This post is in an occasional series of blog posts (starting here) examining angel investing and the role it plays in high net worth peoples’ investment portfolios. This post looks at the ‘angel investing goes mainstream’ route of investing via crowdfunding platforms, drawing on an exclusive survey I ran on my blog.

I’m dealing here with equities – buying shares in companies – though most of my arguments would apply to crowdfunding platforms offering ways to invest in property, loans, and other asset classes.

This is the third in an occasional series of posts about angel investing. My first post looked at 10 Tips for new angels; my second post talked about what to expect of your angel investments. This post tackles a question that grows in importance as you build experience, and a portfolio, of angel investments: how much money to devote to it?

How big is an angel investment?

Most angel investments are between £5k and £100k. I am ignoring here the punts people can make on retail investment platforms like Crowdcube/Seedrs, which I will cover in a separate blog post.

A company raising money from angels will typically be raising between £100k and £1m. Their valuation will usually be between about £500k and £5m. A very normal round would be around £150k investment, buying perhaps 15% of the company (i.e. valuing the company, post investment, at £1m). In such an investment round, there would usually be perhaps 10-15 investors, ranging from £5k to £50k each. Investors with less than £5k to offer are quite a lot of bother for not much impact; conversely, an investor with £100k+ to offer might just strike their own deal – but these investors are rare and by definition such deals are usually hidden from view.

With £5k+ required per investment, angel investing is not really a regular FIRE activity. But it is a more common ‘Fat FIRE’ activity, and several regulars on the FIRE blogs mention dabbling in angel investing – not least Monevator’s TI himself. After all, even frugal FIRE types will amass well over £200k of investments before they are financially independent, and you might think that a £200k portfolio potentially has room for quite a few £5k investments. If you have a say 60:40 equity:other weighting, and if angel investing can deliver excellent returns, isn’t angel investing a potentially effective way to deploy your equity assets?

This blog post looks at the topic from the point of view of the allocation, which is a very dry topic until you have made a few angel investments and started to think about how they fit in to your net worth / FIRE / allocation.

1: The asset allocation paradigm

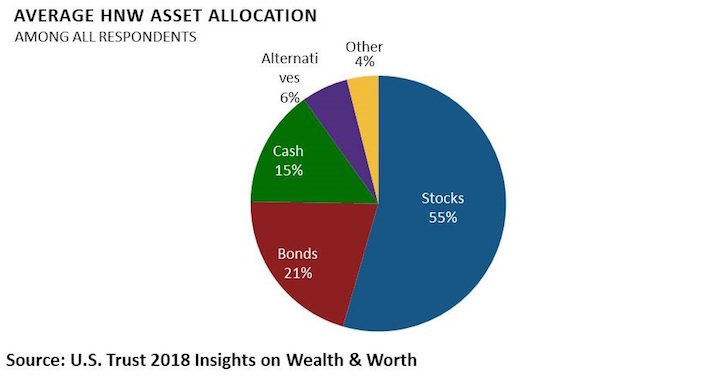

Most ‘textbook’ approaches to managing wealth start with considering the allocation into different asset types. A pretty typical, and therefore reasonably ‘ideal’, allocation is shown below. This ‘textbook’ says to have a reasonable pot of cash on hand, at least 3 months’ spending, and then beyond that have a equity:bonds mix with, usually, more equities than bonds. Around the fringes of that core allocation, feel free to have ‘alternatives’/other. You’ll see that in the pie chart below alternatives are shown as 6% of the total wealth; this is a fairly high allocation, as many people would say 5%/2%/similar.

What are ‘alternative assets’? Well, how long is a piece of alternative string? This label can be applied to anything high risk /illiquid / unconventional – this would include cryptocurrency investments, classic cars, old masters paintings, and certain hedge funds. It would also, usually, be where you’d put angel investments.

I have taken the asset allocation model very much to heart. As a lover of public equities, I have learnt the hard way the downsides of private investments, and think that treating them as ‘alternative’ is very important. So in my mental model, I think of angel investing as my ‘bit on the side’. I am happy to have a few percent of my portfolio in angel investments, but that is about it.

Challenges with the asset allocation paradigm

So, a few years in, and you’ve made a handful of angel investments. Say, for £10k, £15k, £20k, over 3-4 years. Against, say, a total portfolio of around £1m. And let’s say that you are targeting an allocation of 5-7%, roughly in line with the HNW pie chart shown above. You’re holdings are in roughly the right place, with investments totalling £45k out of a total pot of £1m.

The first challenge you start to face, as you consider your asset allocation, is knowing what value to place on your angel portfolios. The reality is that a few years after investing you probably have very little visibility in what your holdings are worth. You will (probably) know if one of the businesses has failed completely, which is fairly likely. But if one holding starts to do pretty well, what does that mean your investment is now worth? That is very hard to guage.