I had a decent break over the New Year period, and whiled away far too much time reading blogs/etc. I felt very up to date, at the time. Now of course I can’t remember what actually happened in January – proving the point of Nassim Taleb/others.

Overall I don’t think January was that notable for world politics/markets. Davos saw the usual flurry of policy-making headlines, but nothing stood out for me.

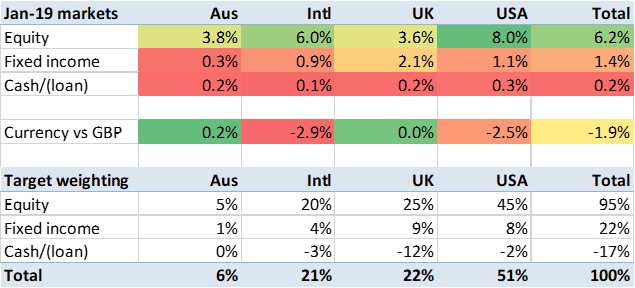

Closer to home Brexit dominated the news media, with as expected the UK government’s EU deal being rejected by a thumping majority in parliament. For some reason markets have reacted fairly favourably to these developments, I think because they appear to suggest ‘no deal’ looks very unlikely. I can’t say I am as sanguine, but in any case the pound rose to $1.33 at some point and ended the month over 2% up against the USD.

Equities recovered over half of their Q4 falls. Everywhere. Especially some tech stocks (Amazon up 13%, Facebook up 25% (!)). Even bonds rose gently. Sentiment has changed dramatically, without any particular data or hard facts to point to. Sigh.

Australia had a slightly different month. I haven’t followed it in detail but I was struck recently to discover that house prices in the two main cities have dropped ~10% in the last 12 months, with the banks/asset managers still under a lot of political/media pressure. It is really working to a different rhythm from ‘the West’ right now. Like the UK, its currency was up against EUR/USD and its equity markets rose – but not as much as where currencies fell.

Overall the markets I’m in rose over 6%. Adjusting for their falling currencies (vs the GBP), the rise was ‘only’ 4.1%’. My leverage, and my fairly strong US weighting, helped me here, as my portfolio rose 5.1% in the month. That is the 2nd best month in the 70+ that I’ve been tracking. That rise hasn’t repaired all the brutal Q4 damage, but has more than covered the net loss of the whole of last year. Many happy returns to all my readers.

Let’s all say thanks to the Fed Chair Jerome Powell. Global stock markets loved his rapid turn toward dovishness and his willingness to stop balance sheet tightening by 2020, rather than 2021. The markets have bullied him into doing what they want. Another central banker with no spine. Yay …the Fed put is back! In Europe, ECB governor Draghi has got even more dovish (if that was possible) hinting that QE may be extended into 2020.

Of course the long term implication is far less benign. The US stock market didn’t like Fed funds above 2.25-2.50%. The ECB can’t get rates even back to a positive number. Neither can unwind QE without the market having a panic attack. Japan seems the model here and that is not good for anyone.

LikeLiked by 1 person

Aha yes that does make sense. I think I was taking too much of a break to focus on the Fed but this narrative feels bang on. Thanks!

LikeLike

[…] FireVLondon has a pretty good January (23) […]

LikeLike