My goals for each quarter are as follows:

- For my net loan to shrink by £10k per quarter, without any margin calls.

- Maintain investment income of at least £Xk

- Closely track my target asset allocation

Goal 1: For my net loan to shrink by £10k/qtr

This goal is proving somewhat unsatisfactory, because it’s harder to assess than I had hoped.

The nature of a good margin loan – as implemented by Interactive Brokers – is that it is quite hard actually to track repayments. It operates a bit like an offset mortgage; it is just a cash balance. Any cash paid into it via e.g. dividends reduces the negative balance. Any cash consumed from it – e.g. a share purchase, or brokerage fees – adds to the debt. Given that I have been trading a bit, the margin loan fluctuates naturally.

My other margin loan – with a private bank – is a different matter. It sits in its very own account. Cash income from my portfolio sits in other accounts. If I want to use cash income to pay down the margin loan I need explicitly to transfer the cash from one account into another. Intellectually I like this approach less, though I must admit it is easier to track the actual repayments.

In any case, my bargain-hunting has got the better of me in June, with my purchases (in Interactive Brokers etc) having helped increase my overall net debt by over £20k. This came from £13k of net buying and the rest was interest costs. This is rather feeble because I didn’t even pay the interest properly on my private bank loan – it has just added itself to the total loan. So this goal is a FAIL.

As it happens, I’m not beating myself up too much about this fail. Readers may recall I toyed with the idea of measuring my loan as a percentage of the portfolio value. In the end I decided against this as I didn’t want to feel I should reduce my loan if the equity values all plummeted. In fact what has happened is the opposite; my equity value has risen strongly, leaving my margin loan falling from around 35% to around 30% of my portfolio. Happy days.

Goal 2: Maintain investment income of at least £Xk.

My investment income is also proving quite hard to track.

In Q1 I benefited from some useful lags – in that I received dividends from stocks I’d already sold. So in terms of actual income I saw a 20% drop in Q1 from the year earlier. This lag has pretty much unwound, and Q2 saw a 43% drop in income from 2015. 43% drop in income is pretty painful. I had anticipated something similar, and in fact my target income of £X is a lot lower than my income before buying my Dream Home.

The other measure I track here is the ‘running yield’ of my portfolio. This is not very accurate but does closely track reality. This (pound) number has risen significantly post Brexit, reflecting the drop in value of the pound and the high level of overseas assets I hold. So in fact after Q1 this projected income figure was 53% below the year earlier – even worse than the drop in actual income that I received. At the end of Q2 though my projected income is only 39% below the year earlier.

At the end of Q2 my actual income received was about 5% more than £Xk. This goal was HIT.

Provided the stock markets hold up then my ability to hit this goal should be OK. I am continuing to reinvest some of this income so I will gradually enlarge my safety buffer.

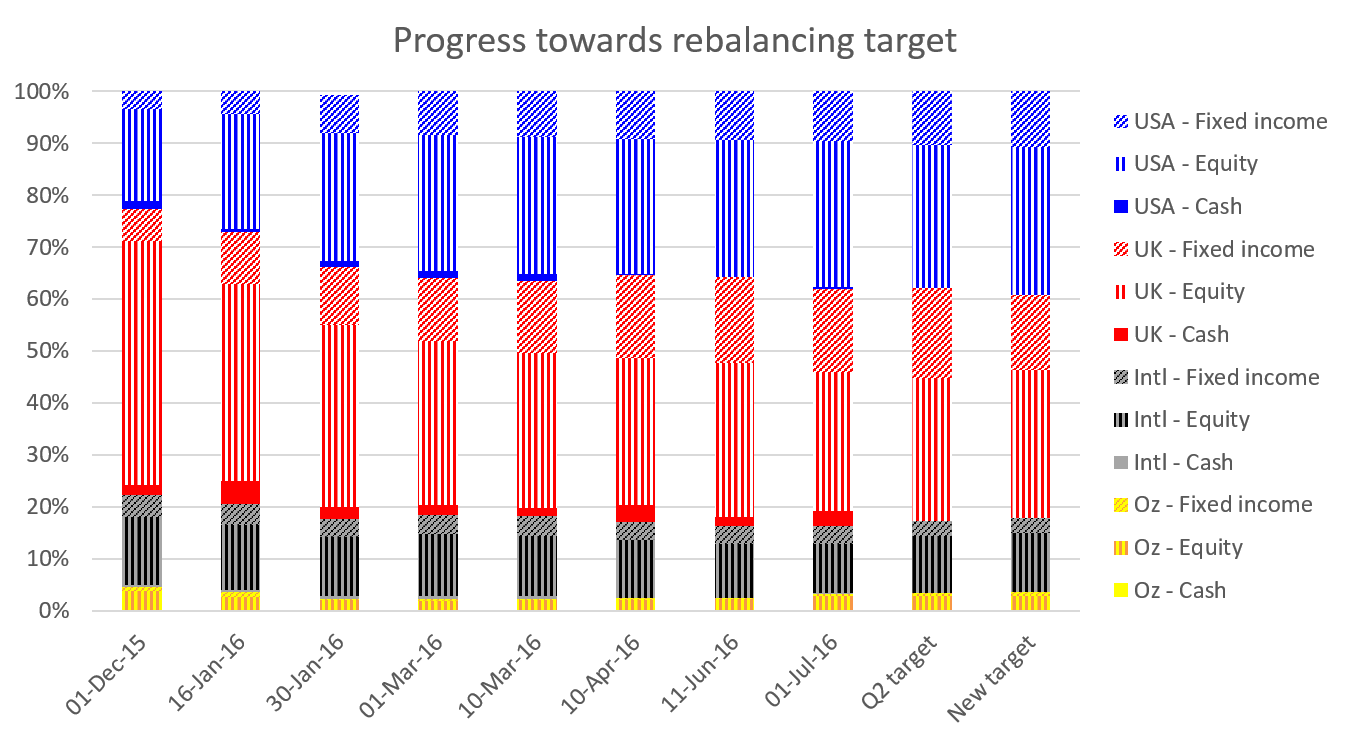

Goal 3: Closely track my target asset allocation.

I finished Q1 overweight 5% on my UK loan and underweight 7% on the US loan; this left me exposed if the pound gains versus the dollar. Fortunately that is the opposite of what happened, with the pound falling about 10% against the dollar. In terms of the mix of investments I finished Q1 very close to my target allocation.

In Q2 I have tightened up further. Looking at my position on 1 July versus my target, the only slight mismatch against my intended allocation is being a bit underweight on UK fixed income (and this was due to me consciously reducing my bond exposure when bonds had gained >10% YTD) and being a bit underweight on International Equities (which given the fall in Eurozone stocks is not surprising). I have a bit of cash ready to pounce on any buying opportunities. Overall this goal was HIT.

Since the end of the quarter, I have slightly changed my target allocation. With my loan now at only 30% of the value of my portfolio I’m looking to reduce my target debt level (to the level I’m already at, fortuitously). I’m also up for a slightly higher share of equities rather than bonds (i.e. I’m not up for buying more bonds at current prices!). You can see my evolution over time and the new target in the graph below. This change effectively says I want to stay where I am at the moment – and just use market dips to signal buying opportunities against this target allocation.