In March the rain stopped. We started March with North London already having seen 2x its usual rainfall for this point in the year. And thankfully in the middle of March, it stopped. As I write this I have actually needed to start watering the garden, something that felt a very remote prospect a month ago.

I’ve had quite a bit of travel in March. Some travel to the south coast. And some travel to the Alps.

Meanwhile out in the wider world, the US and Israel have been hard at Iran. I’m not going to comment on this madness except for what it’s done to the markets.

Markets in March

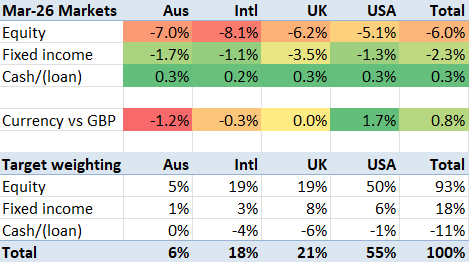

The market most impacted by the Iran war is the energy market. Diesel prices are up sharply; jet fuel is in short supply, and regular unleader is up significantly too. Americans, with lightly taxed fuel, are seeing a sharper increase (there is some justice in the world). Here in the UK unleaded has gone from c.£1.37/ltr to £1.57/ltr; this is a spike but not the end of days.

The Australians have copped it worse for some reason; they all rushed to the pumps to hoard fuel and lo the pumps ran dry. Why Australian fuel disruption is worse than any north of the Equator baffles me.

Meanwhile, for crazy policy reasons, the UK’s electricity prices have actually just fallen. Much worse will be to come later this year but in the meantime all feels relatively stable on the energy-prices-are-escalating front. Certainly even the most badly affected prices are not nearly as high as they soared back in 2022 when the other crazy president was running amok.

In any case, the stock markets in March are a textbook response to global market jitters. Ironically, the USD has seen a flight to safety. But everything everywhere is down all at once, pretty much. Equities were down around 6%, and bonds were down around 2%. UK bonds were down even more with too much loose talk about energy bailouts.

My portfolio’s March

My portfolio proxy VWRL was down 6.2%. And my portfolio was down 5.7%. At one point towards late March things were even worse but hey ho. In the scheme of things I got away relatively lightly; for instance GOOG, my biggest single line holding, has seen a ~20% drawdown since early February.

When markets drop a lot I need to pay attention to my leverage. However thankfully I entered 2026 with leverage levels below my long term target. My portfolio loans remain low; the size has barely changed in two months, and remains at a level lower than before I bought the Coastal Folly. The ratio Loan-to-Value has risen slightly, as the portfolio’s value has dropped, from 9.3% to 9.8% but my risk levels remain very mild here.

March was the end of the UK tax year. I’ve been thinking a bit about crystallising losses but most of that activity happened in February.

As I write this we are now into the new tax year and I’m slowly filling my ISAs against their new allowance. I’m not doing this as quickly as normal; as of 12 April I have topped up my + Mrs FvL’s ISAs with £6k (15% of the £40k combined allowance). I expect a small windfall in the next couple of weeks which I have earmarked for a bigger topup.

Appendix – Press in March