July has been travel month. Not for me, in fact. But London has been full of visitors – and Mrs FvL and I have been inundated. So much so, that it has been handy to have the Coastal Folly for overspill. But London has a lot to offer and it has been fun doing some touristy stuff.

Summer in London

Visitors in mid July saw the hottest temperatures ever recorded in the UK. London saw 40C for its first time. I confess I was down at the Coastal Folly at the hottest point, where sea breezes kept temperatures to a lovely 30C. So I missed the bring-your-cat-to-the-office mayhem going on up in town.

(UPDATED: it was hot in Downing Street too, with Johnson finally resigning early in July. That is too well covered for me to add any value here)

The markets had positive momentum throughout July. VWRL, Vanguard’s world equity ETF, was up throughout the month and ended up 6.2%. Bonds took a bit longer to rise but from mid month they too rose significantly. With the 25% leverage I’m targeting, my markets rose on average just over 6% – the fifth best result in at least 7 years.

My portfolio went up even more than this, rising almost 8%. For the most part this was due to my long exposure on Amazon. AMZN’s share price rose over 25% in the month, following reassurance about its trading (on the non-retail side, at least).

I took the opportunity of the market popping so much to take a few ‘profits’ – I sold about 0.5% of my portfolio, in margined accounts, reducing my margin loan with the proceeds. In particular I sold some Amazon stock – something history has taught me to regret doing – but with the recent volatility and my overweight position it feels like a bet I can sensibly take.

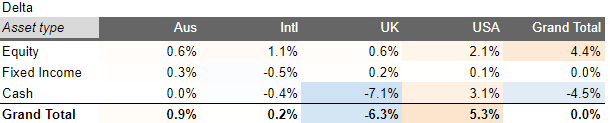

I also rebalanced slightly, rotating about 1% of my portfolio out of USA equities and into Fixed Income and UK equities.

As a result of these gyrations I ended July with almost exactly the same portfolio value as at the end of May, but a total loan 5% smaller than then. My leverage ratio has dropped visibly. I remain significantly short of cash but less badly than a month ago.

The astute reader will see that I am in fact overweight USD versus target, and underweight GBP. In other words my margin loan is more in GBP than ‘normal’, and less in USD. This is a tactical overlay on my target allocation – right now with the USD so strong and no UK policymakers sticking up for the GBP, I would rather borrow the declining currency than the rising one. I may yet change my target but for the moment I attribute this stance to the Ukraine war, and I will wait to see how that plays out for the next few months.

I wonder if you are unnecessarily over-complicating things and dont just go for 100% US equities exposure?

LikeLike

Not if you agree with Modern Portfolio Theory, which I do. Having a balance of equities and risk should be a better mix of risk/return.

LikeLike

I’ll have to read up on the Modern Portfolio Theory. It seems like you are spreading things out pretty well and eliminating home country bias with your exposure to US equities.

LikeLike