One of several highlights for me in January was visiting Salisbury cathedral, which I did on an impulse while travelling back from the Coastal Folly.

My main frame of reference to the cathedral being those notorious Russian nerve agent assassins citing it as their reason for visiting England, something which to a Londoner had as much plausibility as as Putin’s claims that Ukraine’s Nazis started the war. I hadn’t taken seriously the idea that the cathedral might actually be a reason to visit England. But I would say I was wrong – it is stunning, and surprisingly moving. Photos really don’t do it justice.

Elsewhere in the world, the focus has shifted from the Ukraine war to the Gaza crisis – which has escalated to the Houthi shipping attacks off the Yemen.

It’s the start of a calendar year. Let’s take a look at what 2023 did to me financially. I’m following the same structure I’ve used for the last few years (2022, 2021, and 2020). Overall, 2023 was a good year on almost all measures – thanks in particular to Q4 which saw the US stock market drag the year into a top quartile performance.

Q1 How did markets do?

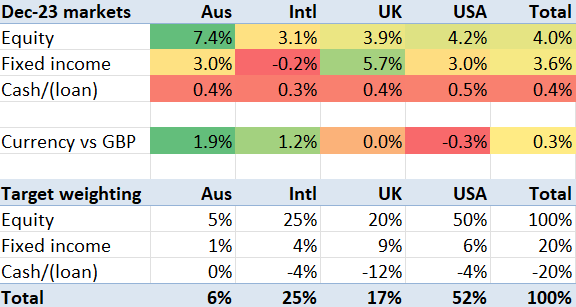

First of all, what happened out there? Well, the year felt pretty ‘meh’ for the first nine months – as illustrated by my rather depressed blog post in mid October. But almost as soon as I hit Publish, the US market in particular led a dramatic recovery – reflecting a sharply improved outlook for inflation and interest rates. You can see below firstly the performance in December.

December 2023 market returns, by geography and asset class

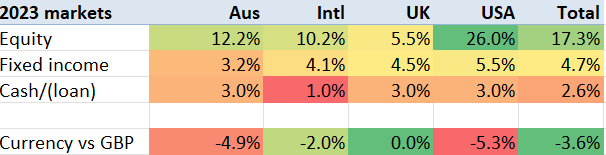

Then we get to the year as a whole. Bonds rose by 3-5% across the board, but equities did strikingly better – particularly in the USA where the S&P500 rose around 26%. The UK equity market looks like the runt of the litter, which given the tech-driven nature of the uptick and the lack of UK tech wouldn’t be a big surprise. However it isn’t quite that simple, because the GBP rose against most currencies.

2023 market returns, by geography and asset class

Another way to look at the benchmarks is to look at the world equities (e.g. VWRL) and world bonds (e.g. AGG/BND or the UK’s IGLT). My portfolio has often pretty closely tracked the VWRL ETF. The graph below shows VWRL and IGLT’s share prices (but not dividends) for the year, showing the world equity bundle up (in GBP) 13.4% and the UK government bond index roughly flat.

2023 performance of Vanguard World Equities, and UK Government bonds (excluding dividends)

Q2 How did I do, vs my benchmark?

Against that backdrop – bonds up a bit, equities up considerably more especially in the USA, how did my portfolio perform?

But my net worth includes an important asset class – property – that I don’t normally track, but which I have held in some form for over 20 years.

So, this post takes a look at how my real estate assets have performed.

Real estate works completely differently, for me, than my investment portfolio. For starters, I have never bought a home as an investment. But let’s start at the beginning.

My property owning history

I nearly got on the property ladder in the mid 1990s.

I hadn’t realised, until a friend pointed it out a few years too late for me, that in fact one of the easiest times to get on the property ladder was the moment when I graduated and moved to London. My first job earnt a reasonable London salary of just over £20k, and 1 bed flats in a reasonable part of Zone 1 in London were available for under £70k (now £800k-£1m, sigh).

Mortgage rates had dropped from >13% in 1990 to around 7%. The interest costs could have been around £5k, a quarter of my first-job income. That was in the mid 1990s. It didn’t occur to me to buy a place, and of course those property prices were so high…..

By the late 1990s, buying a property had become a lot harder. But once I was earning £40k+ I decided to take the plunge. I found a reasonable 2 bed place very close to Zone 1 for £200k (now £500k). The mortgage (at around 7% interest, i.e. interest costs were £13k, a third of my gross income) and the deposit (£20k, if I remember rightly, for a 90% mortgage) were a massive stretch….. and then I was gazumped. By the time I reorganised, the places I wanted cost £220k+ and I couldn’t quite afford it.