A Coastal Folly

One thing has, after all, led to another. Against many years of better judgement, Mrs FvL and I have taken the plunge and bought a second home on the UK’s south coast. Our Coastal Folly.

This blog post tells the story of how I’ve paid for the Coastal Folly. I’ve surprised even myself with how it’s happened.

The Coastal Folly is expensive. Well over £2m of property. It is not a little 2 bed cottage 20 minutes drive from the sea. It is a premium piece of real estate, with uninterruptible sea views.

As a second home, it attracts additional stamp duty (the property transaction tax payable in cash to the government at completion) – for this value of property my stamp duty is well over 10%. A lot of people I know froth at the mouth at this level of stamp duty. Not me. My portfolio has benefited from low investment taxes. And most of what I spend my money on incurs 20% VAT. So having to shell out 12-13% purchase tax on a discretionary purchase, using money that has been taxed at 0% or 20%, doesn’t feel unreasonable at all to me.

Rustling up £3m

So I’ve had to find, for argument’s sake, about £3m. This is before any furnishing / renovation / upgrade work.

When I made my offer it was a ‘cash offer’ – I said I was not using any mortgage finance. This enabled me to move quickly and be in control of the process, which I think was to my advantage.

My vague plan when I put my offer in was that I would fund the property through three means:

- Some spare ‘windfall’ cash I had received recently and had not put to work

- Selling down a small portion of my invested portfolio, drawing on unsheltered accounts.

- Borrowing money via my margin loan – i.e. enlarging my existing margin loan(s)/portfolio finance arrangements.

I was able to pay the 10% initial deposit out of ‘windfall’ cash, and that gave me a little bit of time to get organised around finding the remaining funds. Apart from a wobble in which my private bank thought that I couldn’t use their margin loans to buy property, until they relented, I have gone ahead very much in line with my vague plan.

What I had not taken into account was capital gains tax. Once I realised that selling down unsheltered assets would involve realising significant gains – and thus becoming liable for significant capital gains tax – I became a bit more aggressive about borrowing the money, rather than selling down assets.

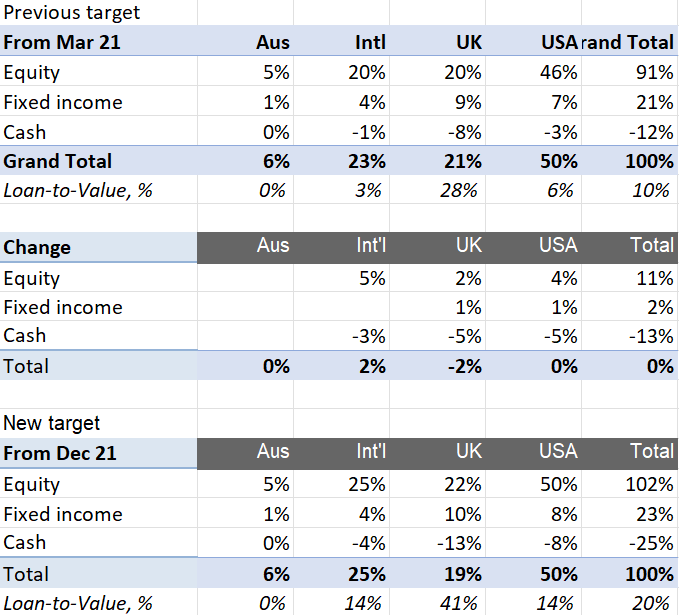

As a result I have adjusted my target asset allocation. I am now aiming for a loan amounting to 25% of my total investment portfolio (net, which is equivalent to 20% of the Gross value – i.e. if the portfolio is £12.5m Gross, with a £2.5m loan, then the net total is £10m). Initially I will be slightly over levered versus even this new target, so any rebalancing will need to slowly whack that loan mole flat until I reach the 25% point.

This loan is in EUR, GBP and USD – about half in GBP (resulting in quite a high LTV against UK assets), the rest split USA and International in line with my target weightings. I am already finding the EUR margin loan tricky in practice because I don’t have many EUR holdings and don’t like feeling that I am borrowing EUR to buy (even EU-focused) GBP holdings. So I may yet adjust the loan target away from EUR but for now the theory beats the practice.

Alongside that loan adjustment, I am increasing my fixed income target slightly – to reduce the volatility of the leveraged portfolio. I am also increasing my target overseas exposure – largely at the expense of my UK exposure – reflecting my greater disillusionment with the UK FTSE, the increase in my (property) UK assets, and the significant home bias evident even with a reduced UK target.

A free house

I had told myself that raiding my portfolio for funds would set me back 2-3 years, and that if I was financially secure 2 years ago, I would still be financially secure after raiding my portfolio. This assumes I can absorb the extra running costs of an additional home, which in the scheme of things I think are a rounding error.

What I now realise, doing the annual sums, is that if anything my position has been set back only 12 months, not 2-3 years after all. My invested portfolio (which excludes properties and illiquid assets) has ended 2021 worth almost exactly the same as it finished 2020. And that’s despite having funded a c.£3m house purchase. As Mrs FvL put it to me, “we have bought a house for free”! Or putting it another way, if my returns (and windfalls, to be fair) in 2021 had been +0%, I’d be in the same place, but minus the Coastal Folly.

Managing a £3m loan

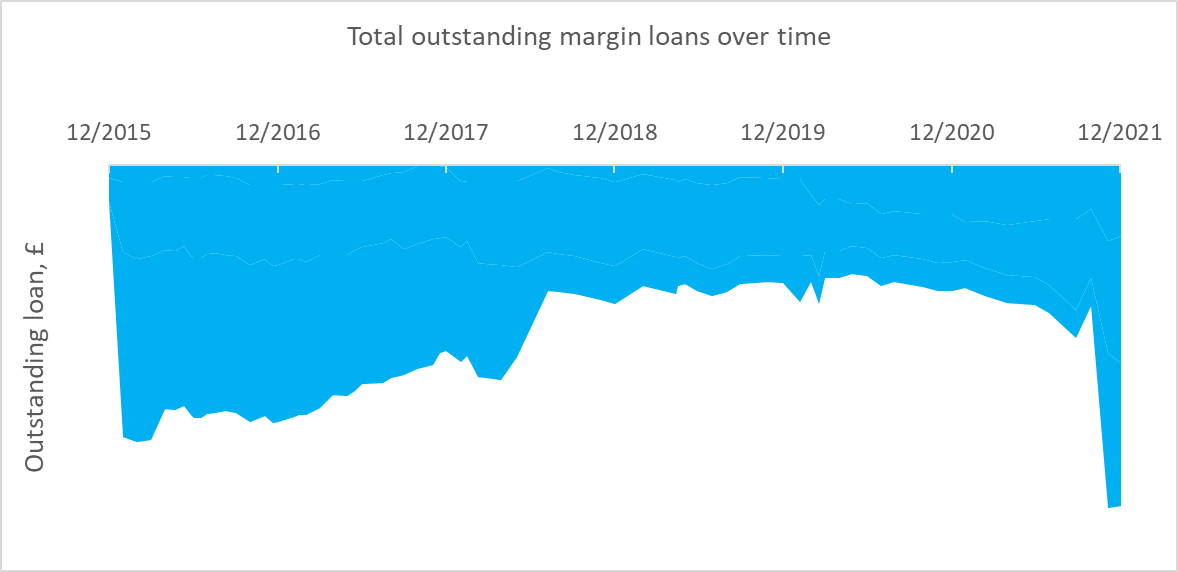

As you can see from the above graph, the blue Net Total may be in the same place as it was at the end of 2020, but the composition is different – the dashed Gross total is quite a bit higher, and the yellow Margin Loan has grown a lot. By taking out the extra margin loan I haven’t had to sell many holdings at all. However, this leaves my enlarged margin loan at around £3m. This is the biggest it has ever been – somewhat bigger than it was even at its peak just after I bought the Dream Home in early 2016.

When I bought the Dream Home, which was my first serious foray into using margin loans in the physical world, I was significantly leveraged. My loans (orange, in graph below) then were almost half of the value of the accounts they were borrowed against (orange+blue), so a drop in the markets of say 25% would have put me under real pressure. I was aware of the risk, and managing it carefully, but it was a real risk. While I didn’t manage to sell my previous home when I expected, in the end I was fortunate that markets were kind to me (thank you Brexit!), and via a mixture of repayments from windfalls and market gains I had managed to get my leverage to a ‘safe’ level by the end of 2017.

My increased loan exposure, of about £3m, leaves me in some respects no more exposed than the ‘safe’ level I reached by Q4 2017. My total portfolio has grown considerably since 2017, so the new record level of loan is, in proportionate terms, no higher a proportion of my total portfolio than the smaller debt was in 2017.

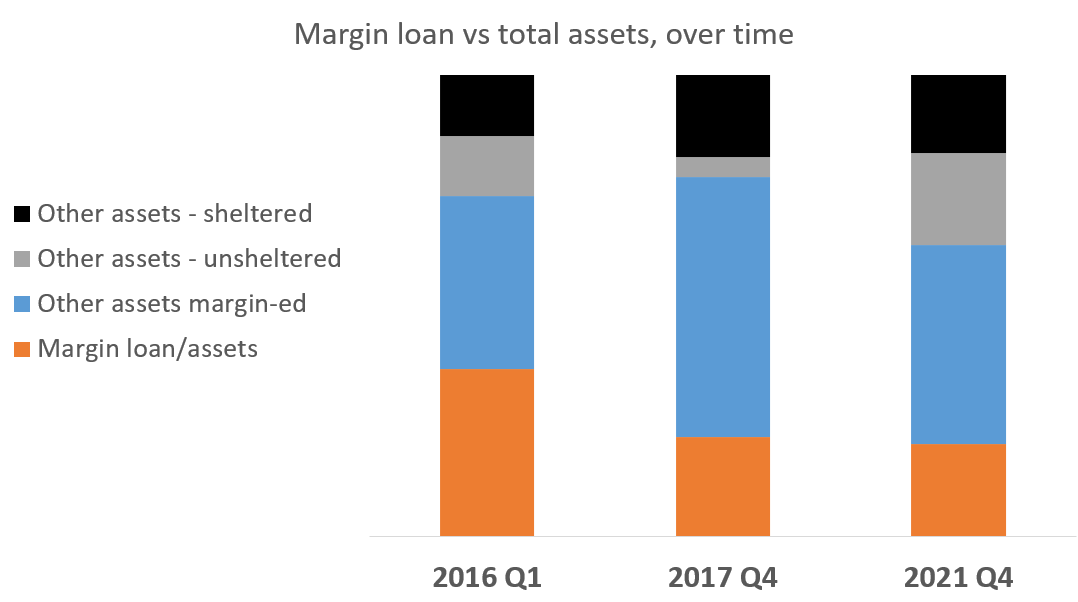

As it happens I use margin with two brokers – my private bank and Interactive Brokers. Back in 2017 these brokerages had the vast majority of my unsheltered funds (i.e. excluding the black segment in the graph above). But now I have quite a bit invested in other accounts too – the grey portion above – which I could easily move into a margined account but at the time of writing is not available to my lenders. So my lenders only see the orange and blue bits, but not the grey or black bits.

One of the key risk ratios here is the Loan To Value – LTV. This is the orange section, as a % of the orange plus blue section. It has just risen to about 30%. If you took into account my total value, including the grey and black sections, my overall LTV is closer to 20%, but for the purposes of avoiding margin calls the number that matters is what the lenders see and that is around 30%.

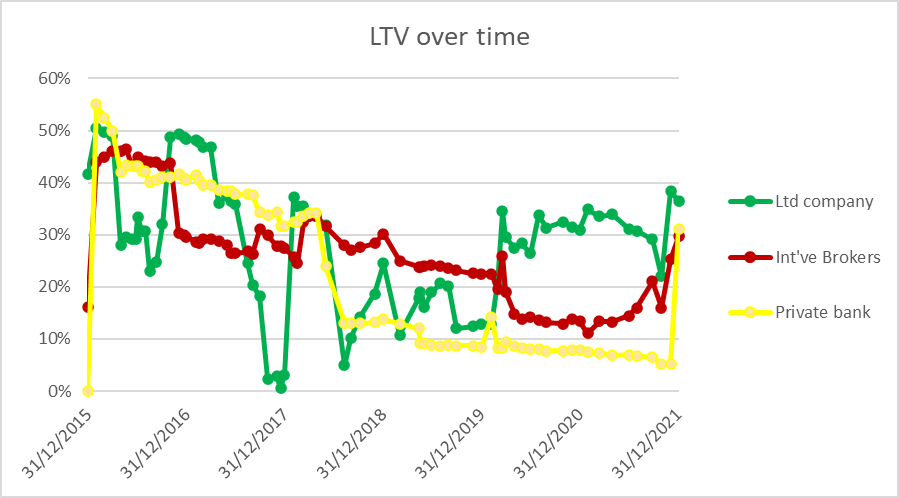

In fact what really matters is the LTV on each account. I have different brokers, and multiple subportfolios within the brokers. But the headline three numbers are shown in the line graphs below – the Maroon and the Green lines are Interactive Brokers (personal and via my Ltd company respectively) and the Yellow line is my private bank. You can see my LTV has jumped up into the 30%+ zone, which is a level I haven’t been at since 2017. But it’s not as high as I was at when I bought the Dream Home. These days I consciously run the Ltd company leverage at the highest level of the three, because interest charges are tax deductible for companies (but not for me as an individual).

As to the cost of funds, Interactive Brokers as ever beats my private bank. I’m paying a blended 1.3% to IB, and 2.35% to the private bank (tho I think I could roughly halve this if I consolidated all my funds with them). I’m expecting total annual interest costs of under £50k (and dividend income of at least £70k from the collateral assets). This feels very competitive with a mortgage alternative, but hasn’t required any income disclosure or repayment commitment that would come with a mortgage.

Avoiding Bill Hwang’s mistakes

I need to make sure I don’t inadvertently become the next Bill Hwang – the billionaire whose fund Archegos overextended its margin loan to a level that hurt not just him but some of the biggest banks in the world.

As well as LTV, a ratio that matters a lot is the ‘headroom’ I have left above the amount of collateral I have. With Interactive Brokers (IB), the proxy for collateral is ‘initial margin’, and the headroom is indicated by the ‘Avail funds’ (so called because is the amount I could spend on new investments).

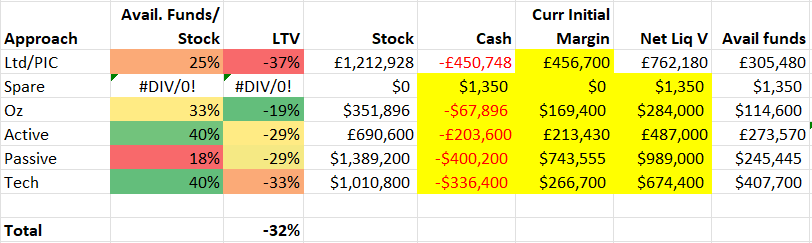

One trap for the unwary is that some stocks are better collateral than others. And as it turns out, I have one sub portfolio which I now realise has more ‘unsuitable’ holdings in it than I knew. This is revealed by my colour coding in the table below (note – numbers are illustrative, not actuals). The ‘Passive’ subportfolio, running at 29% LTV, has only 18% Available Funds – whereas the Active and the Tech subportfolios have 40% headroom despite running at very similar LTVs.

Digging in to this further, I discovered that the culprits are some of my newly acquired Lyxor ETFs such as LCUK and GILI. Whereas for large tech stocks, IB wants only 25% of the value as collateral, for relatively illiquid Lyxor ETFs it wants 100% of the value (i.e. you can’t borrow anything against these securities). My Passive subportfolio, and my Oz subportfolio, have quite a lot of unmarginable ETFs in them. I think from IB’s point of view ETFs on other exchanges are higher risk, so the Oz ETFs I use have always been difficult to margin. But thankfully for the holdings in my Passive subportfolio there are marginable alternatives from Vanguard/iShares – e.g. VUKE not LCUK, and INXG not GILI. I may take a slight hit in higher fees / more concentration risk, but when I need to manage my loan exposure this is a very small price to pay.

In fact even as I wrote this blog post, IB is reducing the margin available against GILS, one of Lyxor’s ETFs:

The red box on my margin dashboard has led to me rotating back out of Lyxor and towards Vanguard/iShares. I will look to rotate the other way in my sheltered accounts, which I can’t margin.

I am still not completely safe here so my portfolio will need attention over the coming months, to ensure I get my leverage levels down to ‘safe’ levels. In the meantime, I am really learning for myself why rich people buy houses differently from the rest of us.

Nice analysis, FvL. Congrats on your 2nd home!

If I understood correctly, one risk is IBKR arbitrarily increasing the margin requirements to, say 100%. This would trigger margin calls and your collateral would be sold unless you topped up.

And this is usually done when there is a downturn or an expectation for one.

What happened in March 2020 in terms of IBKR requirements? Did they panic?

Also, what are your thoughts on “buy utility rent luxury”? Cheers.

LikeLiked by 1 person

Just an FYI with IB. They recently gave me a margin increase notification notice for VDEM[0] which moved from 25% to 100%. VDEM is the USD version, whereas the GBP version VFEM is staying at 25%.

I found this a bit peculiar and I tried to imagine what would happen if IB decided that VWRL, my biggest holding, would be lifted to 100%. I would have the same problem as you — if I were to switch into a random S&P 500 ETF, I would have to pay a hefty capital gains tax bill.

Also, reminder that during the US elections in 2020, they put up the margins to 33% across everything. The only good thing is that they do announce you very early. So, you do have time to run around and find the liquidity in case one needs it.

[0]: Vanguard FTSE Emerging Markets UCITS ETF Distributing

LikeLiked by 1 person

Margin requirements for mutual funds at IB are rules-based only (at 25% but only after 30 days from purchase for some reason), whereas ETFs are risk-based and subject to IB’s whim. It would seem holding say Vanguard FTSE Global All Cap Index Fund leaves you in a safer position than VWRL.

Vanguard funds also used to be commission free to purchase but IB’s agreement with Vanguard has apparently changed recently so it now costs £4.95.

LikeLiked by 1 person

Congrats on the 2nd home FvL…

Very interesting post and a lot I can relate to.

A few thoughts/comments:

– I was surprised to receive an email from IB saying lending against HMWD was being removed (although perhaps they have since reversed this decision as the Margin Requirements are still showing as Default).

– This is a great link to use to check what lending is available with IB, if you don’t yet own it with them: http://tiny.cc/ibmargin (see Margin Requirements section)

– For buying a property, I personally like to use IB for short term borrowing, to be able to move very quickly like you did, then refinance immediately after (if with a private bank) or after 6 months with a retail bank (computer usually says no otherwise). Whilst the rates available with IB are great, a small interest premium to remove any risk of margin calls/IB arbitrarily changing rules is a small price to pay.

– A mortgage also has the benefit of reducing your net equity in the property. E.g. if a property/wealth tax was to appear (similar to IFI in France) it would likely be based on net equity at the point of introduction. In France for example, you aren’t able to refinance to reduce your liability after the fact, so presumably the same would apply if one was to be introduced in the UK.

– I believe you are still working? Hence you should have access to great mortgage rates. Failing that, via private banks.

– A personal favourite would be an offset mortgage. I.e. continuing to borrow within your Ltd company’s IB account (lower rates & tax deductible). Yet have 75% of your property’s value offset in cash as dry powder, ready to deploy instantly for margin calls, other short term opportunities, etc, with only 25% net equity in the property itself. Assuming you meet retail bank lending rules, you wouldn’t pay any interest if fully offset, only the arrangement fee.

– Unfortunately I no longer have any ‘earned income’ (living off investment income/return – for now), hence I no longer have access to any retail offset mortgage products. Is anyone aware of offset products with private/offshore/other banks who would lend with no earned income (but good investment income) please? Coutts have an offset product, however they still charge 25% of their extremely high offset mortgage interest rate even if fully offset, making a standard mortgage for the full amount not much more…

– The above might be worth considering for your Dream House too.

– Lastly, consider buying a ‘self driving’ car (Tesla) or one with ‘active lane centering’ (most new premium cars now have it as an option) to make your journeys down there a breeze… This really is a game-changer for regular long journeys. Be careful to research which actively keep you centered within the lane, not just ‘lane assist’ which only acts like side bumpers in kids bowling.

None of the above is advice of course…

Enjoy the new pad!

LikeLiked by 1 person

Many thanks B.

I love that tiny.cc/ibmargin link – very helpful – my blog readers heard it here first. Thank you!

I think your point re the interest rate not being the only factor – and higher rates being a price worth paying for greater certainty – is a good one.

I am giving some thought to expanding my (currently very small) mortgage on a BTL property. My mortgage rate on that is similar to that of the private bank, but the risk/repayment profile is obviously very different. And that mortgage is tax deductible, albeit only at basic rates, unlike the private bank’s portfolio finance facility. However there is work/admin/hassle in expanding the mortgage – including a revaluation of the property – whereas one thing I really love about the margin loans is how simple they are to access/arrange.

LikeLike

Reading this makes me realise … I’d love to hear what someone like you gets out of your private bank .. (and how much you have to pay them for the pleasure…)

LikeLike

Thanks for sharing the level of details and congrats on the new home!

Would love if your next post would Center around your asset mix over time with some commentary.

I will close on my first investment property soon and it will significantly alter my asset mix towards RE and make me a net borrower for the first time in my life which is something I still need to wrap my Head around…

If it’s not too much to ask 😉

LikeLike

I have covered my asset mix over time, over time.

My Investment Policy Statement shows where it has ended up, but also a change log of each material change. https://firevlondon.com/my-investment-policy-statement/

One of my original posts on the matter: https://firevlondon.com/2015/06/30/my-ips-4-of-5-target-allocations/

Then this key change at the start of 2016 as I bought my Dream Home. https://firevlondon.com/2016/01/24/housing-pt-10-stress-testing/#more-1450

And this 2017 post provides more commentary https://firevlondon.com/2017/01/27/updating-my-target-allocation/

LikeLike

Congrats!

Well I fretted and fussed at the time of your Dream Home v1.0 leverage, and that worked out spectacularly, so good luck to you and hope it works that well again! 🙂

It’s funny how the spectrum of risk works — a bunch of my readers think I’m crazy with my interest-only mortgage, but if the Marvel movies have taught us anything it’s that there’s always a bigger badder take on everything out there 😉

You obviously have way more experience of margin now than most of retail investors/commentators, and certainly me! But please — as others have alluded to — do keep in mind changing margin requirements at times of stress.

This is exactly what happened in 08/09 and it led to waves of forced selling for some very over-exposed big private investors. They were mostly on spreadbetting platforms from memory and that was 13 years ago, but the principle should certainly hold up again. As you know margin is there to protect the lender, and if it believes/models risk (/volatility) is up it will want more protection (maybe even it — look what happened with RobinHood et al and their clearance houses et cetera.

That will almost always happen at times of dislocation which equals downturns in markets. Even if you can sell other stuff to meet the calls, do you want to be a forced seller?

Personally, I’d consider getting a bit of a mortgage… heck it’s still ‘free’ at the moment, inflation is paying it for you! 😉

Okay, I’m at it again. I should really be totally deferring to you on this! 🙂 But anyway, that’s the sort of thing I’d say to you in the pub. And I know you’ll have thought about it all anyway.

Enjoy the views! 🙂

LikeLiked by 1 person

Sorry, slight garbling — I meant even mighty Interactive Brokers might be forced to change margin requirements due to what its own market partners demand/mandate.

LikeLike

Interested to know what changed your mind about a second home given your previous post on this…?

I sold my second home in the US in 2020 after 16 years of ownership. Whilst we enjoyed staying there our usage reduced to the extent that it just didn’t make financial sense having capital tied up there plus the annual OPEX overhead and administration time spent to keep it for the period we were there each year. Plus, we felt obligated to go there given the ongoing financial commitment but also wanted to travel to other places which became challenging given the limited free time available each year. We miss the place but don’t regret the sale.

The bottom line in terms of justification (for me) is usage. If I am spending so much time there that it’s cheaper to own it makes sense, if not it isn’t.

LikeLike

Yes I worry about the ‘feeling obligated’ dynamic. That has always put me off owning a 2nd place, whether abroad or in the UK.

What has changed my mind is, in a word, Zoom. I think I can work at least 2-3 days a week from ‘anywhere’ in the future world, and that in that case I fancy having a change of scene.

Another factor is that I have always thought ‘rent, not buy’ for such fripperies. But in practice the area we like does not have very good ‘rent’ (hotel, or nice homes) options.

LikeLike

Congrats! Enjoy it. One of my regrets was not buying London property in 2014 when I visited for Wimbledon. That would have been a nice investment!

But we did buy another home in the summer of 2020. Feels great to make money and enjoy your investment.

Sam

LikeLiked by 1 person

[…] about margin? Some gung-ho sophisticated investors use margin debt from a broker to fund property. The risks are magnified because unlike with a mortgage, margin debt […]

LikeLike

[…] about margin? Some gung-ho refined traders use margin debt from a dealer to fund property. The dangers are magnified as a result of not like with a mortgage, […]

LikeLike

[…] about margin? Some gung-ho sophisticated investors use margin debt from a broker to fund property. The risks are magnified because unlike with a mortgage, margin debt […]

LikeLike

[…] about margin? Some gung-ho sophisticated investors use margin debt from a broker to fund property. The risks are magnified because unlike with a mortgage, margin debt […]

LikeLike

[…] given that I have just bought a Coastal Folly, there is clearly an argument (made particularly by Mrs FvL) that I have taken a giant concrete […]

LikeLike

[…] the meantime, my expenses have skyrocketed, with the Coastal Folly needing all manner of ‘investments’. Beds, new car, furniture, gadgets, etc. These are […]

LikeLike

[…] about margin? Some gung-ho sophisticated investors use margin debt from a broker to fund property. The risks are magnified because unlike with a mortgage, margin debt […]

LikeLike

[…] because I keep raiding it for whimsical house purchases (see previous posts such as this one and this one), tax payments and such like. But assuming I avoid any more dramatic raids on the portfolio, […]

LikeLike

[…] to USA equities. But what will be will be. I am as well positioned as I have been since buying my Coastal Folly at the end of 2021. […]

LikeLike

[…] December 2021, I borrowed about 25% of my portfolio’s value to buy my Coastal Folly. I targeted reducing this to a 20% ‘loan-to-value’ (LTV) as soon as […]

LikeLike

[…] means I consider that the extra leverage I took out to buy the Coastal Folly has now all been repaid. Thanks to interest rates jumping up in 2022 and stock markets taking quite […]

LikeLike