It’s the end of the second quarter. That means it’s time for my usual monthly portfolio performance along with a quarterly review of how 2017 is progressing.

June’s news was dominated by the UK’s general election. To my mind the electorate called it about right. Under the UK’s first-past-the-post constituency system no voters have a say on the overall leadership, but nonetheless the overall outcome often reflects the wider mood of the nation with uncanny fidelity. That’s what seemed to happen here: the Tories were badly led down by their leader, and Corbyn’s Labour offered a genuine and, to many, welcome alternative. Yet at the end of the day the Tories remain in power, with an extremely short leash and an exploding collar.

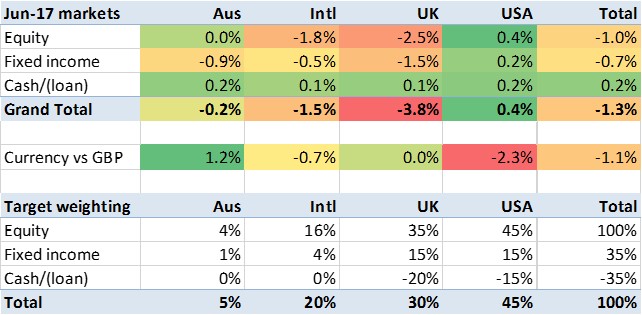

The other news in June, which if you blinked you might have missed it, was the central banks publicly stuttering about the next policy move. This unsettled UK and USA markets noticably, but it seems to have lasted less than a week. From the point of view of my process however this was material; the pound gained about 3% culminating in it reaching $1.32 at exactly the end of the month (see graph). Even as I write this, a few days later, the pound has reverted – but as I took my portfolio snapshot on 30 June my quarter-end numbers were pretty different.

The other news in June, which if you blinked you might have missed it, was the central banks publicly stuttering about the next policy move. This unsettled UK and USA markets noticably, but it seems to have lasted less than a week. From the point of view of my process however this was material; the pound gained about 3% culminating in it reaching $1.32 at exactly the end of the month (see graph). Even as I write this, a few days later, the pound has reverted – but as I took my portfolio snapshot on 30 June my quarter-end numbers were pretty different.

Even a week before the end of June I was having a positive month. But thanks to the pound blipping upwards at the last minute, and most of my portfolio being overseas at this point, I recorded a negative month. If the pound remains at the level it’s already returned to, then I am highly likely to post a positive July.

As it happens, the Aussie dollar had an even stronger June. But the USD fell 2.3% and the Euro fell 0.7%, so the currency headwinds for my portfolio averaged negative 1.1%.

When ‘foreign’ falls, the UK’s FTSE-100 goes with it. The biggest UK businesses are mostly global businesses, for whom ‘foreign’ is the biggest driver. In June, with the USD falling 2.3%, the FTSE-100 fell 2.5%, almost in lockstep.

In the meantime the European equity markets stumbled at the end of the month too, I think unsettled by those same central banker comments. And bonds eased off slightly too – particularly in the UK. While US markets maintained their poise, the weighted average across my exposure was a loss of 1.3%. Coupled with my forex headwinds, I’m anticipating a 2.4% fall in June – one of the more hostile environments I’ve seen for a while.

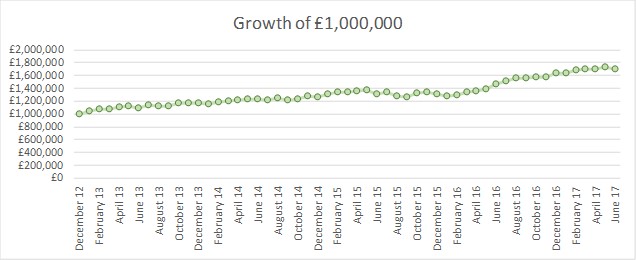

Sure enough, My investment portfolio lost 1.6% in June (leaving the quarter up, but only by 0.5%). One of its worst results for months. But not as bad as the markets overall. And I reported a few months ago how the relentless upward march of the markets had left me feeling ‘giddy’ so I can hardly act surprised by something of a correction. As I mentioned above, if anything the odd thing here is how spiked it was on the last day of the first half of the year.

I had three financial goals for 2017.

The first goal was to stick closely to my target asset/geography allocation.

In Q1 I I was trying to pay down my margin loan. My overall loan-to-value fell by about 1.5% to about 28%. I’ve made further progress on this. By liquidating some bonds holdings, and belatedly biting the ‘stupid bullet’ and using some idle USD cash to pay off my GBP loan, I’ve reduced my loan by well over £100k in Q2. My LTV now sits just above 26%. This leaves me about 2% overweight on cash, which I’m very happy to be.

I’ve maintained pretty tight exposure tracking throughout Q2. My overall UK exposure, which is underweight both equities and fixed income, is a bit adrift at -2.9%. But this is where I want it. This goal is PASSED again.

Delta from target exposure, % of portfolio

My second 2017 goal, about spending/cashflow being on track, is a lot of work to measure. However, I am pretty certain I’m OK this quarter, because my earnt income spiked upwards and my spending remains roughly unchanged. So this goal is a provisional PASS. Arguably what really matters here is hitting this goal without earning any money, but I am much less interested in the semantics of FIRE than Monevator and numerous others, and I’m enjoying the work.

My third 2017 goal is about tax efficiency. I set out my intention to move £200k into my wife’s name this year. Actually, since the fascinating discussion on my ‘Peter’ blog post, I’ve realised I need to upweight my Ltd Company assets too. So how have I got on?

I’ve had my eye off this ball in Q2. I’ve only moved £25k out of my name; some into my Ltd Company, and some into Mrs FvL’s ISA. I did also move £20k of assets into my own ISA, so there was almost £50k shifting around in a tax efficient direction. But I’m giving this goal a mild FAIL. I say mild because I still have time to catch up later this year.

In Q1 I said my portfolio earnt a lot more than I did. In Q2 the reverse was true. Overall it was a fairly unremarkable quarter, in which I made solid progress towards a well balanced, tax-efficient and low cost portfolio.

Hi FvL,

A shame that the change in the £ has impacted your overall portfolio – are you wanting a stronger or weaker £ just out of interest?

Your graph against the £1M invested shows some really good progress over the last 5 years. Congratulations on paying down the loan by a relatively significant amount and getting the LTV down – at this rate it will be gone in now time!

There is a lot to be said about an unremarkable quarter – slow and steady and continuing to tick up – it is all good. I wait with interest to see what happens in your tax efficiency approach – I assume you are also filling up Mrs. FvL’s pension as well as ISA?

Cheers,

FiL

LikeLike

@FIL generally my diversified allocation leaves me ambivalent between strong and weak pound. For UK Inc I would prefer a stronger pound but at the end of the day stability is what really matters.

Yes Mrs FvL’s pension will be getting gentle topups too. I am a bit sceptical about pensions but hers has a long way to go so the only way must be up!

LikeLike

Hi FvL,

Cool thanks – being ambivalent to the strength of the pound certainly takes a weight off the mind I can imagine!

Glad to hear you are making the most of Mrs FvL’s pension allowance as well – like you I am somewhat sceptical of them as they will keep changing the rules, but the tax rules just make it a must sadly!

Cheers,

FiL

LikeLike

Mr Market makes “Noise”. Traders bid prices up and down, but unless the world comes to an end, nothing has changed and if it does we will not be around to care/worry. Yep sure there are boom and busts, again thanks to the Traders, bidding up the prices or vice-versa. but if the world does not come an end then good quality companies will continue to churn out the results, the dividends and share growth.

LikeLiked by 1 person