In the UK, July 19th was long-awaited (and once postponed) ‘freedom day’. Or, as the FT aptly renamed it, ‘surrender day’. Despite rapidly rising cases, and technocrats loudly reminding people that unlocking was not ‘following the science’, the UK removed many restrictions on July 19th.

At the time of writing, this move appears to be paying off. While it is too soon to judge the impact of a policy enacted only 12 days ago – given the lags in the virus’ severest impacts – the case count has in any event been falling for a week. Over 90% of UK adults now have antibodies, and the role that children have in spreading the virus remains unclear (paywall link here).

The average age of people with cases is around 25 – and people with 2 jabs almost entirely escape intensive care, let alone the morgue. In my local neighbourhood the case count has just hit an all-time high, but the hospitals remain relatively unaffected.

London remains distinctly subdued. But with last week’s opening of the borders to fully vaccinated EU/USA visitors, the tourist trade should start to pick up.

The most notable news in the markets in July has been the China crackdown on foreign investors. The direct attack has been on education stocks – one unfortunate tycoon has been hit to the tune of $15bn – but the total value destroyed across Chinese stocks in the month is around $1tn. But the collateral damage has hit the big listed tech stocks too. China officially bans foreigners from owning any of its businesses, something that has been largely ignored/circumvented by the investors on NASDAQ investing in Alibaba, Tencent, Didi etc. I have a small holding in Alibaba (technically, in its US-listed Variable Interest Entity) and have been puzzling over whether to close out or extend it. Opinions welcome in the comments.

The main market news is inflation, with USA consumer price inflation hitting 5% for the first time since 2008. I see inflation is a feature, not a bug, in the macro picture at the moment – at least from the point of view of policymakers. I also consider equities to be a reasonable source of protection from inflation. The likes of Amazon, Google, Nestle, JP Morgan etc have revenue sources (and costs) mostly linked to the price of goods and assets – so as prices rise, so should their revenues and profits.

Right at the end of the month we saw some stellar earnings results from the USA’s big tech groups. Amazon’s share price was a notable casualty here – despite good results, expectations took a knock – dropping 7%. It is my biggest holding so this impacted my July return noticeably.

For some reason bonds have risen significantly in July. This was largely recovering from previous falls. I do not understand bonds well enough to explain this. UK bonds rose almost 3% in the month – almost as much as USA equities.

My portfolio’s returns are as usual shown here. My portfolio underperformed the market by about 0.5% on the month, but I’m still enjoying the ride.

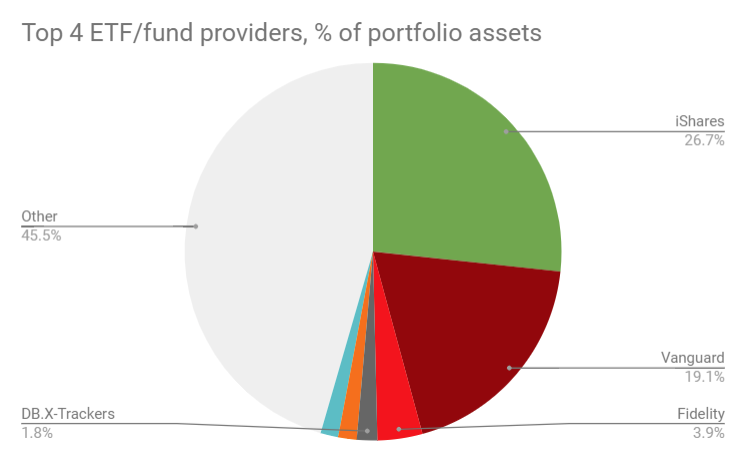

One metric I keep an eye on, but haven’t shared yet in the block, is my concentration risk against the big ETF providers. I would like to keep my biggest ETF provider – Blackrock(/iShares) – at no more than 25% of my portfolio – just in case the unthinkable happens to them. In practice Blackrock, the European market leader in ETFs, is generally slightly above this target – and would be higher still if I didn’t actively seek out substitutes to it.

In the meantime, my allocation remains roughly in line with my target. I have more windfalls anticipated in the next few weeks so I will be bending a little in the wind over the next couple of months.

Hi FIRE – I held Alibaba too, but have bailed out recently after the recent dramas. I think it’s a great company but ultimately it will either have to escape the clutches of the Chinese government and put its headquarters outside China (as most Western companies do that conduct business in China) or delist completely. I think all funds in Chinese companies are at risk currently.

LikeLiked by 1 person