April was the first month for me where the portfolio damage (and buying opportunities!) of August and December last year felt truly behind us. The FTSE-100 index reached 6350, and S&P crossed 2100.

What else happened in April?

- The Brexit referendum campaign seemed to swing slightly against the Brexiteers, coincidentally around the time President Obama was meeting Prince George in a bathrobe.

- The Panama Papers scandal broke. In which the UK’s PM was vilified for his father having been an investment manager and having done what UK tax authorities pushed investment managers to do for most of the last 50 years – he set up his structure in an internationally-compatible way.

- The oil price rose to $45/barrel. This is over a third up from a low in mid-January of $32.

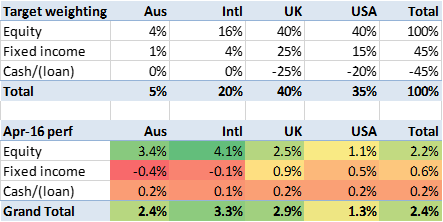

In early April, I finally received the funds for a couple of illiquid assets which I sold some months ago. Aside from a very small portion of these funds which Mrs FvL will ‘invest’ in furnishing the Dream Home, I’ve halved these proceeds: one half has reduced my margin loan and the other half has been added to my investment portfolio. Accordingly I have slightly tweaked my target allocation – it has shifted from 100:50:-50 equity:bonds:cash to 100:45:-45, reflecting the slightly smaller debt load and a slight increase in the equity mix to mirror the drop in risk.

Against this backdrop, my portfolio returned a slightly disappointing 1.0%. Not, you understand, that 1% in a month is disappointing. But most markets were up in April, and at my target (and leveraged) exposure I’d have expected 2.4%. So I lagged the market by about 1.4%.

Why did I lag? As with March, a big factor is the strength of the pound. All my major overseas currencies fell against the pound – by about 3%. Put the Australian monthly equity return of 3.4%, let alone the US equity gain of 1.1%, against a drop of 3% and you aren’t happy. I am relatively relaxed about these currency fluctuations, as described elsewhere in this blog. In fact a key part of my strategy this year is to reduce my UK exposure to insure myself against the risk of Brexit hammering the pound.

Another reason for my lag is that I have been relatively underweight on the resource sector. With the oil price recovering, key commodity stocks like BHP Billiton, BP, Glencore and Shell have risen strongly. I don’t have much of this sector; less, in fact, that I had before rebalancing in January because I have disproportionately sold my FTSE ETFs.

Overall I’m happy and relieved with the last few months since I took out a margin loan in January. My portfolio is up 5.2% since January, and my debt has dropped from over 37% of my total to under 32%. I’m also three months closer to selling my old house, at which point I’ll be in a position to repay the entire margin loan. The downside risks from me taking on leverage have dropped dramatically.