The Taliban’s back. The West has been vanguished. We all read the media. There wasn’t anything else to read.

I was surprised to learn that total UK deaths in the last 20 years in Afghanistan numbered less than 500. Total USA deaths: under 2400 (fewer than 1900 as a result of hostile action – leaving me shuddering about the other 500). A lot of treasure but not, in the scheme of things (compared to, say, road traffic, alcohol, let alone covid-19), that much blood. For reference, the UK lost 258 people in the Falkland conflict, 47 in the Gulf War and 179 in the Iraq War.

In the business press there is a lot of talk of supply chain shortages. Pictures of empty shelves. Tales of shortages of lorry drivers. Rampant inflation. I don’t see these things in evidence around me but what you see on the internet can’t be wrong.

London is starting to feel a little bit like normal. People wearing masks are a frequent sight – though almost always on a voluntary basis. Restaurants are filling up. I haven’t used the Tube in over a month but carriages are now sometimes standing room only again. People are getting covid but it is starting to feel like a nasty cold / flu / etc – nobody is panicking.

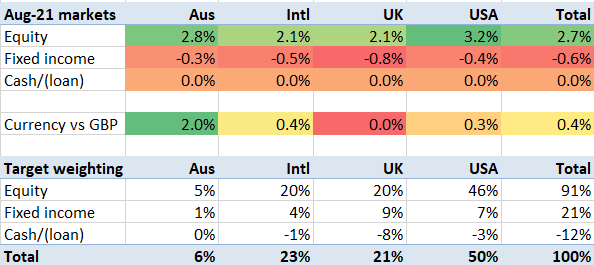

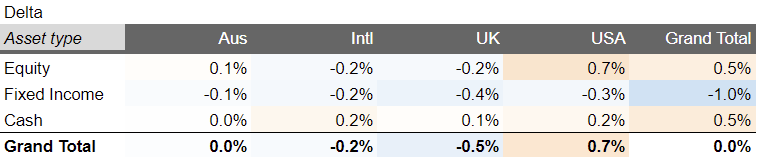

The Afghanistan news has had negligible impact on the markets. Which makes sense to me, insofar as I can’t quite see what impact higher terror risks, a resumption of the Afghan opium trade, the shredding of Afghan women’s rights, and a potential humanitarian crisis has on the stock markets either.

China stocks continue to be under pressure. But no new news, as such.

Beyond that, the stock market just seems to climb and climb and climb. Bonds shed some of their July gains. The Australian dollar climbed a bit. But not that much to report.

My portfolio’s returns are as usual shown here. I saw returns of over 3% on the month, slight overperformance reflecting some strong performances among tech stocks in particular (Google up 7%, some smaller stocks like ESTC up over 10%).

I swapped out some iShares and Vanguard ETFs for their Lyxor equivalents in August, after doing my own research prompted by an old Monevator article (which is out of date as far as the wrinkle it mentions, but up to date in terms of the price-competitiveness of these Lyxor ETFs). Lyxor ETFs now account for over 5% of my portfolio, and iShares/Vanguard are both under 25%.

I’ve had a couple of windfalls recently, so have been topping up the portfolio. As a result the tactical cash overweight of the last few months is definitely being reduced / leverage is going up slightly.

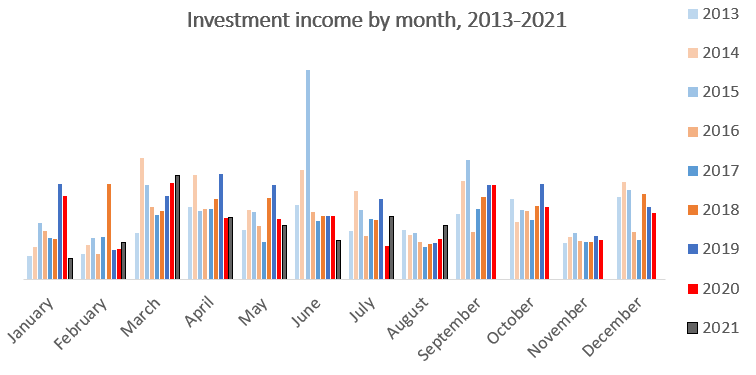

Lastly, I’m interested to note the income levels I saw in August. Dividend/etc income has been down since the pandemic, but in fact August’s income was my best August ever. This partly reflects my portfolio’s increased size, but it is the first month that I can declare record income for since I bought my Dream Home over 5 years ago – even though my portfolio has been at record levels for over two years now. I think a combination of my topups to the portfolio plus dividend payout normality being resumed bodes well for income for the rest of the year. September, as a bumper dividend month, will be a key test.

“The West has been vanguished” You must spend too much time thinking about Vanguard funds.

LikeLiked by 1 person

Regarding Lyxor ETFs, are they domiciled in Luxembourg?

I read that Ireland domiciled ETFs have a tax advantage on dividends from US shares:

“dividends of US securities are subject to a US withholding tax of 30%. Prefer Ireland except where the fund holds only non-US stocks.”

https://www.bogleheads.org/wiki/Domicile#Ireland_and_Luxembourg_domiciled_UCITS_funds

Comparing total return against Irish ETFs tracking the same benchmark over longer time spans may show a difference.

LikeLike