Boris is bashing the pound, Trump is bashing the global economy. Who’d invest in anything, in this environment?

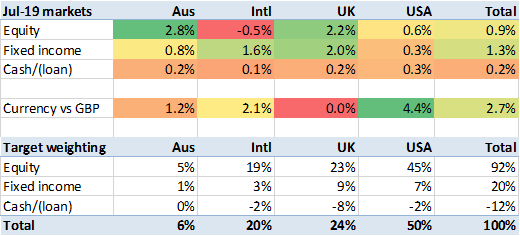

Well, when the Brexiteers pummel the pound, us globally diversified investors tend to do alright – provided we measure our progress in pounds! And FTSE-100 does alright too. This month was no exception; the GBP fell over 4% versus the USD, and FTSE rose over 2% partly as a consequence.

Bonds went up too, particularly in Europe (inc UK, obvs) – for reasons I’m not sure about.

Elsewhere was a bit more of a mixed bag – Oz equities steamed ahead, European/Asian equities sagged, the US shuffled forward.

Currency movements alone moved the markets I’m in up 2.7%, in GBP terms. Though the UK FTSE rose over 2%, my UK equity weighting is relatively low, so the diversified markets I’m in rose ‘only’ 1.1% in their local currencies during July (more thanks to bonds, than equities!). Combining the two effects means my market benchmark was a gain of 3.9% in July. Such months don’t happen often.

For the record, and despite my ‘what am I doing? nothing’ post a couple of weeks ago, I have made a very tiny tweak to my portfolio allocation – to reduce my target equities exposure by 1% (93% ->92%, UK equities 24%->23%), and my gearing by 1% of the portfolio (i.e. a relative drop of almost 10%, from 13% to 12%).

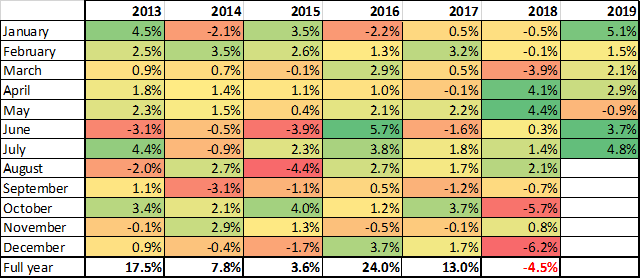

How did I do, with markets rising almost 4%? In fact my unitised return was a gain of 4.8%, in one month. That’s the third best month since I started tracking monthly gains, 67 months ago.

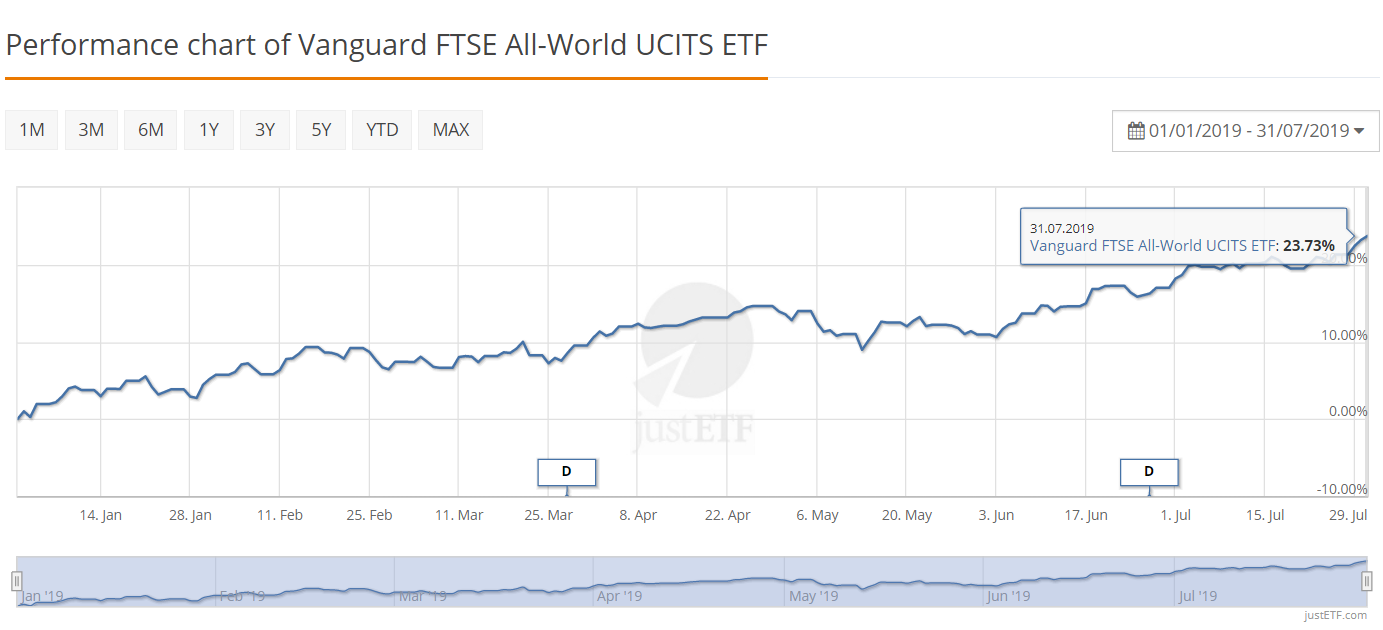

World equity markets have risen almost a quarter this year so far (see chart below). The US global bond aggregate has risen 12% too. What a year to be alive.

[…] And a July progress report (36) […]

LikeLike

The problem is those nice returns are not happening for the right reasons. First, you’ve got positive returns from a weaker GBP. Yes, your foreign assets grow in size but what about your liabiltiies? Once you measure your net worth in a hard currency (say the USD) things don’t look half as pretty.

Second, why are those bonds rallying so hard? A bond market rallying (and the yield curve flattening) means lower inflation expectations and lower real yields. German 10-year bonds yield -0.50%, the 30-year -0.01%. The market is saying the average rate for the next 30y will be zero. That means secular stagnation, ‘Japanification’. Low growth forever. Yes, you get a positive return now, but all you’ve done is PV upfront the gains for the next 30 years. That ain’t anything to be happy about.

Third, the stockmarket. Are these returns coming from great earnings, higher growth or higher productivity? Absolutely not. It’s coming from lower expectations for policy rates from the Fed, ECB, BoE, BoJ (and they are cutting because they are worried about global trade and sentiment) and the end of QT and possibly more QE. So short-term, yes, the stockmarket junkie gets another hit of stimulus to keep the high going. But, honestly, how is that going to end? Equities are also just another asset getting that tailwind from lower long-dated bond yields. Those long-term discount factors are not just going to 1, some are now above 1! This means a Euro in 10 years time is worth more than a Euro now. More PVing upfront of the next few decades of returns.

LikeLiked by 1 person

a very gloomy view, I must say, @ZX48k! But yes I see your logic. But Moore’s law hasn’t disappeared entirely either and so economic progress will continue, somewhere, at some price. Japanification will not become a global permanent phenomenon.

LikeLike

The suggestion that markets price 30 years at a zero return, is not exactly telling us much about the next 30 years….it tells me a lot about the mood now.

1981, 30 year bond yields told me nothing about what the next 30 years would be like ! It told you a lot about the mood though.

LikeLiked by 1 person

@ZX

What does your portfolio look like in light of the above situation? How are you investing new money?

Would you borrow (or short) to invest given that interest is close to zero for 10/20/30 years?

The world seems to have gone mad and I’m interested in risk management and also profiting for the situation if at all possible.

B

LikeLiked by 1 person