This post drills in to the niche that I have found myself in – of having an uncomfortably high level of leverage margin during a bear market. None of this is worth trying at home so for you to continue reading I assume you are anticipating some schadenfreude, car crash blogging, or perhaps some material to share with your crazy crypto mates.

I have become quite a fan of margin lending. Just reviewing first of all the journey I’ve taken…

Normal mode: 10% leverage

I first dabbled with margin lending, literally on the margins, about 10 years ago. More recently, about five years ago, I decided to use the lending strategically, and for several years I set my target asset allocation to include approximately a 10% level of margin – i.e. I own assets amounting to 111% of my portfolio value, having borrowed 11% to fund the purchase; the 11% loan is 10% of the total asset value. I consider this level of leverage to be minimal risk, because the dividend yield off such a portfolio will, under auto pilot, pay off about a third of the loan every year, even if the markets suffer significant falls.

For completeness, I should mention the rest of the debt I hold. I have a modest level of mortgage debt on investment properties, on a mixture of interest-only and repayment arrangements. These investments generate significant free cash flow, which is mostly used to (over)pay down mortgage principal. I have no other significant debts. Unless otherwise stated, I ignore the mortgages when talking about my leverage level.

In terms of affordability ratios, in normal mode my total loans (including mortgages) amount to about 4x my income (including investment income), and about 10% of my net worth (including properties). Nothing here that would give my bankers too much trouble.

Unorthodox procedure 1: buying House 1

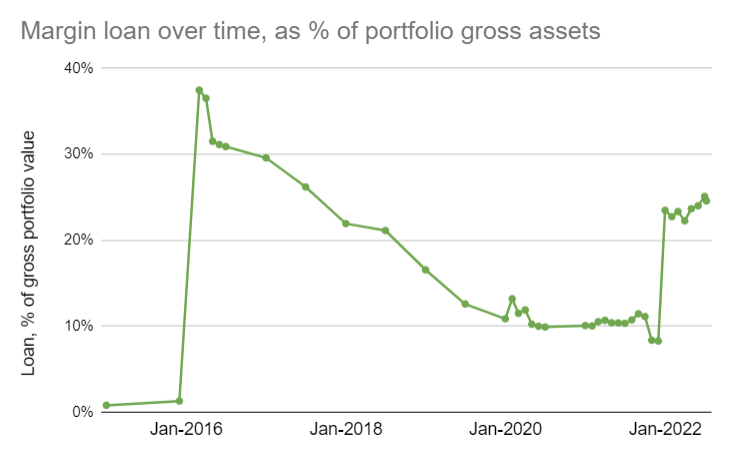

A key moment for me was when I took a large risk in 2016 by buying my Dream Home with a margin loan. I pushed my Loan To Value temporarily up to almost 40%. To be fair the Value here wasn’t my entire household net worth, it was only my own liquid portfolio, but it was still a level of leverage that could have caused me trouble. Fortunately, for a reason of anticipated reasons (windfalls I was expecting) and unanticipated reasons (Brexit hitting the pound, which reduced the value of my loan against my global portfolio) and the extended stock market boom, I never looked back from that initial high level of leverage, and four years’ later I had my leverage back down to 10% again.

It is worth highlighting the simple arithmetic behind my leverage fall from 38% to 10% over four years. Falling from 38% to 10% is a drop of almost 75%. And indeed during that time, my loan shrank significantly, but ‘only’ by 55%. At the same time my gross assets increased in value by 51%. The combination reduced my loan as a % of total value by ~75%, to 10%. Rising markets hide naked swimmers, and they rapidly reduce leverage (which is why we should expect western governments secretly to support inflation for a few years yet).

Unorthodox procedure 2: buying House 2

Second time around, last December, I used another margin loan. This time around my loan was even bigger than for The Dream Home, but given my larger portfolio in 2021 than 2016, the loan to value was smaller. It started off nonetheless at almost 25% of my gross assets, and over 30% of my net value.

I set my target allocation at a cash allocation of -25% of net value, i.e. a loan to value of 20% (25% loan as % of (25%+100%) is 20%). Being on target means the loan is a third as large as the net portfolio (net = 75, which is 3x 25). Though this was my target, my immediate position after buying the Coastal Folly was to be significantly over-indebted, with an imbalance of about 5% of my portfolio value. I hoped to see myself steadily reducing leverage and getting closer and closer to my target allocation.

What happens next?

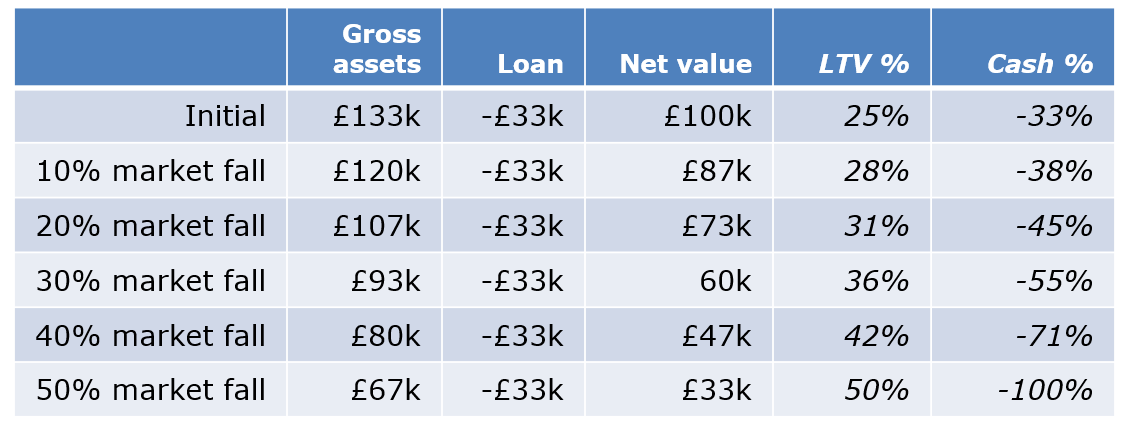

At a LTV of 20%, any movement in the gross assets is multiplied (levered, ahem) by 5/4ths. So a 10% drop in the assets produces a 12.5% drop in the portfolio value.

First of all, after a drop in the value of the assets, if one doesn’t reduce the loan in line then the leverage has just gone up too, to 22%. So the next 10% drop in assets in fact produces a 12.86% drop in portfolio value. Pretty soon you are talking about real money. In my case, markets have fallen so far, and I have not managed to reduce the loan as quickly, so my loan to value has increased to 25%, a long way up from the targeted 20%. At 25%, every drop in the markets is magnified by 4/3rds.

When is a nasty negative return not such a nasty negative return?

I am attemping to stop regarding my portfolio as a leveraged portfolio, and instead to disaggregate it into two things:

- My holdings of assets. The ETFs, stocks, bonds, unit trusts etc that I own. I like these, irrespective of what they are worth, and I do not want to be forced to sell them.

- My margin loan. This margin loan is taking on scary properties, but in fact it is *just a loan*. Not dissimilar to an interest-only mortgage. Who is scared of an interest-only mortgage? (The subject of another blog post in the future, no doubt….).

Thinking of it this way around ensures that the % gain/loss every month is not the primary metric. Instead, I have two clear priorities which have different primary metrics.

- Do not sell assets.

- Pay off my liability.

1: Do not sell assets

This is the relatively easy part. In practice I do sell things every so often. But what I am not doing is selling down an asset and not recycling the cash. So whenever I sell, I make sure I top up elsewhere in my portfolio. Not necessarily the same account, but somewhere in the same tracking system. My metric here is ‘net sales/purchases (£)’.

2: Pay off my liability

My primary metric here is ‘net movement of the total margin loans’. Ensuring this movement is downwards is difficult, especially since I’m not allowing myself to sell assets to raise cash. So how am I doing this?

First of all, any unexpected windfalls I receive are being used to pay off the liability. I don’t get too many of these windfalls, but have had two in the last six months – as angel investments I made long ago were sold and I received my (modest) share of the proceeds.

Secondly, I am trying to use cash from dividends. This is proving more challenging than I had expected, as I’ll explain.

I track my investment income every month. It is a healthy number and it has been rising steadily all year, despite the market drops. In theory I can repay 5% of my loan every six months from this income – which would certainly be useful to keep my leverage under control. However in practice about half my holdings are in accounts which I either can’t or don’t want to access – such as my pension SIPP, my tax-free ISAs, or Mrs FvL’s unleveraged (and less taxable) accounts. This is a quality problem, clearly.

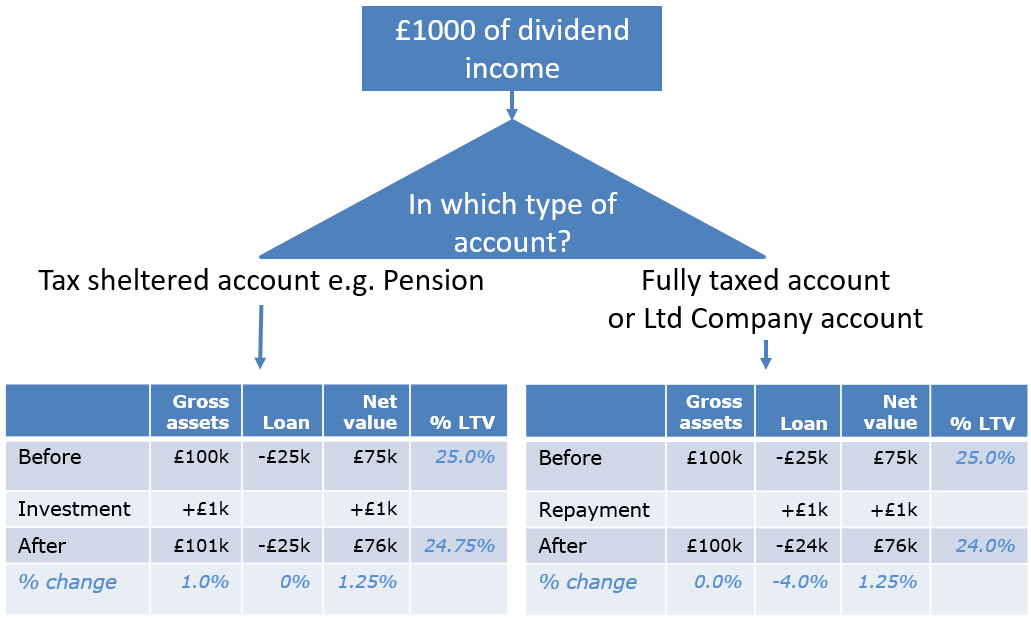

Every £1000 of income that I invest, instead of using to repay a loan, also helps my loan-to-value, but at a 25% LTV it helps only one quarter as quickly. Assuming a portfolio gross value of £100k, with a £25k margin loan, £1k of income invested in more assets reduces the LTV to 24.75%. Whereas using it to reduce the loan would reduce the LTV to 24.0%. So with about half my income being reinvested, not repaying the loan, progress would be 2.5x slower than I had anticipated – if my LTV was still at 20%. In fact with a higher LTV, buying more assets is slightly more impactful on the LTV – but my progress is still twice as slow as I had mentally set myself up for.

So in fact I have managed to reduce my loan by just under 5% over the last 6 months, thanks to some windfalls and some dividends.

Revisiting those affordability ratios again, right now my total debt (including mortgages) is about six times my annual income, and about 15% of my net worth. Six times income is towards the upper end of what I think is reasonable; 15% of my net worth suggests I remain very much under control at a balance sheet level.

One more thing – interest costs

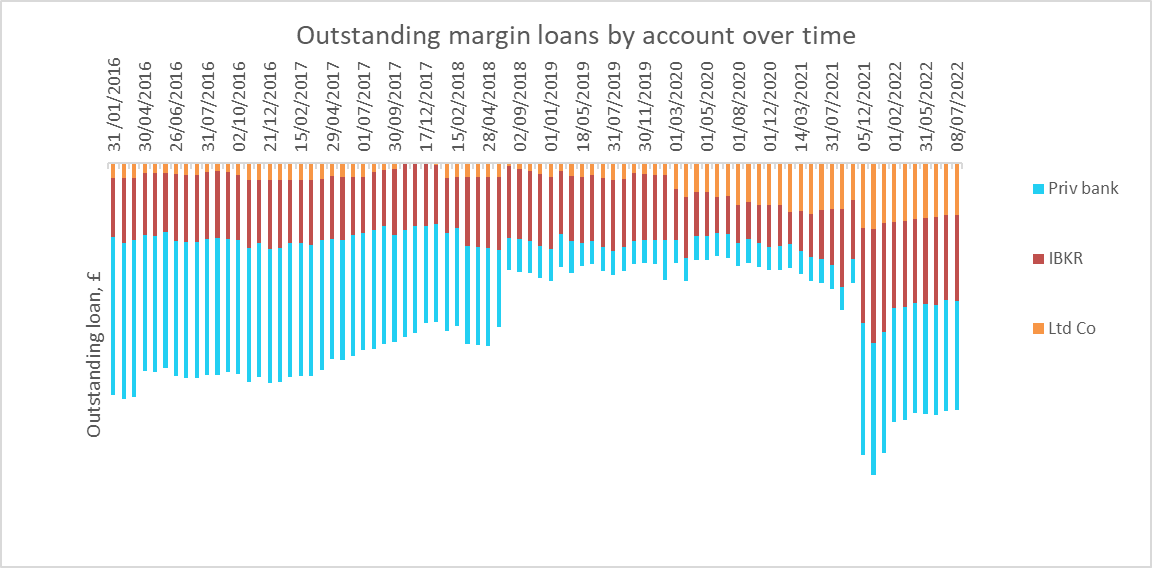

This update wouldn’t be complete without reference to the interest costs I’m paying for my margin loans. Much of my loan is with Interactive Brokers, which is commendably cheap – generally less than 2%. But with base rates rising, what has happened to my interest costs? Thankfully, not much. My blended rate (including the pricier private bank) has risen from 1.73% at the start of the year to 2.39% now. Interest costs remain far lower than the dividend income provided by the portfolio. But of course they are continuing to increase.

Next steps

But to get my leverage back in line, assuming no market recovery, I need to chop 25% out of the loan. That will call for patience. Or, perhaps, swapping out some of my margin loan for a mortgage – which shifts the repayment challenge somewhere else in my personal finances. I am going to need to hope for another windfall or two!

Thanks for the update FireVLondon, and very glad to hear you still appear to have everything under control. 🙂 Must admit my thoughts had turned to you occasionally in the past six months, albeit more with genuine concern.

You seemed to have entirely avoided what I consider the biggest risk of this operation — brokers changing the rules / margin requirements on either a whole or per security basis. I suppose Interactive Brokers is a superior outfit to the smaller platforms where I saw carnage play out from this in the financial crisis (luckily as a bystander!) but am still surprised the past six months volatility wasn’t enough to even bring this onto the amber radar.

I’ve mentioned this before but I’d urge you to incorporate it somewhere into your thinking/framework, and you don’t mention it at all above? I know, you’ve got infinitely more experience of running a leveraged portfolio than me so here’s how to suck on an egg. 😉 (But really, at the least perhaps see what IB did in 08/09 if you’ve not already? Do you feel you have some kind of legal protection to avoid it changing the rules? Look at Robin Hood et al with Gamestop for a recent example of rule changing overnight, albeit in a different context.)

Perhaps your portfolio comprises sufficiently non-volatile stuff for this not to be an issue for the broker, but most things have been volatile the past six months… 😉 Perhaps they are looking at you more holistically than platforms did in the last crash?

The other thing you don’t mention as a recourse is those investment properties. I presume they are ripe with capital gains? And I appreciate you’re not setting them off directly against the investment portfolio. Still, they must be in the picture, somewhere?

Perhaps to feel better about it you could sell one off, take the CGT hit, then use the proceeds to increase the investment side of the ledger? That way you’re bringing your leverage down without, effectively, selling low. (Indeed you’re buying!) Obviously doesn’t reduce risk to the same degree at all, but nudges it?

Just a little rambling food for thought.

Good luck!

LikeLiked by 1 person

Yes, fair shout – I have not mentioned this at all! Am wondering whether to edit the much read (thank you for Weekend Reading link!) post or do another one or put reply in comments. The short answer is that most of my collateral is very liquid indeed and I don’t perceive the risk of IBKR changing the rules to be high/material.

LikeLike

Very interesting article, once again thanks for the detail.

Not too much to say beyond to echo the investor. I looked closely at margin loans a year or so ago but worried that at precisely the point where you most need security – i.e. in times of major financial distress, the institution providing the margin loan has the opportunity to pull the plug. Hence why I went with a five year fix at now. In your position, like you, I’d be paying that loan off asap. If you pay it off slowly, most likely you make more money. However tail risk could be materially negative for you and that would keep me awake at night. Hope it works out.

LikeLiked by 1 person

Aristotle, or some lesser sage, said that if you’ve won the game stop playing.

Suppose you took that attitude – suppose you sought wealth preservation rather than wealth growth. How would you go about it?

LikeLike

wealth preservation rather than growth, in a world of 8-10% inflation, feels pretty similar to growth, I think? Perhaps I would allocate more to real estate/property, and also to income-producing investments, pegged off defendable/predictable cashflows. But I think I would not manage to preserve all my wealth in the current environment.

LikeLike

Am thinking of using one of the 2 uk private bank margin lending facilities to remortgage my own home, what do they typically charge at moment?

LikeLike

not sure I understand the question – margin lending is lending off an investment (stocks/shares/similar) portfolio, not a home. What exactly do you have in mind?

LikeLike

Sorry for not being clear, I have a large equity portfolio and would like to use it as collateral to get a new mortgage fix for my current home, I understand that barc/coutts, as long they have custody of the total assets, will offer mortgages against your equity portfolios.

LikeLike

aha yes. Barclays/Coutts will both offer margin loans against equity portfolio. I think rates are around 2% above base – significantly more than IBKR but similar to mortgages. The loan to value can be quite high – e.g. 70% of the value of any (tradeable) assets that they manage, and of most liquid assets beyond that.

LikeLike

[…] spent a fair amount of time pondering solutions to these questions when I read this post from FireVsLondon. I do not have definitive answers yet, but it is excellent content for a […]

LikeLike

[…] the meantime, my leverage is getting worse. What am I doing about that? I will tackle that in a separate post […]

LikeLike

[…] Life on the margin – FIRE v London […]

LikeLike

[…] Life on the margin – Fire V London […]

LikeLike

You’ve written quite a bit about margin loans. Have you explored the economics of spread betting? It’s a lot harder to get your head around but the implicit borrowing costs seem quite favourable and (contrary to what is often said) I think might be suitable for long-term holding. I started doing it recently and the maths requires a few cold towels, but I’m pursuing it as a small portfolio strategy right now with a view to ramping it up if the experiment goes well and if I can finally get some straight answers out of IG about how they price their forwards (which in practice seems to be the cheapest way to place a long-term bet). Key differences versus a margin loan: (1) the finance cost of spread betting effectively ‘scales’ with your position, you end up paying a finance cost which is proportionate to the size of your position when you sell, rather than it being fixed at the outset, and (2) (crucially) it’s tax free for everyone except ‘professional gamblers’ so you don’t get the obvious hinderance of margin loans which is that the interest is non-deductible, and there’s considerable upside benefit.

LikeLike

No, I haven’t. As a source of leverage, spread betting sounds interesting. As a source of funds – to buy things outside the portfolio – it doesn’t help. My margin loans derive mostly from the latter.

LikeLike

True, it doesn’t work as a direct source of funds, but if you sell down an ETF position of £X and place a (5x leveraged) ETF spread bet with £X*20% margin, you get to much the same result as borrowing £X*80%. Higher maintenance than a fully collaterised trading account, I’m sure, but with other potential upsides. On a related note, could you check the message I sent you on your ‘About’ page?

LikeLiked by 1 person