A year ago this week I sold my Modern Flat. And shortly afterwards, I reinvested £500k into a liquid stocks/shares portfolio with a property-like mandate. One year on, here’s a short review of the performance.

The portfolio has been set up to spit out £2000 pcm, which I take into general household expenses. This amounts to a 4.8% withdrawal yield on the £500k initial portfolio value.

What’s happened?

I ran out of money once, by about £100. As it happened, when that happened I ended up receiving a dividend on the 31st of the month which meant I had *not* in fact ran out of money, but by then I had already lent the portfolio the money to cover. I charged the portfolio £50 of interest costs for the trouble.

I stand today with about £5640 of cash in the account. I’m not sure whether further dividends are due in October but in any case I am certainly not going to run out of cash in the foreseeable future.

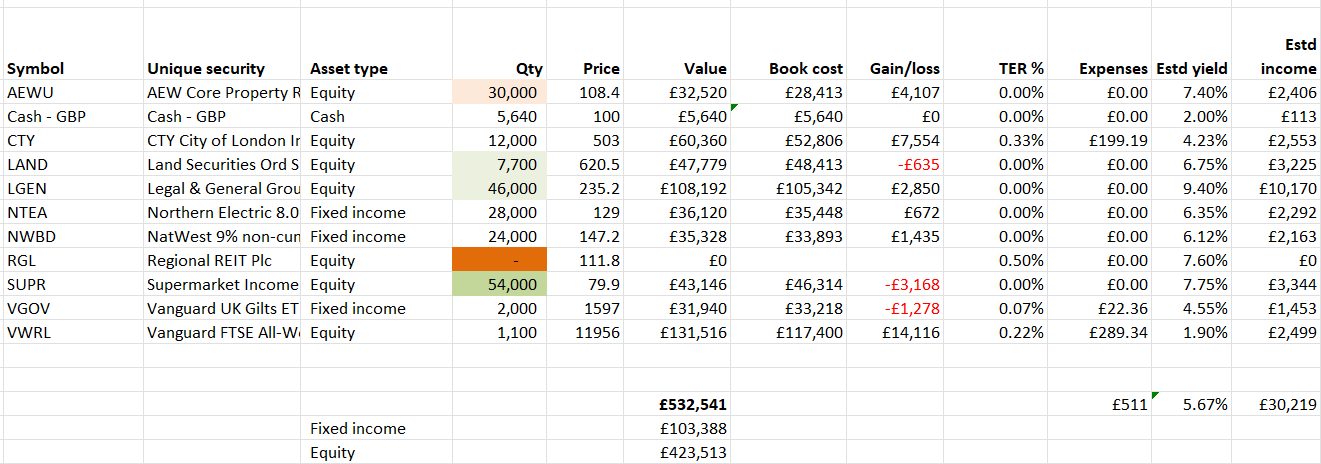

Partly in response to comments on my original blog post, I rejigged the portfolio a little bit half way through the year. I reduced the AEWU position in half, which I don’t think has made much difference (partly because it had already risen by almost 20% when I did this). I replaced RGL with SUPR; RGL has dropped but so has SUPR. I sense I timed this badly, but am happy with the swap.

I watched LAND drop significantly after I opened the position, but I didn’t have enough spare cash to top up and average the cost price down. By the time I did have some spare cash, months later, LAND had mostly recovered. In any case I have topped up a little bit.

The anchor stock in this portfolio is LGEN. My ~£100k LGEN holding has produced over £10k of dividends. It feels churlish not to partly reinvest these, so I have added 1000 shares to the initial 45k holding. Most of this dividend is being spent, but a 2% reinvestment will help me inflation-proof. The share price is up about 5%, down from an intra-year gain of about 10%.

The two notable contributors here have been the equity index holdings. I started with about £50k of CTY, a FTSE-100 proxy. This has risen 14% (and produced >4% dividends). And my biggest holding, VWRL, Vanguard’s world equities index, has risen 12% (plus ~2% dividends). These two holdings have added £22k of value to the portfolio alone.

Returns after 12 months

The portfolio value one year on stands at £532.5k. The portfolio has risen in value by 6.5%, and paid out income of 4.8%. That’s a total return of over 11% – more than £50k.

Assuming a tax rate of 40%, applicable to the 4.8% dividend income only, the tax bill will amount to just under 2% of the portfolio value, around £10k. Plus a few hundred quid of capital gains tax on the trims/disposals. That’s an effective tax rate of less than 20% of the total return it has generated.

That’s one:nil to stocks&shares over property.

What’s next?

Inflation over the last year has been about 3-4%. Rents have, from what I can gather, increased about the same. So I’ve bumped up the monthly standing order by 3.5% to £2070 pcm, almost £25k pa.

Thanks to the hefty increases in the equity index holdings, I am now underweight on fixed income compared to my starting position. While I am tempted to let it ride, with the media full of talk about stock market bubbles, I will rebalance back to 20%:80%. To rebalance I need to sell £4k of equities and buy £4k of bonds. I will sell 1000 CTY (currently at £5.03/share, yielding 4.23%) and buy a mixture of NWBD (yielding 6.1% , NTEA (yielding 6.3%) and VGOV (yielding 4.5%).

Even before rebalancing, my projected income of £30.2k suggests I have reasonable headroom above the annual withdrawals.

So far, so good. The portfolio is better positioned than it was a year ago, and my ‘rental income’ has risen with inflation. Next, one more year into the breach.

great analysis. Thank you!

LikeLiked by 1 person

A great reminder that property investing doesn’t mean only buying bricks and mortar. There’s lower hassle and more diversified routes to go down.

LikeLiked by 1 person

Great to see how this is going. Have you considered adding property exposure beyond UK markets?

LikeLike

Eddie – no, I haven’t. Generally I understand the property markets in the UK, and this portfolio is an experiment to see what a substitute for a UK property holding could look like.

I wouldn’t really know where to start with non-UK property markets – any suggestions would be interesting!

LikeLike