Trump dominated the headlines again. This time partly due to some very biased editing by the BBC of a Panorama show about Trump before the US election.

There was also the omnipresent UK Budget. Which has had more than enough coverage. I did a ‘damage assessment‘ at the time and haven’t revised/updated my view since.

Back at home, the Christmas season started early. I found myself dining at two of London’s impressive skyscraper restaurants in one week.

I also managed a trip up to Oxford, where the Christmas lights were out in force.

Other London highlights included a performance of the Crucible in South London, and a dinner at George’s club in Mayfair.

And of course I got some time down on the south coast – including an early morning trip to Bournemouth beach!

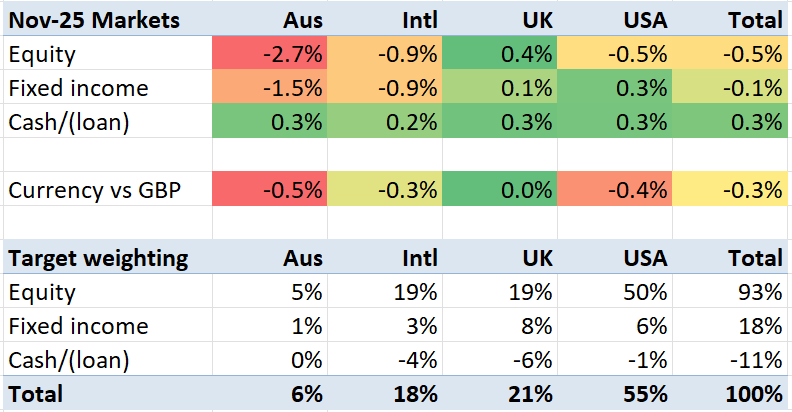

Market movements

The markets generally had a gloomy month. Australian equities did the worse. For once the UK’s FTSE-100 was the best thing to be in, especially if you were in a foreign currency.

The markets I’m in dropped 1.0% in the month, about half from forex movements.

My portfolio

My investment portfolio dropped 0.4% in the month – a fraction less than the benchmark.

But my portfolio’s big news in November was a windfall equity sale I made of a private holding (not itself part of the investment portfolio, but the proceeds are now). There will be a tax bill to pay from this but for now my ‘winnings’ are being used to pay down my portfolio loan. This actually leaves me underleveraged versus my ‘Silver rule‘ (which wants the interest expenses to be less than a third of the income in the unsheltered accounts). I will most likely need to borrow to pay the tax bill (not for the first time!) but that’s over a year away so for the moment we’ll enjoy having the lower debt levels.

Moreover my interest expenses, in pound terms (shown in the pink columns below), now are roughly what they were when I first leveraged up to buy the Coastal Folly in December 2021. My loan is a lot smaller now (back at the pre-Coastal Folly levels of LTV in fact), but interest rates are higher. The difference is that I think of my loan now as long-term sustainable, rather than a temporary loan that I would slowly reduce over time.

This means I consider that the extra leverage I took out to buy the Coastal Folly has now all been repaid. Thanks to interest rates jumping up in 2022 and stock markets taking quite a hit too, it hasn’t been entirely plain sailing. Nonetheless I have felt under control and, as the graph above shows, I managed to steadily reduce the debt ratio in a fairly consistent way even when interest expenses peaked in 2023. It’s taken four years, to the month.

Appendix: Press clippings

What a fantastic shot of the Tower of London and surroundings! You inadvertently got a picture of my London flat’s terrace (it’s a stone’s throw from the FS Tower Bridge). I left London in 2013 for Switzerland, and since moving to Asia in 2018 haven’t really been back to London very often. Your photo has brought back a lot of memories for me – it’s a fantastic area – St Katherine’s Dock, Shad Thames, etc. I used to have to pinch myself when I’d run home from the office in Mayfair – Hyde Park, Green Park, Buckingham Palace, St James’s Park, Westminster Abbey and Big Ben, London Eye, Tate Modern, a glimpse of St Paul’s across the Millennium bridge, before finishing up over Tower Bridge and then around the Tower of London. It was a beautiful run (even despite all of the tourist dodging!).

LikeLiked by 1 person

Just popping on to say congratulations – you may recall I was worried back in the day about this leverage plan, but you’ve managed it adroitly and he who dares wins, eh?

Of course this is only one run of many universes, but you still deserve your flowers 😉

I continue to think I’m a fully risk-on investor by not paying down my I/O mortgage. That’s racy enough for me…

Wishing you prosperous investing in 2026!

LikeLiked by 1 person

just on the chart, if your LTV now has dropped back to Dec 2021 levels, but interest rates are 3 or 4 times higher, how can the interest costs have dropped back to roughly Dec 2021 levels as well? Should they not be higher?

@TI is your IO fixed rate or variable? If FR, when is that running out? Reason for asking is I have to remortgage in Oct if I want to avoid SVR so it’s on my mind.

LikeLike

Fair Q

Interest expenses are 2.5-3x times higher, yes. I was paying about 1.7% (blended, across currencies) at the end of 2021 and am paying about 4.6% now.

And the total loan when I bought the Coastal Folly was 2.5-3x bigger than it now is.

Bingo!

LikeLike

@Rhino — It’s a five year fixed I/O. You commented on the post at the time! 😉

It looks like our host has disallowed links in comments but if you Google for Monevator and “mortgages and emotions” you should find the discussion.

I’m on balance happy with my mortgage as my way of levering my portfolio especially versus FvL’s marked-to-market margin loan, but it’s a personal thing and he’s provided a great template of how to do it calmly and analytically over the years here.

LikeLike

Brilliant, found it, and yes I had completely forgot that article existed. Cognitive decline no doubt.

LikeLike