The month began with the Conservative party annual conference, and the aftershocks were still being felt as the month ended. The prime minister sounded much more pro ‘hard’ Brexit than the markets had expected, and the home secretary was willfully misquoted by everybody – especially overseas – as saying that UK companies would have to publish lists of their foreign workers.

From an investing point of view the main impact arose from May’s critique of quantitative easing:

“People with assets have got richer. People without them have suffered. People with mortgages have found their debts cheaper. People with savings have found themselves poorer….. A change has got to come.” – Theresa May, UK Prime Minister, October 2016

Lest you wondered whether the change needed is the Government’s problem or the central bank’s problem, William Hague (a former Tory leader) helpfully clarified the next day that the Bank of England’ ‘days of independence could be numbered’ unless its policies change. If this didn’t look like political interference, what would? This, after all, was from the party which strongly opposed giving the Bank of England independence back in 1997.

Just as I was beginning to contemplate whether we might be in for a full-on Sterling crisis if Mark Carney, the foreign Bank of England governor, decided he’d had enough, the latest news is that he will be staying until mid 2019. Hopefully the Tories have seen into the abyss and will step back from it. Carney may not be perfect but there is no better anywhere in the world and right now losing him would be a big mistake.

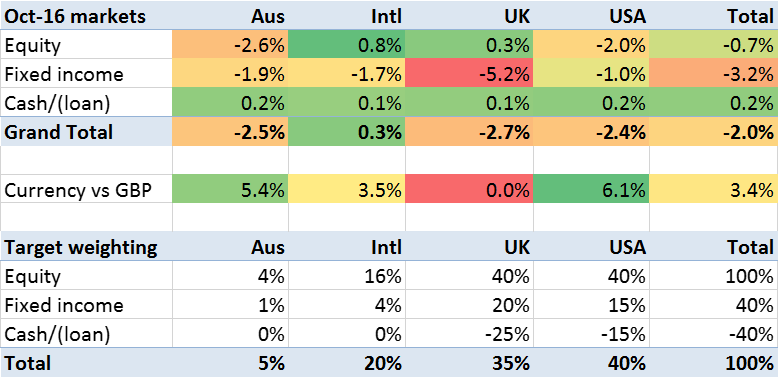

In any case, the wider damage inflicted by the xenophobic and anti-economy tone of the UK government has been reflected in a further significant drop in the pound. It has fallen by 6% against the US dollar and 3.5% against the Euro. The weighted currency impact on my portfolio has been to increase my overall portfolio, measured in pounds, by 3.4%. In one month. Hooray for a globally diversified asset allocation.

The underlying markets, measured in their local currencies, fell slightly in October. Australian equities and bonds fell around 2%. US equities fell 2%, bonds slightly less. Weighted by my exposure, the market fall was about 2.0%.

The big drop was UK bonds, which fell over 5%. This is a massive drop for a supposedly low volatility asset class. In foreign currency terms the drop was closer to 10%. Does such a drop reflect the extreme highs to which bonds have risen over the past few years? Does it reflect a dramatic loss of confidence in the pound ? Does it reflect the prospects of higher interest rates? Does it reflect some market technicalities? Time will tell.

Allowing for the foreign exchange movements the overall markets I’m exposed to rose by about 1.4%.

My portfolio duly ended up 1.2% in the month. Not a bad result, and my ninth consecutive monthly gain. My portfolio, measured in UK pounds, has gained 20% so far this year, and over the last twelve months. Quite an extraordinary performance. And a performance which confirms the UK Prime Minister’s observation that the asset-rich have got richer. She’s right too that my mortgage and margin loan debts have got cheaper. It’s a funny old world, this terrible Brexit thing, isn’t it?