for a total of $170,000,000, to the Commission. The Commission also created a Fair Fund, pursuant to Section 308(a) of the Sarbanes-Oxley Act of 2002, so the penalty paid, along with the disgorgement and interest paid, can be distributed to harmed investors (the “Fair Fund”). BlueCrest has paid in full.”

LikeLike

@Pro. I want my portfolio to hedge my future liabilities, not generate growth. That’s my idea of a true passive portfolio. I constrain my input risk, the returns are an output of the model which I have no control over. It’s constructed to be low risk, low vol and to perform best when my liabilities grow rapidly. The fact it generated 14% over that time is just luck. Nonetheless, I don’t see any point holding portfolios that can lose 20% in a year when inflation is 10%. That is a terrible hedge.

Re: Bluecrest got rid of nearly all it’s external investors in 2015/16. So you are 6 years out of touch. They did get fined a miniscule amount for basically not being transparent about an internal fund (though I knew about it for the prior 15 years so I cannot believe everyone else didn’t know). Returns since they dumped external investors have been: 50%, 54%, 25%, 50%, 95%, 30%, 100%+. I’ll take that thanks. It’s higher risk now but I constrain my notional exposure in return.

The argument about black boxes. When you invest in an tracker, you invest in a synthetic replication. They don’t buy the actual index and you don’t know their exact replication strategy. You also get them lending out their bonds/equities for peanuts to hedge funds. You don’t understand the counterparty risk they take with that. Moreover, the companies in the index are “black boxes” to a great extent. Do you really know what is going on at Tesla? Does anyone really know what Musk is doing? Does he even?

When I invest in Millennium, I invest in 250+ trading teams (so over 1000 PMs), all of whom have a 5% stop and aren’t allowed to talk to each other. I may not know what they are doing but it’s massively diversified, has a very tight stop-loss, and 90% of the capital is in T-bills. So counterparty risk is minimal. I prefer strong risk management to a fake idea of transparency that trackers provide. Plus the results speak for themselves: 14% annual returns since 1989 (S&P 10%) , annual volatility 5% (S&P 15%), largest drawdown high to low 7% (S&P -51%), longest time to decline and recover 11 months (S&P 84 months).

We all have different approaches. I’m happy mine is lower risk than most.

LikeLiked by 1 person

That’s great but not really a repeatable strategy if allocating today. It also only applies to 0.1% of the readers of this blog.

LikeLiked by 1 person

@Pro. This is a blog about the 0.1%. Not the average person. It’s about people who earn 7 fig compensation or are entrepreneurs who have sold companies. Else how they would they have wealth levels in the 10s of millions as you and I do? How applicable that is to the median person is clearly minimal since they have modest savings. Investment is a fairly moot point for 90% of the population.

Nonetheless, something like Millennium is (or was) available to many with a HNW. $200k was the min investment size so hardly out of reach for anyone with a net worth in seven figs never mind 8 figs. Brevan is available to all via BHMG and has generated a decent 10%/annum since it started, generated 28% in 2022 and 170% over the past 5 year. It’s made a positive return in 18 out of the last 21, 10%+ equity market falls. So it’s a far more reliable diversifier than bonds, for example. There is more to investment than just equities and bonds.

LikeLike