This is the third in an occasional series of posts about angel investing. My first post looked at 10 Tips for new angels; my second post talked about what to expect of your angel investments. This post tackles a question that grows in importance as you build experience, and a portfolio, of angel investments: how much money to devote to it?

How big is an angel investment?

Most angel investments are between £5k and £100k. I am ignoring here the punts people can make on retail investment platforms like Crowdcube/Seedrs, which I will cover in a separate blog post.

A company raising money from angels will typically be raising between £100k and £1m. Their valuation will usually be between about £500k and £5m. A very normal round would be around £150k investment, buying perhaps 15% of the company (i.e. valuing the company, post investment, at £1m). In such an investment round, there would usually be perhaps 10-15 investors, ranging from £5k to £50k each. Investors with less than £5k to offer are quite a lot of bother for not much impact; conversely, an investor with £100k+ to offer might just strike their own deal – but these investors are rare and by definition such deals are usually hidden from view.

With £5k+ required per investment, angel investing is not really a regular FIRE activity. But it is a more common ‘Fat FIRE’ activity, and several regulars on the FIRE blogs mention dabbling in angel investing – not least Monevator’s TI himself. After all, even frugal FIRE types will amass well over £200k of investments before they are financially independent, and you might think that a £200k portfolio potentially has room for quite a few £5k investments. If you have a say 60:40 equity:other weighting, and if angel investing can deliver excellent returns, isn’t angel investing a potentially effective way to deploy your equity assets?

This blog post looks at the topic from the point of view of the allocation, which is a very dry topic until you have made a few angel investments and started to think about how they fit in to your net worth / FIRE / allocation.

1: The asset allocation paradigm

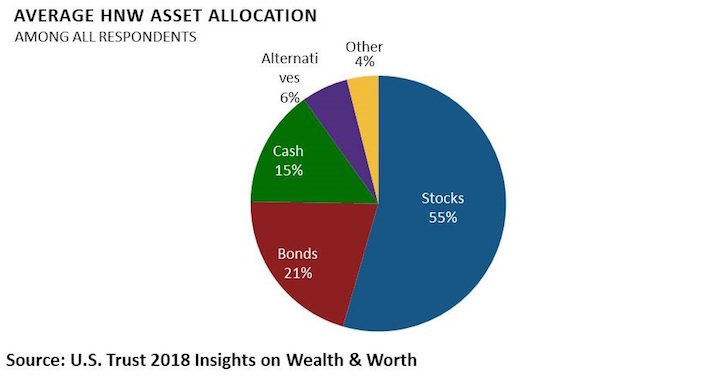

Most ‘textbook’ approaches to managing wealth start with considering the allocation into different asset types. A pretty typical, and therefore reasonably ‘ideal’, allocation is shown below. This ‘textbook’ says to have a reasonable pot of cash on hand, at least 3 months’ spending, and then beyond that have a equity:bonds mix with, usually, more equities than bonds. Around the fringes of that core allocation, feel free to have ‘alternatives’/other. You’ll see that in the pie chart below alternatives are shown as 6% of the total wealth; this is a fairly high allocation, as many people would say 5%/2%/similar.

What are ‘alternative assets’? Well, how long is a piece of alternative string? This label can be applied to anything high risk /illiquid / unconventional – this would include cryptocurrency investments, classic cars, old masters paintings, and certain hedge funds. It would also, usually, be where you’d put angel investments.

I have taken the asset allocation model very much to heart. As a lover of public equities, I have learnt the hard way the downsides of private investments, and think that treating them as ‘alternative’ is very important. So in my mental model, I think of angel investing as my ‘bit on the side’. I am happy to have a few percent of my portfolio in angel investments, but that is about it.

Challenges with the asset allocation paradigm

So, a few years in, and you’ve made a handful of angel investments. Say, for £10k, £15k, £20k, over 3-4 years. Against, say, a total portfolio of around £1m. And let’s say that you are targeting an allocation of 5-7%, roughly in line with the HNW pie chart shown above. You’re holdings are in roughly the right place, with investments totalling £45k out of a total pot of £1m.

The first challenge you start to face, as you consider your asset allocation, is knowing what value to place on your angel portfolios. The reality is that a few years after investing you probably have very little visibility in what your holdings are worth. You will (probably) know if one of the businesses has failed completely, which is fairly likely. But if one holding starts to do pretty well, what does that mean your investment is now worth? That is very hard to guage.

The second challenge, which is a high quality problem, is when one of your investments does really well. One of the appeals of angel investing is that a success can be a mega success – which I would define as 10x or better. If any of your first handful of investments, as described above, become a 10x holding, then suddenly your angel holdings are worth at least £100k – perhaps £250k. And suddenly your allocation is out of shape; your total portfolio is now about £1.1m-£1.2m, but your angel component is worth 10-20% of it.

What do you do? You probably can’t, and wouldn’t necessarily want to, sell down your angel investments – there isn’t a ready market for them. Do you instead sell down public equities, shifting into bonds? There is some logic to this – you have quite a lot of risk exposure in your angel portfolio, so perhaps derisk your publicly quoted portfolio. But now let’s suppose that your 10x-er is bought, for 10x; suddenly you have £150k of cash, and your angel allocation is underweight. You won’t easily find another £100k+ of angel investment opportunities overnight, and you may not want to redeploy all at once into public equities. Decisions, decisions. High quality ones, to be sure.

In other words, with a decent angel portfolio, there is now the question of ‘latest valuation, or original purchase value’. One approach is certainly to stick to using your book cost to value all your investments, unless something falls/disappears completely. Then if you have a 10x holding you’ll essentially ignore it when considering your allocations / net worth/etc.

A further problem with the asset allocation approach is that, once you have a few years behind you and a few investments in your portfolio, then you will be faced with the dreaded ‘follow ons’. Follow ons are when an existing business asks its existing shareholders for more money. If you are minded to participate in such opportunities, you will have even less control than normal in your timing and allocation – suffice to say that follow on opportunities do not tend to cluster at the moments when you are keenest to increase your equity exposure!

The basic problem with ‘asset allocation’ as an approach is that you can’t rebalance either in or out of angel investments in a reasonable timeframe. The right angel investments are not the ones that present themselves when you are underweight on angel, and if you make a good angel investment your ability to track its value is too poor to make a rebalancing decision robustly.

2: The windfall paradigm

So, if asset allocation frameworks are not very effective as a way of deciding how much to invest in angel investments, what other methods could we use?

One other approach is what I am calling the windfall approach. Otherwise known as ‘easy come, easy go’. This says that after receiving an unexpected windfall, such as an unexpected bonus, a bequest, a lottery ticket payout (!?), etc, these funds are good funds to put to work into something that itself might generate a windfall.

Under this approach I’d say you should normally ignore angel investing.

But if you come into a £50k windfall, and a couple of bright sparks you know well are looking for some help in setting up their software business, then putting £25k to work into their business might be quite a bit of fun. Sure, you could well lose the lot – but assuming you weren’t banking on that windfall in the first place, that won’t matter. And you might just make a decent windfall in a few years’ time out of that investment. In the meantime, you’ll feel part of an exciting journey, and hopefully have the gratitude and thanks of those two bright sparks.

Problems with the windfall paradigm

The windfall approach has the central advantage that you are very unlikely to regret your angel investments under this approach.

However it has several disadvantages too.

First of all, there is opportunity cost. What else could you have done with that windfall?

Secondly, the best angel investment opportunity is highly unlikely to be the one you are considering exactly after opening that premium bond good news letter. If you have just sold a large investment for £100k+, you are probably going to be an softer touch for the next 2-3 opportunities you see, than if you have just had to dip your hand into your pocket again for a long-in-the-tooth business that needs more help. In an ideal world, you’d assess each opportunity on its merits and without regard to your current flush-ness.

Thirdly, you won’t build experience and knowledge as effectively as you could with more regular angel investing. Which brings me on to a more common approach.

3: The income (a.k.a. tax relief) paradigm

The single most common approach I see in others is what I am calling here the ‘income paradigm’. This approach is particularly common with highly paid City finance types. It is to be trying to deploy a certain amount of this year’s total income – often out of the end-of-year bonus.

The UK tax system drives this particular approach.

Source: taxtrends.org

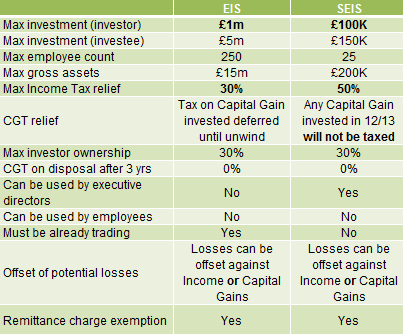

The UK gives very significant tax reliefs to angel investors, under the EIS (and its close sibling, SEIS) system. The Enterprise Investment Scheme provides relief to early stage investors in (most) companies in three ways. For a £10k investment in your friend’s software startup, EIS will give you:

- 30% (more, under SEIS), i.e. £3k back – as soon as you send them the certificate of your investment. I.e. you get £10k of shares for only £7k

- EITHER

- If things go badly, a further 20% of any loss. In the worst case, this is a further £2k back.

- If things go well, then any gain is free of capital gains tax (though any dividends are taxed normally). So if your shares end up selling for £30k, you’ll receive £30k after tax, which is 4.3x your £7k net investment.

These tax breaks encourage high tax payers to deploy ‘spare’ cash into EIS, especially around the end of the tax year.

But I also know regular angel investors without large end-of-year bonuses who budget to spend [£40k] on angel investments a year.

Strengths/weaknesses of the income paradigm

The income paradigm has quite a lot to recommend it.

For one thing, it fits into the annual budget in a fairly simple way.

Secondly, it forces some discipline – on making choices about which investment to pursue. You might think this new software business is a great idea, but is it the best one you will see this year? Will they not take your money if you waited three more months to see what else came along? And if that CBD pet grooming business that you put money in 2 years ago is asking for another £10k, how does that opportunity compare to this new software business? You only have £20k – is it £10k for each, or £20k for one, £0 for the other? This is a healthier way of looking at angel investments, and closer to how the professionals/institutions will do it.

The big weakness of the income paradigm is that it encourages people to invest to a deadline. City types are notoriously ‘dumb money’ in the Jan-March period that they are receiving bonuses/ending their tax year. If they don’t know opportunities themselves, they often look at VCT/EIS funds (that their helpful accountant can help them find) instead – a generally poor decision as I will explore in an upcoming blog post.

The no-paradigm paradigm

So, with the problems of either an allocation strategy, or a % of income strategy, what is the best strategy?

My personal strategy is really to have no strategy.

I started with a view that alternative assets should be a small % of my net worth. I’m glad I took this view, because I learnt several hard lessons for the first few years, but never was seriously stressed about the potential damage that any of my investments could do to me.

After 10+ years of angel investing I had over a dozen investments to my name, including the odd winner. This made me realise that, if I valued them at latest value, in fact my angel investments were well over 10% of my total investments. At points, notably after liquidating a load of my public investments to buy my Dream Home, my angel portfolio represented potentially a majority of my investment portfolio.

However eagle eyed longstanding readers of my blog will note that I tend to describe my portfolio as my ‘tracked portfolio’ – the portfolio I report on every month is the publicly quoted portion. I completely ignore my angel portfolio from the point of view of any net worth / FIRE / returns / allocations / complexity analysis. If I receive an exit from an angel investment, this windfall cash is often partially reinvested in my publicly quoted portfolio – but it doesn’t show up in my reported returns, which are unitised.

And if a promising new angel investment opportunity comes along, or more likely one of the existing portfolio persuades me to follow on, even if I no ready cash funds available, I dip into my publicly quoted portfolio to pay for it. Thanks to my margin loans, this doesn’t involve selling anything; I simply withdraw £10k/£20k/£30k from my margined account, the margin loan expands a bit, and my cash/debt position changes a bit – for a few weeks. At some point in the following few months, either dividends appear to pay down the loan, or I may sell down an overweight position, or I’ll top up the account from other sources, or similar.

When I make a windfall gain, which in my case is usually from an existing angel investment, I usually earmark a bit of it for some angel reinvestment in the next 12 months, but only very approximately.

What I lack is a constraint to provide discipline. I don’t have a ‘my annual budget is £25k’ approach. In theory, I might invest in the next three opportunities I see. In practice, my lack of time / focus provides some discipline.

The challenges I face with my approach are complexity and sprawl. My portfolio has tended to expand in size, and has not reached steady state. As it grows, the number of follow on requests has grown – resulting in significant and unexpected cash asks of me, sometimes at awkward moments. When I disappear, my angel portfolio will be the most gnarly bit of my estate to deal with. I need a new paradigm, I just don’t know what it should be. Any suggestions are very welcome!

I came at it a slightly more roundabout way. From my reading and (limited) interaction with the VC industry, I decided I needed to make at least 30 unlisted/start-up investments — and eventually closer to 50-100 — to maximise my chances of getting 1-2 true winners.

My total net worth (and similar thinking to you about total allocations) meant these were not going to be big investments individually.

It was this as much as anything else that directed me towards the crowd-based platforms. (I’d have happily put £500 to £1K into a private round with some whip-smart fellow, angels but clearly that’s too small for anyone to bother with!)

I have a separate sheet where I track all this, as part of my mega-master-spreadsheet. I track cost, cost after reliefs, and then valuation updated as per the most recent funding round. I then discount the whole lot by 50% to account for future lemons and for illiquidity.

This is after taking already-realised lemons out of the total, of course. (If this was a double-digit % of my net worth I’d probably discount harder!)

For a couple of years this looked very pessimistic (*cough* Monzo *cough*) but now looks about right, at least on a valuation perspective. Maybe not for liquidity.

The latter is hard to get your head around. One of my good friends always asks about my unlisted investments, and I usually tell him about the latest one to go wrong. Eventually I’ll mention something that has gone better so he doesn’t feel the need to stage an intervention, then he invariably says “Great, so when will you get that money out!?” The whole field is closed to him because of this mentality.

I don’t say that’s wrong (nobody needs to be investing in these, at all!) but it’s not the right mindset for unlisted investing. But then if I’m happy to answer “maybe never” then perhaps I should do as another friend does, and discount the whole lot to zero until anything is cashed out?

I do enjoy it, and have wondered if I should do it professionally. It’s particularly great fun when a more low-key company you haven’t heard from (funding wise) for a year or two suddenly does some sort of discreet pre-emption round and you find out the valuation is up 2-3x on last time! Wish it happened more often… 😉

TLDR: It has to be a fun money allocation, so do what makes you happy. 🙂

LikeLiked by 1 person

Medium time (can’t really say long time and be honest about it!) reader, first time commenter. And disclosure, I have no angel investments because I’ve only recently got to a financial position where it’s feasible to consider. However, I do have via my normal job access to some PE fund investments on a friends and family (or similar) basis. My theory is between the income and the no paradigm paradigm. That is, have a rough amount available per year to invest (which is itself based on a rough allocation cap) but each investment has to be one you “like”. It means some years you don’t invest the target amount and others you have invested the target and another good opportunity comes along – at that point comes the decision as to whether (a) the new / late investment is good enough to break the guidelines (no rules, more like guidelines right?) re the allocation I want to sit around (easier to conclude yes if the prior year is a down year) and (b) funds are available. It can mean missing some good opportunities but there’s no perfect way of solving for that . On the other end, amounts that get invested are then excluded from net asset calculations (carried at zero) which makes it a bit of a task to consider if the target annual investment amount should change (which is probably why I don’t think about that much – although that changes if there is a substantial change in tracked net worth). Far from perfect but gives me buckets that work in my head.

LikeLiked by 1 person

It’s quite…… I’m not sure what the word is, amusing? That you (and many others) are looking at such “risky” investments so that you can avoid the tax- really does show the government is rather unsure of what they want exactly. One hand is a tax/ni rate of nearly 50%, the other giving all that tax back if you invest in potentially risky smaller companies. Though, I guess you could say that its working as people are investing in these!

LikeLiked by 1 person

@Southwalesfi – In point of fact, I am not doing this to avoid tax – if I gave you this impression it is not right. But it is true that many people do angel investing largely for that motivation. My motivations have generally been to help somebody I rate; the tax reliefs have been a cherry on the top, and have led to me doing slightly larger investments and probably, on the margin, slightly more such investments.

LikeLike

Would you say it’s right that unless you are at the stage where pensions and Isas aren’t able to be utilised this isn’t something you should even bother with? That’s the conclusion I’ve come to on my own investments. I can’t quite fill my pension and one isa let alone utilise my partners so haven’t strayed into vc territory. I’m a high (100k) but not stupid high earner so have discounted these as not necessary for me personally

LikeLike

Belated reply to you @FBA… I wouldn’t quite say that you shouldn’t bother with it. I would say any angel investing should be done highly selectively, and strictly from a ‘starting a multi year learning process’ point of view. If a super talented guy from work sets up their own business and offers you a piece of it, by all means consider it – no matter what your pensions/ISAs are doing – as you have ‘edge’ in knowing how talented this person is.

LikeLike