It’s that time of year again. The start of the new UK tax year (for ancient reasons, UK tax years begin on 6 April). My favourite time in the financial calendar.

It’s time to top up the annual ISA. ISAs are the tax-free savings accounts we are – unusually in the world – blessed with in the UK. While the funds we put into an ISA are net of tax, with no pension-like tax relief when we save, all subsequent returns are tax free. Forever. If you are fortunate enough to have £20k lying around, and you move it into an ISA…. by the time it has doubled, say, four times (which it probably will, if you invest in low-cost equity trackers and live long enough) it may well be producing £20k a year of tax-free income. If you can do this enough times, when you are young, your ISA will knock your pension into a cocked hat.

There are no upper limits on how much you can have in your ISA pots, unlike pensions. Hence, one of my ambitions is to (live long enough to) build an ISA pot worth potentially $100m.

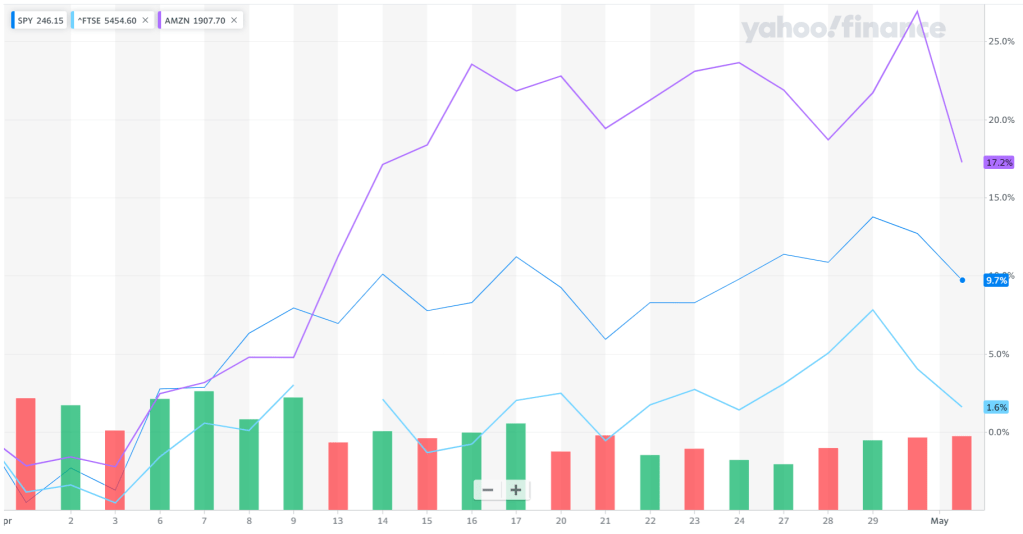

However, with markets melting down over the last two months, it is definitely a case of two steps forward, one step backwards. Nonetheless, my ISA’s income is £24k – up about 10% on last year – so our (two) ISAs are generating more than one of us can top up every year.

Continue reading “My ISAs need a topup” →