June was gloomy.

Not in London, which is lively, crowded even – and a delight to see. Pavements are busy, restaurants are proving tricky to get bookings in, the river is heaving. I even managed to get to ‘the beach’:

I managed to spend a bit of time down around the Coastal Folly too. I’m still finding my rhythm having two homes but so far it is going pretty well. A London kitchen project is running late / badly which gives us plenty of excuses to be down by the coast.

The UK saw a week disrupted by rail strikes but with Working From Home now an option and so many cycle/etc options it didn’t feel too disruptive for me. It was interesting though how positively the union leader Mick Lynch came across in the media and I think if we do find ourselves in a year of employee-driven strikes he will deserve the credit/blame for it. The RMT appears to be asking for about 9% pay increases for train workers. Drivers are coming up next, apparently, along with GPs (asking for 30%!). We are rapidly getting away from ‘inflation is just spiking up temporarily’ to ‘well, if they’re getting it, then I want it’ and that could take years – and a much more competent government – to shake out.

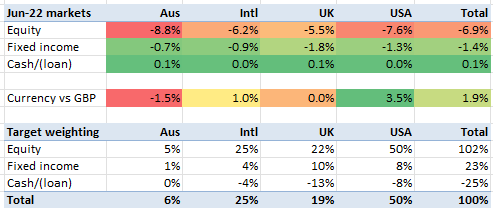

And it is this inflation gloom which is suddenly pervasive. Not just in the UK, though the UK does appear to be taking a particular bruising. Markets got hammered in June and, lest anybody forgets, they hadn’t had a good run of things earlier in the year either.

In fact, in general equities carnage, the UK’s FTSE remains relatively unscathed. The S&P was down 8% and Australia’s ASX down 9%. Such carnage tends to boost the USD and June saw the GBP fall 3.5% against the USD.

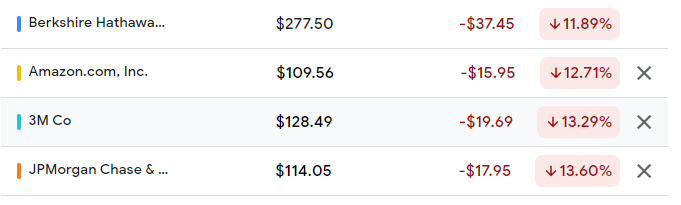

Though the tech sector has been most painfully hit, there aren’t many places to hide. Just the four US heavyweight stocks in the table below tell a painful story (and bonds were no respite either):

UK media (that I read) is full of references to how uniquely weak the GBP sterling is. This is a very UK/US perspective. I have yet to read the (more correct) interpretation that in fact the USD is uniquely strong. With EUR rates still unchanged at -0.5%, there is scope for the Euro to gain significantly, though it has a large Italian bonds headwind that could push it the other way.

My portfolio lost 7% in June. But for me the big milestone in June was breaching my worst yet drawdown. It has now lost 21% from peak – which it has not done (on a month end basis) in the last 9.5 years that I’ve been tracking.

UK readers will for the most part not have hit this painful milestone yet. My performance is worse than most because I am significantly leveraged. June results saw this writ large; in most of my leveraged subaccounts, my holdings lost 7-8%, but due to the leverage my portfolio dropped 11-14%.

Yet there isn’t much evidence the downturn has hit bottom yet. For instance:

- Based on long term earnings multiples (CAPE), the USA remains above historical norms. And earnings could well fall, pushing P/Es up, before we are done yet.

- There is not yet evidence of reaching the bottom among ‘lossy growth stocks’. The likes of DOCU, HUBS, CZOO are not at their bottom yet.

- Interest rates are clearly going to carry on rising. The Bank of England’s governor is talking about increasing the speed of increase – from 0.25% to 0.5% per jump. The ECB hasn’t even actually increased rates yet, after 11 years.

- The Ukraine war continues, and has a good chance of lasting through the European winter. This could have unpredictable but painful effects on energy prices / consumer sentiment / inflation.

I have lost two years’ of growth – the unitised return on my portfolio being back at the August 2020 levels. In the scheme of things, this is not too bad. A further 5% (taking the drawdown to 25%) would take us back to July 2019 – which doesn’t seem too horrendous either. We have to drop a further 10.5% from today (29% from peak) to take us back to July 2018, which feels possible. If we fell 40% from peak, which is roughly as bad as most bear markets get (though I would get there first due to leverage), we would be back in early 2017. That feels, right now, in the ‘unlikely but possible’ zone.

In the meantime, my leverage is getting worse. What am I doing about that? I will tackle that in a separate post shortly.

Interesting times! I yesterday added an additional 10% leverage to my (100% equities) portfolio. Borrowed at 2.3% 10 year fix, invested in VWRL and VUSA. Now approx 23% leveraged.

LikeLiked by 1 person

great update. cheers!

LikeLike

Hi, great post as usual. Seems from your ‘Investment Diary’ that you’re paring back exposure to the hardest hit areas (US growth/tech stocks) in favor of sleepier UK value and commodity dominant AUS markets. I would have thought this was the time to lean into those areas hardest hit and shy away from regions/sectors which have already benefited from Energy / Commodity related resilience (that’s my simpleton thinking at least). Is this a personal exposure management decision(?), or do you think there’s more pain for US tech relative to UK/AUS value in the short term? My biggest fear is the QQQs taking off as soon as I start reallocating capital to ‘less volatile’ areas (UK/AUS). Thanks

LikeLiked by 1 person

One thing I am a bit puzzled about is that the US S&P has taken more of a hit than e.g. FTSE , but nonetheless I see my US Equity exposure rising ahead of target (usually when global markets drop). I think the USD strength is part of the reason.

I am not changing my target allocation and am generally following its guide as to when I rotate – i.e. I sell overexposed things and buy underallocated tihngs. But when buying I am tilting towards ‘less volatile’ things – e.g. I am buying the Oz index, not XRO – and selling ‘more volatile’ things not the index, e.g. single stocks like HUBS, DOCU, ESTC and not selling VUSA, SPXD.

LikeLike

Dave – good questions. In my experience rebalancing doesn’t work so well with sectors let alone individual stocks. And in particular I find it hard to see ‘the bottom’ with any of the tech stocks I know best. A rev multiple of 6 rather than 12 is still a high rev multiple. I think AMZN below $105 (already slightly distant memory, 3 weeks after your comment!) is cheap, but a further drop of 25% on QQQ is quite easy to imagine. In the meantime a couple of growth-y UK stocks such as AHT and DOM feel at least as good value. In my own case I still have a large exposure to QQQ-ish stuff so if it does start taking off I will go up with it. As indeed somewhat happened in July.

LikeLike