September saw some lovely weather. I found myself getting out around a lot of water, for some reason. London has a lot more water than just the Thames.

Autumn kicked in with a vengeance at the end of the month. Along with it, the surge in Covid-19 cases that has been occurring across Europe started happening in the UK too. The government brought in a ‘rule of six’ (people, maximum, except in workplaces / weddings). In London our lockdown remains relatively mild, but there is a definite question of how long that can last – while some pubs/restaurants are models of compliance, others aren’t – if I get covid-19 anywhere it will be from one of them, I am virtually certain. Most likely from some waiter leaning over me, with their mask not reaching their lower lip, breathing a dose-y viral load all over me in a confined indoor space.

I’ve been back in the office a few times. I’ve used quite a few Ubers, and been on the tube a couple of times. I’ve been out to quite a few restaurants/similar. My spending is definitely returning to normal.

That ‘summer’s over’ feeling

Early in the month, a cause of the prolonged ramp in tech stocks was revealed – a ‘whale’ at Softbank, buying call options on major tech stocks. This, combined with herd behaviour from retail investors who have discovered stockmarket investing in lockdown, appears to have propelled some of the big hikes in stock prices. The whale unmasked, tech stocks took a tumble. NASDAQ, a reasonable proxy for tech, fell almost 10% on the month.

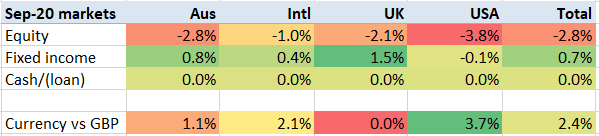

In the wider markets, the rising stream of covid-19 cases bodes badly for the winter. The confidence that was palbably returning in August has equally palpably drained away in September. Equity markets were down across the board, particularly in the USA – where there appears to be something of a Biden discount occurring.

Here in the UK, the mood music on Brexit (where the UK and the EU are in the closing stages of trying to agree a post-transition trade deal to take effect from 1 January) also deteriorated. This led to the GBP falling versus pretty much everything, especially the USD.

Markets moved, on a constant currency basis, down by 2.3% in September. Foreign currencies moved up, on average, almost exactly the same. This left the weighted market movement at precisely zero. Against that simple bar, my portfolio underperformed – my portfolio fell by 1%. I think this underperformance was roughly explained by my outsized tech holdings.

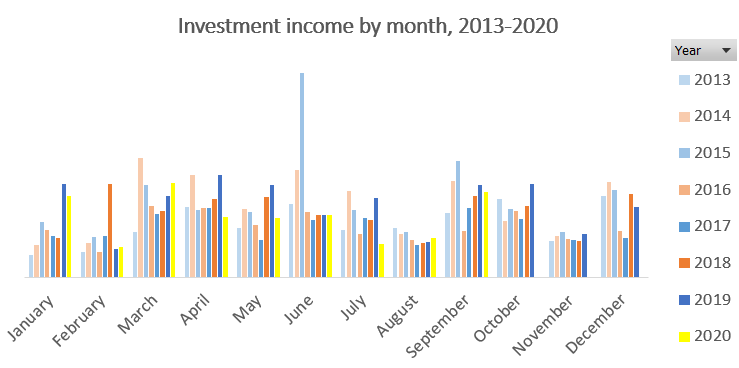

My dividend income has dropped considerably in Q3. I’ve shown my ‘@weenie graph‘ below. July was particularly miserable, with less than half the dividend income of July 2019. August, usually a very thin month, actually saw a very slight rise, year-on-year, but the normal bumper September harvest was slightly down on last year’s figure. Considering I have invested a house sized sum in the market six months ago, this is very disappointing – but it has been expected ever since the national lockdown kyboshed the economy in late March.

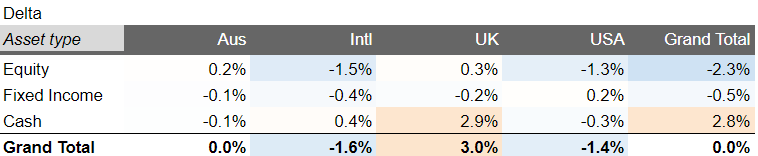

As a result of the paucity of dividend income to reinvest, I have been quiet on the trading front. I have done a modest rebalance from US Fixed Income to International Fixed Income, but otherwise held very steady. I remain slightly underweight on equities, and slightly long on cash (in fact, short on GBP debt).

Looking ahead to the next quarter, we have both Brexit and the US election to contend with. Both of these could create significant volatility for US markets and currencies. However, neither threaten the US’s unrivalled technology leadership position. And with covid far from behind us, I think tech stocks represent as safe a haven as any – and I can’t see tech being dramatically affected for better or worse by either Brexit or the US election. I’m sitting tight, for now.

{kind=link}

[…] FirevLondon (25) […]

LikeLike

Tech is at pole position today but then there are movements such as one depicted in Social Dilemma (documentary on Netflix). How far can the party last if regulations tighten?

LikeLike

Loveed reading this thank you

LikeLike