We ended November in the UK with the same prime minister that we started with. That makes a change on October and September. Moreover, our chancellor of the exchequer (Finance Minister, in any other country!) remained in place too. A sigh of relief at these green shoots of stability could be felt all over the place – not least the political podcasts and Op Ed columns.

The UK government released its well signposted ‘Autumn Statement’, having successfully previewed almost every key measure in it. Bankers bonuses remain uncapped, but almost all the other moves from Truss/Kwarteng have been reversed. Notional tax rates are unchanged, but thresholds are either fixed or have been reduced, so there is a bit more tax to pay all round.

The main changes for me are the drop in the 45% tax threshold by £25k, and the corporation tax staying ‘high’ at 25%. The reduced 45% tax threshold adds 5% x £25k i.e. £1250 of tax to my annual tax bill, and corporation tax being 6% higher than it might have been will cost me considerably more than that.

Input prices are falling

Meanwhile, elsewhere in the markets there was a distinct sound of air coming out of the inflation balloon. Some key input prices have dropped significantly in recent weeks:

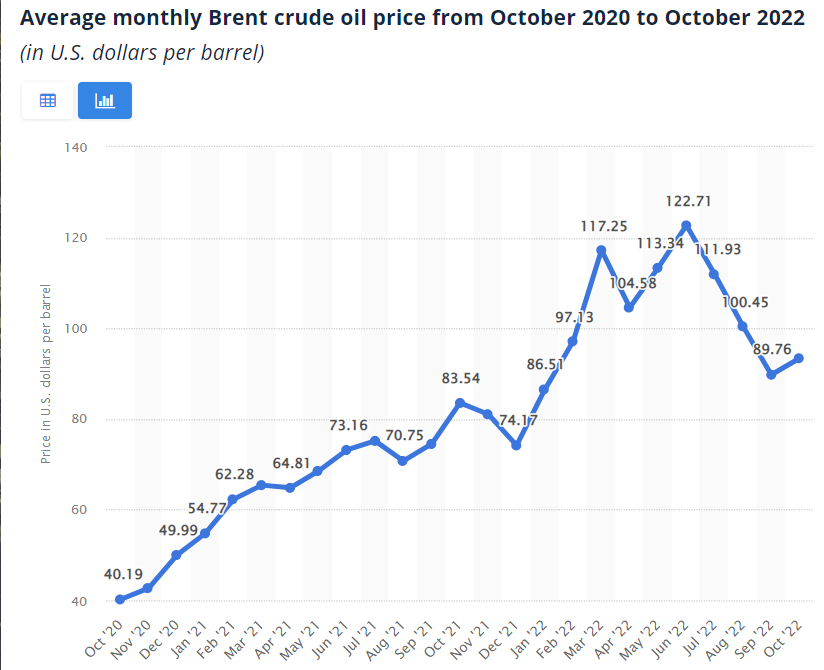

- Oil prices are down below pre-Ukraine levels, and about 25% down from peak.

Avg monthly Brent oil price, Oct 20 to Oct 22

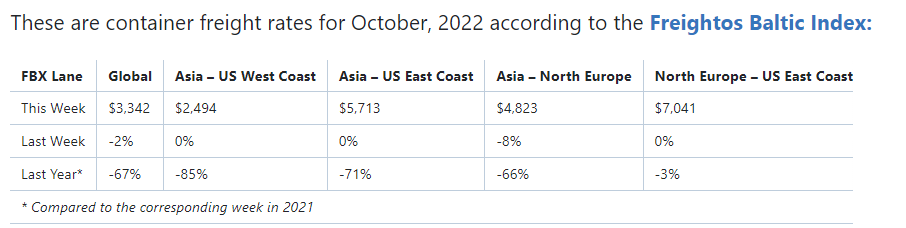

- Freight costs from Asia have dropped 66-85%

- Gas prices have more than halved from the summer peak. The graph below shows the price on 2 Dec for taking gas in Feb ’23 – this price remains about 60% higher than it was in January but it is less than half of the late August peak.

With these input prices falling – suggesting some output prices could potentially drop (which would be negative inflation) – the ‘inflationary spiral’ sentiments have started to dissipate. Interest rates now look likely to rise a bit less (i.e. still increase, but not by as much) than people thought a few weeks ago. And with that, bond prices are increasing – even in the UK – and confidence is increasing.

Markets in November

Equities everywhere continued to bounce off their bottom. Bond prices also rose – as yields softened – everywhere. And the USD weakened. It was this USD drop that was the most striking thing in my portfolio. The pound, having bought $1.03 during those wretched Truss weeks, has now brushed up against $1.23. That is almost a 20% swing, in two months. And most of what I say about the pound has been true about the euro too – the £pound:€euro rate has held pretty stable, apart from a brief Truss blip.

My portfolio’s month

My IB subportfolios’ results are emailed to me at the start of each month. Some of these emails were tantalising. My passive ETF portfolio rose 9%, my Ltd company portfolio rose 10%. However, most of these results are in USD, and once you allow for the USD drop in November, my returns were 3-5% across the board. My overall return on the month was 3.8%, versus a weighted market average (in GBP) of 5.2%. Not the first time, I am lagging the market this year. Hopefully my readers have fared a little better.

As regular readers will know, I am very focused on reducing the size of my margin loan. November saw good progress on this front. The GBP gain helped, because I have a hefty six figure debt in both EUR and USD. So thanks to the drop in the USD, my USD debt is now around 4.9% smaller than it was a month ago. My loan fell over £30k in GBP terms. My loan is now a similar % of my portfolio value to where it was at the start of the year (even though my portfolio has shrunk by around 20%) and, though the monthly interest costs are 50% bigger than they were, they remain manageable.

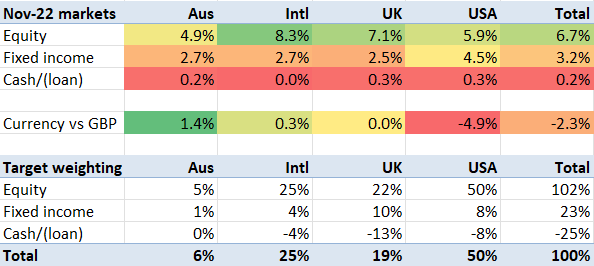

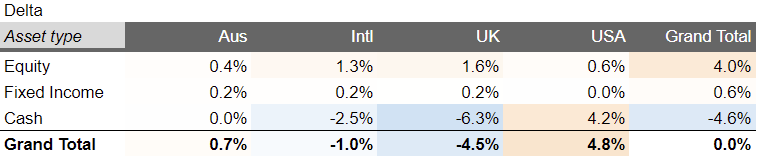

One KPI I track is the £ imbalance from my target allocation, which is over £100k smaller than it was a few weeks ago. This imbalance is still too far from £0 for my liking but I feel I’m in enough control for now. My delta from target allocation at the end of November is shown below. I am a little bit underweight USA Equities (normally my biggest exposure by a factor of 2).

The other monthly metric I pay attention to is dividend income. November has been annoyingly sparse for dividends, partly because some holdings that paid out in November 2021 have spilt over into December 2022. I will do a fuller analysis of this – and a @weenie chart – when I do a 2022 review, but for now it suffices to say that my trailing 12 month investment income is up about 5% on a year ago, but lower than it has been for much of this year.

We’re now in the final month of the 10th year that I have been tracking my portfolio rigorously. Plenty of funds don’t complete a ten year track record. I’m nearly there. A full review awaits.

Eagerly awaiting the 10-year review. This blog inspired me to track my own portfolio with a spreadsheet as well as write my own personal investment policy. It would be great to get your thoughts on strategic and tactical allocation. Would you consider allocating more to bonds now that interest rates are becoming normalised. Should age factor into allocation? What about tactical overlays? Sell-side consensus seems to be 20%+ decline in US stock markets. What do you think about leaning back for now from your target allocation to equities?

LikeLiked by 1 person

I expect, with no very high confidence, years of volatile inflation accompanied by a stock market crash.

So what? There’re umpteen other possibilities including the effective end of Western Civilisation. Or the end of the PRC.

One thing not to worry about is the Climate Change rubbish. In the present interglacial, temperature has been on a falling trend for millennia with wiggles up and down around that trend. There’s no good reason to think we’ll get anything different until eventually the ice returns.

LikeLike

That’s not what the UN’s scientists think

LikeLike

You don’t know what they think, you know only what they say. And what they say is talking their book.

LikeLike

That’ll do for me.

LikeLike

Been another great year in the markets. My top three holdings are thriving on the macro and rate volatility (up 11%, 115% and 25%, respectively in USD terms). My macro portfolio is having a great run in the last few years. Equities have been a disaster (sort of expected it to be even worse tbh) but thankfully only 25% of my portfolio was in that. Didn’t have much in the way of fixed income (<10%) but what I did still have (mainly EM bonds) got clobbered worse than I imagined. Made it up and then some on the mini-budget debacle which created fantastic entry levels. Not sure I see much further upside though. Commodities did really well but I didn't have enough (<10%). Property not really certain but I've marked it down just in case. Overall though still one of my best years in USD return terms.

Not sure I can really foresee much of a rally in conventional assets. Big problem is I can see macro volatility dropping which won't be good for the hedge funds I own which are all now much bigger than a few years ago (some 10x bigger). Plus will be sitting on 25% cash by early 2023 with no clear home for it to go to. That will dilute returns. So I think 2023 is a year for some heavy tactical trading. Major focus on the job since that will probably be the best returning "asset" for me.

Last few years have been incredible for returns and making $50 by 50 is very doable. Could not imagine that in 2017 when markets were just so dreary. Just need this volatility to last that little bit longer.

LikeLiked by 1 person

Hi FvL,

Recently discovered your blog and should thanks you for your detailed posts – they are certainly helpful to readers to grasp on concepts, metrics and apply them to their/my own portfolio.

I can see, as you mentioned several times, that you have a Ltd company for investments? Asking as I have been mulling over setting one for investments purposes, being more tax efficient, or that I believe. Is this incorporated in the UK? Can you, please, give some details on the setting up process, mistakes to avoid, etc? I think it could be very helpful to readers as after the recent change in taxation in November there is no reason to keep investing as an individual and get a hefty tax bill.

Many thanks,

LikeLiked by 1 person