It’s the start of a calendar year. Let’s take a look at what 2023 did to me financially. I’m following the same structure I’ve used for the last few years (2022, 2021, and 2020). Overall, 2023 was a good year on almost all measures – thanks in particular to Q4 which saw the US stock market drag the year into a top quartile performance.

Q1 How did markets do?

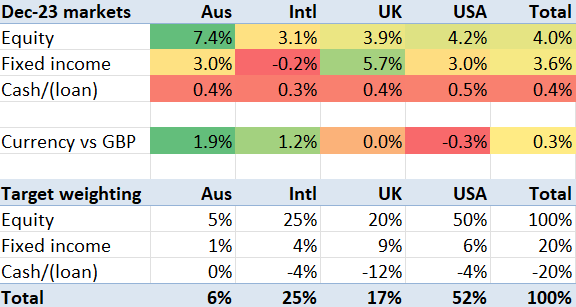

First of all, what happened out there? Well, the year felt pretty ‘meh’ for the first nine months – as illustrated by my rather depressed blog post in mid October. But almost as soon as I hit Publish, the US market in particular led a dramatic recovery – reflecting a sharply improved outlook for inflation and interest rates. You can see below firstly the performance in December.

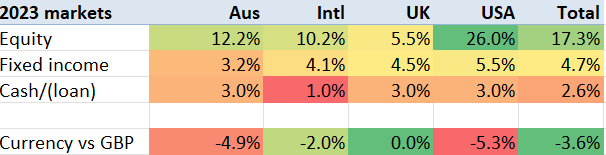

Then we get to the year as a whole. Bonds rose by 3-5% across the board, but equities did strikingly better – particularly in the USA where the S&P500 rose around 26%. The UK equity market looks like the runt of the litter, which given the tech-driven nature of the uptick and the lack of UK tech wouldn’t be a big surprise. However it isn’t quite that simple, because the GBP rose against most currencies.

Another way to look at the benchmarks is to look at the world equities (e.g. VWRL) and world bonds (e.g. AGG/BND or the UK’s IGLT). My portfolio has often pretty closely tracked the VWRL ETF. The graph below shows VWRL and IGLT’s share prices (but not dividends) for the year, showing the world equity bundle up (in GBP) 13.4% and the UK government bond index roughly flat.

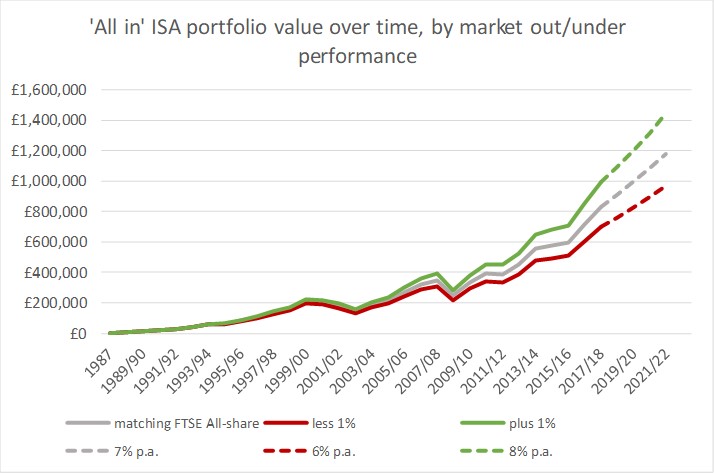

Q2 How did I do, vs my benchmark?

Against that backdrop – bonds up a bit, equities up considerably more especially in the USA, how did my portfolio perform?

Continue reading “Dec ’23 – 2023 in review”