Life somewhat returned to normal in June.

By normal I mean the tariff war resumed, Brexit chaos continued, European political dysfunction filled the newspapers and so forth. The US and Europe now have tariffs against each other on steel and Harley Davidsons. But more dangerous escalation looms – with Trump clearly gearing up to impose tariffs on German European cars.

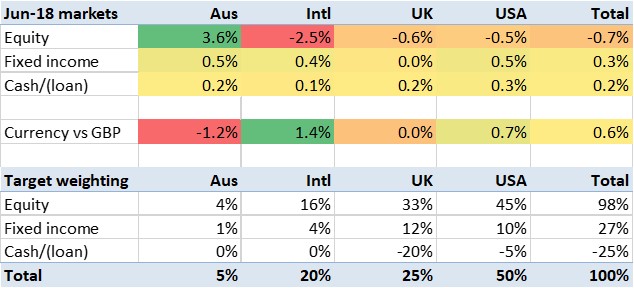

From a market point of view the big loser were major exporting markets. In my world, this meant ‘International’ equities, which lost 2.5%, even as the Euro rose a little against the pound. UK/US equities dipped slightly too.

On a much brighter note, Australian equities jumped, which I think was due to large electoral bribe tax cut passing both houses of parliament. Bonds rose slightly, in line with their long run average.

The second windfall that I was expecting in June still hasn’t arrived. Just as well I hadn’t spent it yet; even with ‘liquidity events’ the liquidity can feel like treacle, not water.

So, in a world which fell a little in June, I was happy to see a blended increase of 0.2% for my portfolio as a whole. This leaves me up almost 9% in Q2, and 4.1% for the year to date. What a difference a quarter makes. I’m still closing in on my first ‘double’ since my monthly tracking started in January 2013.

As it’s the end of a quarter, it is high time I reviewed my progress against my 2018 investing objectives. However, with a significant windfall yet to hit my account, this actually isn’t the time. All I can say is that my objective of learning something new is currently a Fail; I have some professional learnings to credit but I don’t yet see a read across to my portfolio management strategy. Worse, I don’t have a clear plan to achieve this goal. I suspect I will be taking a Charlie Munger reading list on holiday in a month or two, if I can’t think of something better to do.

[…] Firevlondon reviews June’s finances (27) […]

LikeLike