Well, what a month.

The October bloodbath resumed in December, and then some, after a brief November hiatus. US stock markets fell by over 9%, just in the single month. Even Donald Trump has subsequently conceded that stock markets “hit a glitch”.

Given the reality TV show that is the Trump presidency it is hard to say exactly which news story drove such a drop, but you can take your pick from:

- Trump attacking the Fed – which calls into question American economic governance.

- The ongoing ‘trade war’ between the USA and China.

- The government shutdown in the USA, due to the standoff between Trump and Congress over the $5bn border wall. This has resulted in hundreds of thousands of American workers not being paid/not working; I am never clear whether, if the shutdown stops, they then get backpay, so I’m not quite clear how severe this actually is but it clearly can’t be good.

On top of the Trump nonsense, I think that we saw the first rumours in December of a more significant slowdown in China. As 2019 started Apple shocked markets with (slightly Polyanna-ish) tales of Chinese woe.

While UK news was feverish about the inability of the Tory government to pass its EU Brexit deal through parliament, this had very little discernible impact on UK markets; I tend to agree with the commentators who say that this outcome was ‘priced in’ (i.e. expected) by the market already.

Bonds actually had quite a good month. I’m not particularly sure why though I think that the climate of rising rates and ‘flight to quality’ both probably helped.

For my portfolio, December was brutal. Stocks in my portfolio that dropped in price by 12% or more included: retailers Next, Inditex, SCS, and Tanger Factory Outlet; as well as manufacturers/engineers John D Wood, Alumasc, Babcock, and US bluechips WFC and XOM, I also took significant hits on EMR, AMZN, JPM, and a host of others.

Gainers were few and far between. The most notable for me is an illiquid Private Equity fund that my private bank has got me into, which allegedly went up 11%. Mining stocks rose too, and after the builders’ bloodbath last month Berkeley Group, in particular, rallied 8%. But these were crumbs of comfort.

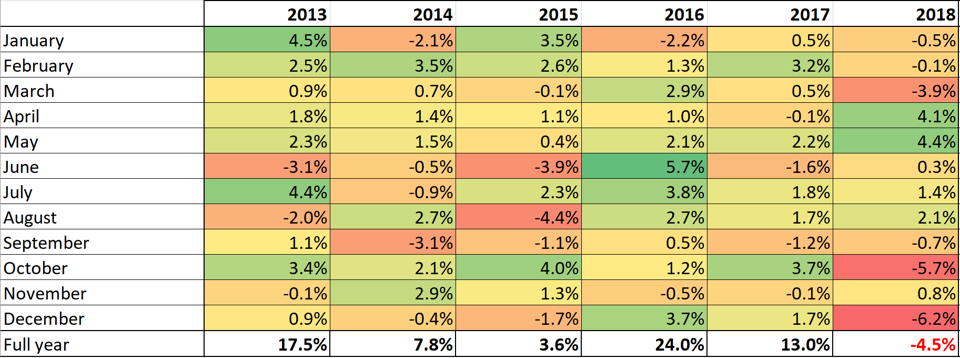

Given that I remain somewhat leveraged, in theory I potentially get especially clobbered by market drops. In practice my portfolio almost exactly tracked the market in December, dropping by just over 6%. In the month. As my heatmap below shows, this was the worst month since I started tracking this stuff properly six years ago.

Last month, and moreover last quarter, have turned 2018 into the first clearly down year since my tracking began. It wasn’t looking too bad as late as September, and even now the fact that six months of 2018 saw falls isn’t that unusual (compared to five in 2015 and 2014 for instance). But a balanced portfolio dropping by over 5% twice in three months is pretty unusual, to put it mildly.

Looking into what rose/fell in 2018, the short answer that the best place to have been would have been in USD, in cash. And the UK, or UK equities in particular, was among the worst places to invest. With interest rates rising to around 3%, and the currency gaining 6% against the pound, your pounds could have had over 8% return by moving all your money into USD at the start of the year. Almost any other approach saw you lose money last year, especially if you were long in equities as I have been. But even as an equity investor, the USA was the place to be, Trump notwithstanding.

Taking a step back, my annualised returns since inception (1/1/2013) have dropped to slightly below 10%. Per year. This definitely isn’t the end of the investing world as we know it. We’re back where we were in around mid 2017, i.e. we’ve lost 18 months.

But beyond the investment returns per say, I had set myself three goals for 2018. How did I do?

1. Reduce taxes and expenses.

My 2018 objectives were to get my investment tax rate from 30% to below 29%, and reduce average expenses rate from 0.65% to 0.60%, a drop of 5bps.

What’s happened? Well, the big move here was redeploying the windfalls I received in Q2 into low-tax/low-fee places. Mainly as a consequence, my expense rate has dropped by 14bps; alas I think my measurement is not consistent with 12 months ago but I make the current blended (across both my and Mrs FvL’s accounts) expense rate 0.61% (0.18% excluding my private banking account). And my investment tax rate has dropped to 28.8% – this is a clear WIN.

2. Maintain my (slowly deleveraging) allocation.

I wanted to get my leverage down below a cash allocation of -20%, and I wanted to stick within my ‘tramlines’.

Thanks, again, to the windfalls, I sailed past my leverage objective in Q2. Since then I have been releveraging a little, and of course markets have fallen which increases my leverage. But I finish the year with my cash allocation at -19% of my invested portfolio (excluding Mrs FvL, which has no leverage). I’m ahead of target, by a bit. One additional factor, which is not tracked as part of my invested portfolio, is that I have been making some mortgage repayments (against interest-only mortgages); if I had instead used these funds to reduce my margin loan I would be at a cash allocation of -18%.

As to my tramlines, I finish the year with only one of my cells adrift by more than 1% of my portfolio value. I didn’t define exactly what success feels like here but I am OK with this performance; I have been trimming the sails regularly and reinvesting income almost exclusively towards the underweight exposures. I call this a WIN too. The only slightly amber cloud in this sky is that, after December’s dramatic drop in equity values, my *total* fixed income allocation is too high by 2.5% of the portfolio.

I grade this goal a clear WIN.

3. Learn something new.

This time last year, I deliberately avoided committing to a goal of reading more books, fearing the worst, and went for the more-achievable-sounding “learn something new, that I can put into practice with my investing”.

A year on, I cringe as I try to hold myself accountable to this goal. I think I have learnt quite a bit this year, but I struggle to summarise any of it here.

Yes, I’ve learnt about some new companies, I’ve seen the value in getting outside my usual media bubble, I’ve learnt stuff from my blog commenters like @zxspectrum48 and @grasmi, and I’ve built further evidence for my investing track record both on this blog and as an angel investor. All of which makes me wiser, more experienced, and probably more learned. But I am somewhat short of crisp lessons I can repeat here.

Sadly, the most pertinent lesson for me in 2018 was what I learnt from a close friend’s demise in his early 50s. His death, and the hopes/plans of mine that it has dashed, has made me reconsider my chances of not making it another 10 years. This, along with the complexity blog post I wrote and its comments, have had me start seriously appraising my ‘wind down mechanisms’. That rather morbid lesson is definitely not what I was expecting a year ago, and that is my main lesson from 2018.

“it is hard to say exactly which news story drove such a drop”: nobody knows what exactly caused the Wall St Crash of 1929, and people have been studying that for decades. The “this caused that” fluff about stock market levels is mainly journalistic entertainment: nobody knows. Nobody can know. In all likelihood nobody ever will know.

It might be reasonable to say “I shall explain to you why I think the US stock markets are overvalued”. It might be reasonable to say “Therefore you would be wise to plan for disappointing returns for the next decade or so”. Beyond that all is murky.

LikeLiked by 1 person

Given how long of equities you were, I think you came out of this well. 2018 was the mean-reversion of 2017. In 2017, virtually ever asset outperformed US$ cash; in 2018, virtually every asset underperformed. “Trump pump” to “Trump dump”.

Looking at your returns since 2013, what stands out is how little volatility there is given the concentration to equities. QE = financial repression = low volatility. At the Fed FOMC meeting in Dec, the moment they implied the balance sheet run-off would continue, the S&P dived. It wasn’t perturbed by the hike but it doesn’t like Quantitative Tightening at all. It was equally noticeable on Friday that the S&P loved the softening of Powell’s language on that.

You say your returns are 9.8%/annum since 2013. It might be interesting to look at your returns in US$. Measuring returns solely in the currency of a country with the strategic aim of being the next big emerging market may be giving you a false sense. Happy new year.

LikeLiked by 1 person

Zx48k… Thanks. In terms of US$ returns, the calculation is pretty simple. The pound has dropped from $1.61 to $1.28 since 1/1/13. My annualised return is 5.6pc in USD over that period. Much less good I grant you but certainly a decent real (above inflation) return.

LikeLike

I take a slightly different approach to measuring true performance due to my portfolio being invested in a range of global companies, even if it is sterling denominated. I just use the MSCI world Net index in GBP as the equity benchmark so it gives a true picture of performance. Last year the equity portion of my portfolio was +3.86% vs -3.1% for MSCi so safe to conclude the outperformance was not due to currency effects. Fundsmith also use the same approach.

LikeLiked by 1 person

Lemsip, your approach works well for equities, provided you are happy to have zero home bias. I do deliberately have home bias though. And for non-equity holdings you need a different approach. Bonds are a very different type of risk. My approach tries to give me the flexibility to flex my allocation both geographically and by asset type. I do agree though that the msci world net index and its ilk are good comparison points for me and all of us.

LikeLike

FIRE v London fair enough. Given global bond yields and the interest rate environment, my bond allocation has been limited to very short term cash equivalents. I am in the Buffett camp where I think adding longer term bonds is likely to increase rather than decrease overall risk at these levels. Certainly just maintaining a cash and global equity profile has worked out OK so far – albeit some of the volatility can be interesting in the short term. Obviously keeping cash produces its own conundrum about currencies so no easy answers anywhere ! Re: home bias, it is unavoidable on the expense and asset side of the household account but I do make a conscious effort to keep allocations global on the equity side.

LikeLiked by 1 person

2018 was an investment education for a lifetime.December, October and February felt brutal in real time but I ended the year +3.6% with a 90/10 equity cash portfolio with no bonds. What worked was a large allocation to defensive US equities that kept their heads above water. Interestingly switching to traditionally ultra defensive options ( like lifestrategy 20/80) or 100% cash at the beginning of the year would have been worse. As it turned out it was the most stomach churning year of my investment experience but the overall performance ended up being marginally better than 2015 !

LikeLiked by 1 person

[…] Firevlondon reviews the whole of 2018 with their December update (38) […]

LikeLike

Happy new year FvL.

Your chart of monthly returns is instructive.

I recall 2015 being quite a rollercoaster year for returns. The earlier commentary this year about “the longest bull market in history” seemed to have erased many of such halcyon days since 2008.

So I’d quite expect in 2021 we will have forgetten this “market turmoil” (urgh). We’ll be left with just the artifacts in our spreadsheets. Plus ca change.

LikeLiked by 1 person

[…] v London’s monthly scorekeeping does a good job accounting for foreign exchange movements between the currencies he invests […]

LikeLike