So, for the avoidance of doubt, the end of the month is the last trading day of the month. Which for February, meant Friday February 27th.

The fact that the Israelis and the Americans invaded Iran on February 28th is going to impact March, not February.

Which is just as well because I had quite a lot of activity in February.

Simplifying the portfolio, pt3

While the weather in the UK was pretty unremittingly miserable, I found myself rearranging quite a few of the portfolio’s deckchairs.

One of my longstanding and most thoughtful readers made a comment on my blog recently that resonated with me. @Grasmi is a Brit who has emigrated abroad – to Australia, so far as I can gather. He is a bit further ahead of me on the path to portfolio enlightenment, and here is what he said:

I vastly simplified my portfolio years ago. I’m down to 8 positions now (7 ETF’s and BRK – so basically 8 ETFs). Never looked back. Less levers to pull = less stress and “busy work”.

After doing the cleanup a long time back, over time you basically “can’t” fiddle any more due to CGT… which is a lot of ways is quite freeing. There’s always a temptation to do something, but once you’ve got large accumulated CG’s in a simple portfolio, that urge goes away. Any change you make needs to make back the cost of any CGT bill (for me this is 20-30%+) just to break even, so I’m very reluctant to make any changes.

Longtime readers will know I went through a concert effort at simplification back in 2020. What I’m left with is about 90 unique holdings held across 9 brokers (6, really; 3 of them are offshore bonds/equivalent that I barely touch and don’t need to file tax reporting on). As at the end of 2025, only 64 of these holdings were in unsheltered accounts – i.e. accounts that need tax filing.

But there is a hidden layer of complexity I haven’t dwelt on before: duplication. In the six brokers that I actively supervise, there are 85 unique holdings. But there are 215 actual positions, meaning my average holding is held 2.5 times across various accounts.

I have ISAs with multiple providers. I have two SIPP accounts, both with brokers who also have an ISA and a GIA. And I have subaccounts with three brokers – for instance my ‘property proxy’ account I have been using since late 2024. Overall I have 25 accounts across these brokers.

What then happens is in most of my accounts I try to have a diversified portfolio. And for that, I want exposure to the 8 geography/asset classes that make up my target allocation. Some of my accounts have significantly more than 8 things in them too, because for instance I might have half a dozen favoured UK equities or US equities in them.

Some core holdings such as VGOV and SAUS end up in numerous accounts. VGOV is in seven separate accounts, providing monthly dividends that are useful to lubricate each account but which, for the GIAs, all need to be filed on the tax return. And even the unreportable ones in my ISA and SIPP end up being logged in my tracking system. Six accounts with monthly dividends is 84 records made in my spreadsheet/trackers. For one holding: VGOV.

In fact I have almost 50 holdings that are held at least twice. That leaves about 40 holdings that I hold uniquely in one account; this includes about 6 single line government bonds (which are 6 holdings).

What does good look like?

As it happens amidst this clutter and duplication, I have one account which is (almost) the model of simplicity. It has VGOV in it, at exactly a 20% weighting. The other 80% is in the S&P500 as an ETF. Actually not one ETF, but two – reflecting me starting off with one but then realising it was a synthetic, and I have slowly been sliding into a better ETF – without crystallising too much CGT in any given tax year. But that is it. Three holdings, two underlying exposures, a nice clean 80%:20% mix to it.

Can I throw a few deckchairs overboard?

So, I’ve resolved to declutter my duplication significantly.

However, as @Grasmi points out, one quickly hits a real world obstacle in the unsheltered account – capital gains tax. After crystallising a couple of holdings in February, my position is now that, with the exception of a few bond ETFs, every single holding in my GIAs is sitting a significant unrealised gain. So I can’t readily throw these deckchairs overboard without a real cost incurred.

But that leaves my tax sheltered accounts. Here I can trade as much as I like and I am not incurring capital gains tax at all. So it is here that I have started.

My initial aim is to reduce each tax sheltered account to only having one fixed income holding in it. Also I am trying to reduce the number of equity holdings in each account; I do not need Australia plus International plus USA plus UK holdings in each account.

(Equity + Fixed Income = Total # of holdings)

Account

Account 1 (Mrs FvL)

Account 2 (Mrs FvL)

Account 3 (Mr FvL)

Account 4 (Mr FvL)

Account 5 (Mr FvL)

Before

4 + 1 = 5

9 + 7 = 16

10 + 9 = 19

6 +2 = 8

7 + 5 = 12

After

3 + 1 = 4

8 + 5 = 13

9 + 8 =17

3 +1 = 4

6 +3 = 9

You might well think that the After column isn’t a lot better than the Before column. All I can say is that I did enough trading here that one of the brokers proactively emailed me to check whether all was OK.

After what seemed like a lot of activity, I could argue that two of the five tax sheltered accounts I took the shears to are now acceptably complex – with one Fixed Income holding and three Equity holdings. I am going to leave ‘account 3’ as it has quite a lot in it and several of those holdings are unique. But I clearly have further to go with Accounts 2 and 5.

Sadly my overall complexity metrics haven’t moved much here. I still have almost 90 unique holdings. My tracking spreadsheet has about 10 fewer lines in it, and my dividend reporting has become considerably a little bit simpler. But for all the actiivity, I don’t have a lot to show for it at the moment.

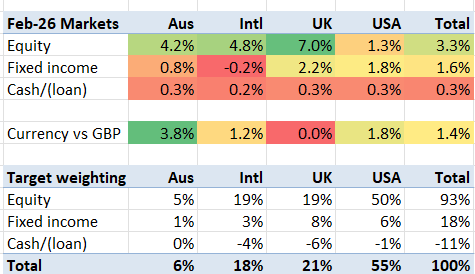

Good month for non-US markets

Meanwhile, beyond my portfolio, the markets had a generally strong month. The pound fell, which probably helped FTSE-100 deliver a 7% gain and nearly hit 11,000 – just a few weeks after it breached 10,000 for the first time. But other markets did well too – except for the USA. But even the US stock market rose about 1%, slightly less than its bonds delivered. The overall markets I’m in rose 5.7%.

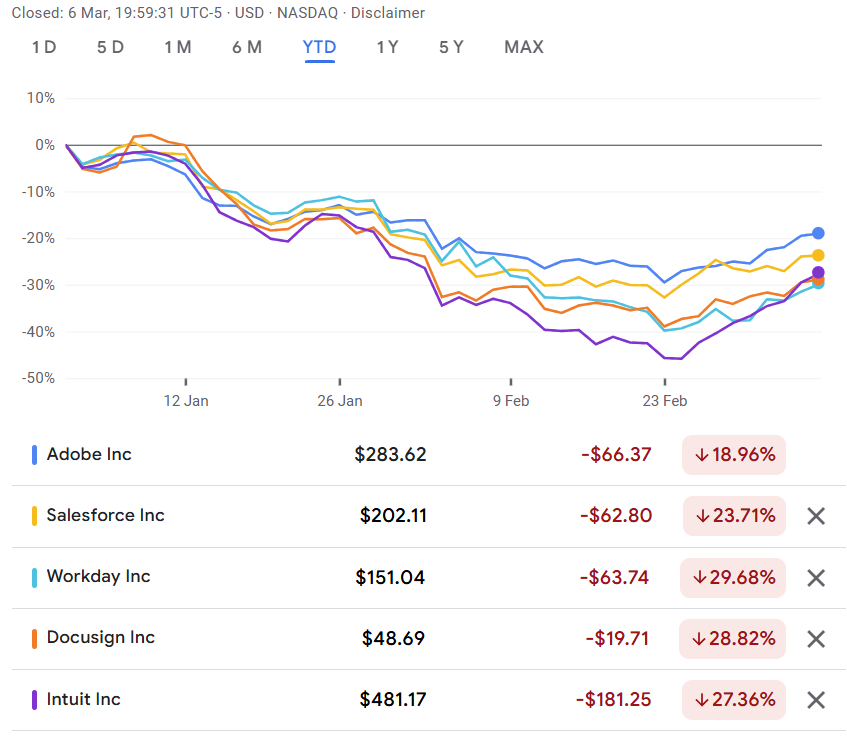

That all looks reasonably benign, right? What you don’t see in the above is any trace of the SaaS-pocalypse / SaaS-acre / SaaS-mageddon – take your pick. For those of you not following the tech/software space, it is has been brutal this year. The chart below shows a random set of example software businesses, all of which have fallen 25-45% this year.

Much of the damage is blamed on Anthropic, whose Claude tool (and its newest variant Claude Work) supposedly gives users the ability swiftly to replace swathes of established software businesses. I do know of entrepreneurs who are replacing software tools (CRMs and employee/customer satisfaction tools, chiefly) with Claude/similar-built replacements but I believe the market is overselling the worry. XRO is down over 50% and I don’t think 50% of its users are going to build their own accounting package. Another example Docusign is down >80% from peak; while its core functionality may be easy to replicate, anybody who has used one of its competitors knows that Docusign’s proposition is considerably more sophisticated than its simplest ‘happy path’ and I suspect Docusign’s business is more resilient than the bears fear.

Relatively poor month for my portfolio

In any case, this defensive commentary on the ‘SaaS-pocalypse’ is another way of saying that my portfolio badly lagged the markets I’m in last month. Small positions in Xero, Adyen, Wise as well as large holdings of Google and Amazon dragged me down. I also don’t have much exposure to the ‘SaaS-proof’ winners of the last month, such as consumer businesses and extractive companies. So my portfolio rose ‘only’ 2.6% in the month.

My income/dividend picture has been fairly disappointing in the couple of months too. I haven’t got all my dividend reporting yet but I appear to be running about 20% down Year to Date on 2025, and lower than I’ve had for the first two months of any year for over 10 years. Hopefully Match will see some catching up!

It’s easy to underestimate the benefits of simplicity isn’t it? Last year I created a more comprehensive “death box” for my partner in case I died, and although that’s unlikely, documenting every account, holding, rental properties, tax implications, etc created what inadvertently became a checklist to simplify. I thought my finances weren’t too complicated, but when looked at from the perspective of my partner taking it all on, I realised changes were needed that are already benefitting me. I’m on a mission now to simplify further.

LikeLiked by 1 person

Firstly, thank you for the kind words. I think I probably topped out at around 50 holdings when I was “dabbling” (mostly to add negative alpha, it must be said!). Just reading about your accounts / positions makes my head hurt!

My next biggest planned simplification comes from selling my EC3N London flat (I hung on to it when I left London in 2013) in May when the lease is up. I got rid of another one in Australia last year (I’ve been accumulating them as I moved around the world for work). After that, it’s just my equities, my “bond tent” portfolio in Indonesian govt bonds (I’m actually living in Indonesia these days), and the house where I live (plus a few pensions). I can’t get much simpler than that. The benefit with dumping the properties, in addition to not being a landlord any more, is that I no longer have to file tax returns in those countries. At one point I was doing UK, Australian, Swiss and Indonesian tax returns (3 different tax years). It was an absolute nightmare. I’m down to just UK and Indonesian now, and after this year, I should be down to just Indonesian. Ironically, after stepping back from work, when I’ve arguably got more free time than ever, I’m more aggressively focussing on simplifying things so that I can free up my time for more enjoyable things (hobbies, etc).

The new AI LLM’s (like claude and open AI Codex) are PHENOMENALLY powerful in an IT development context (but I’m also finding AI useful in SO many other contexts too). Before I RE’d, I was a software architect in the physical commodity trading space. I’ve been playing a lot with the latest models and they are incredibly capable and competent.

There will be a lot of work to get the new models integrated into the corporate world (it won’t happen overnight), but a lot of changes will be coming. I can see headcount being reduced substantially. What the implications of that are for society as a whole is the thing that concerns me most. The counter argument is that people probably said the same very things about computers, word processors, spreadsheets, the internet, etc. and yet, here we are – people have tended to just move up the value chain (or so everyone says). The truth will most likely land somewhere in the middle and we will muddle through as we’ve always done.

I do see a potential scenario where the pendulum swings back away from large SaaS providers and towards organisations taking software systems development back in house, now that the relative cost of “developing” something will fall dramatically. This won’t be for everyone though – some organisations just don’t have an appetite to manage and own software in house, and just want it to be someone else’s problem. Interesting times ahead.

LikeLiked by 1 person

Hi FvL, I’m amazed if you have holdings such as VGOV that you don’t have significant losses with which to manage your CG position! I know I have. I’m kind of banking on my gilts to minimise any CGT when I pay off the mortgage later this year. It’s looking less and less likely that interest rates will be conducive to continuing my mortgage/leverage experiment.

LikeLiked by 1 person