What a brutal month. We moved from ‘crumbs, Italy’s borders are shut’ to ‘whoa, we’re all under house arrest’ in only a few days. The start of March is hard to remember.

I’m glad I managed to get a few days skiing done earlier in the season – now I have three overseas trips cancelled and don’t expect even to leave London for potentially months.

As lockdown loomed, I found myself shocked to be asked “are you staying in London? Or getting away?” by several people. OF COURSE I’M STAYING IN LONDON. In my Dream Home, silly. In fact some friends who had decamped to Cornwall have recently returned to London saying they really hadn’t appreciated how much better to be marooned here than there.

Market meltdown

But turning to the markets, they have had an absolute whipping this month. The fastest decline ever. And, wow, the volatility. Normally liquid ETFs had pronounced spreads, and one of my online brokers resorted to manual trading on a frequent basis. Yet, with all said and done, the damage isn’t yet quite as bad as it feels.

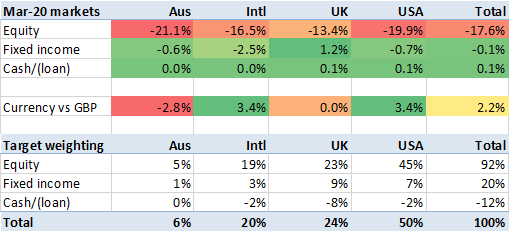

Having caught a cold in February, world markets developed a very nasty flu in March. All equity markets fell. And fell very rapidly. Equities were down around 18%, across the piece.

And while FTSE’s fall, of around 13% (from around 6500 to around 5600), doesn’t look as bad as overseas markets, the pound was falling over 3% against Euros and USD. So measured in foreign currency, there wasn’t much in it between the Eurozone, the UK and the USA. Only Australia did worse – as its stock market (or share market, as they call it) fell over 20%, the AUD fell nearly 3% against the GBP too.

Bonds were a relative safe haven, though it varied by geography. Treasuries/gilts did very much better than corporate bonds; thankfully I have been steadily shifting my fixed income holdings towards (long dated) gilts and away from corporate bonds, thanks to Monevator’s posts (like this one and this one), which I was grateful for in March.

Overall, markets fell over 16% in local currency terms. Overseas currencies appreciated, in my basket, by over 2%, leaving the world markets that I’m exposed to down almost 15%. Against that backdrop, my portfolio’s drop of ‘only’ 12.5% was significant outperformance.

The complexity of mayhem

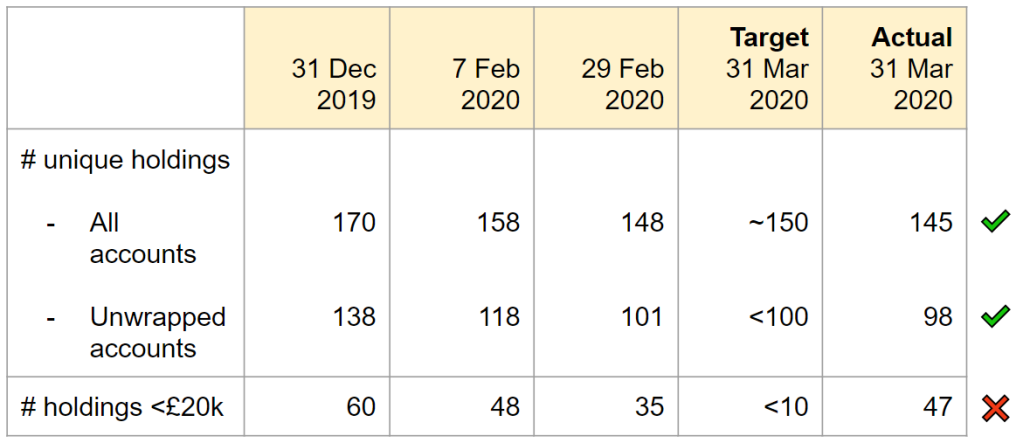

I’m not sure why I ‘outperformed’, but I know that I was very busy in March. My complexity reduction activities went backwards, with many positions falling below my ideal minimum holding size of £20k. I was trimming/nibbling at my positions almost every day – as recorded on my Diary and in this blog post.

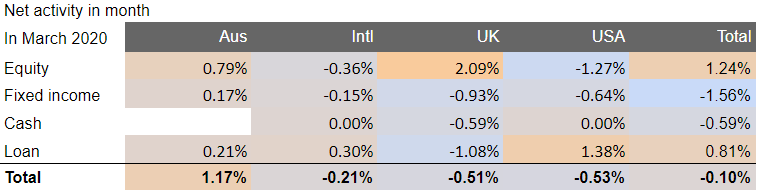

My activity in the month covered almost 100 holdings, and is summarised in an ‘activity matrix’ below. This matrix shows that I purchased, net of sales, UK equities worth more than 2% of my portfolio. I sold, net, fixed income worth over 1% of my portfolio.

Most of my trades were small, nibbly ones, but against two clear objectives.

1: Rebalancing to sell high, buy low

Firstly, I was rebalancing out of Fixed Income (which did absolutely OK, and relatively very well), and to a lesser extent out of US Equities, and into Australia (the most badly performing geography) and into UK equities (where I have been structurally underweight). I now own 10% more GOOGle shares than I did a month ago, 25% more MSFT, 25% more Rightmove, and significantly more Australian ETFs. I own significantly fewer corporate bonds, and bond ETFs. I no longer own any Cisco or Archer Daniels.

2: Managing my leverage

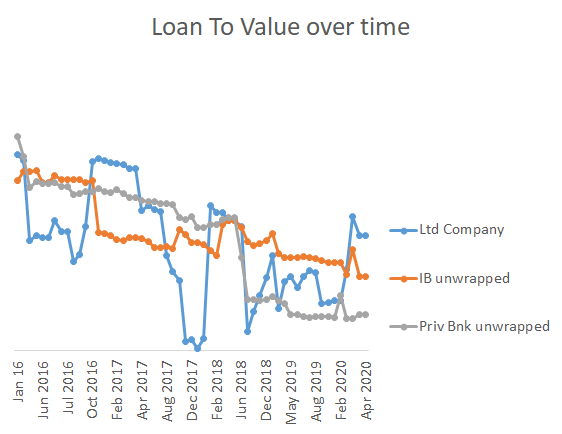

Secondly, I was managing my margin loans carefully. I brought most of the loan back into GBP, as having loans in appreciating foreign currencies is nerve-wracking (even if they are more than covered by my foreign asset exposure).

I also trimmed my leverage mid month. My leverage had spiked up mid month, to levels I last saw in 2017. Not only was the value of the portfolio falling, but in my Interactive Brokers (IB) accounts I was buying (falling knives) using margin. I decided to brace for further falls – something that involved me selling small amounts of some great businesses, like Amazon. As yet those falls have not yet come, but I am relatively well prepared if they do.

And so, to bed

The final week of March saw relative calm in the markets. I finished the month with my allocation close to my target, across both asset types and geographies. I am, deliberately, slightly underweight equities, and slightly overweight Fixed Income. If equity markets fall further, as I suspect they will, I am less exposed; if they gain, they will bring me into balance. ‘Market timing’, if you will – or risk management, amateur style.

We’re now on the cusp of my favourite point in the financial calendar – the start of the new UK tax year. If you haven’t maxed out your ISA allowance for 2019/2020, you have only a few hours left to do it.

Thanks for the update

Out of interest why you so keen on Australian assets at the moment? The country highly leveraged to China, corporate and household debt levels very high and the economy was hollowed out in recent years due to the mining boom and high AUD, and yet to really recover.

Over the medium term I would think Australian assets would be a sell, interested in your thoughts!

LikeLike

I am not making a particular play on Australia, only that my target allocation has a particular weight to Australia (where I have family) and I want to stick to my allocation. Overall I think it is at least well (economically) governed as UK/USA, and arguably Eurozone, so I wouldn’t reconsider my allocation downwards.

LikeLike

Interestingly, the Australian market is the best performing over the past 120 years…

Enjoyed the update. So glad you got that leverage down in good time. Imagine if all this had happened between the property sales. :-\

(Sure you would have survived, but perhaps with more grey hairs? 🙂 )

LikeLiked by 1 person